Developing an Implementation Plan for ‘You Collect We Buy’

Capitalising on the gas capture opportunity

Summary

This paper puts forth recommendations on how the European Union’s “You Collect We Buy” initiative can catalyse the realisation of gas capture opportunities, considering actions within the direct control of the European Commission, as well as necessary actions that fall under the competence of key stakeholders such as partner governments, companies, financial institutions, and NGOs.

The paper builds on elements and suggestions collected during a stakeholder workshop in Paris in June 2024, co-hosted by Clean Air Task Force, the European Commission and the International Energy Agency, which sought to develop a robust understanding of the operational, financial, and market barriers obstructing gas-recovery projects, while also considering what solutions could resolve these challenges and lay the groundwork necessary for all stakeholders to seize the gas-capture opportunity.

Introduction

Gas venting, flaring, and leakage accounts for tremendous wastage. An estimated 267 billion cubic metres (BCM) of natural gas could be made available to gas markets with a global effort to reduce methane emissions and tackle non-emergency flaring.1 These volumes amount to more than 70% of the EU’s annual gas consumption, which was estimated at 360 BCM in 2023, and could be worth $48 billion.2 This wasteful practice harms not only the environment due to the high emissions of heat-trapping greenhouse gases but also harms the health of local communities in the vicinity, and ultimately results in lost revenues for producers.

While venting, leaks3, and flaring present considerable environmental and economic risk, they are also an indication of a considerable untapped opportunity. If this gas was captured instead of released into the atmosphere, it would help safeguard the climate and generate revenue for producers, as well as energy security for purchasers, potentially supplying enough gas to meet forecasted increased demand for natural gas through 2030 in some regions.

However, these transformative benefits pose an important question: if capturing gas is both profitable and technically feasible, why haven’t producers and purchasers leaped at the opportunity? The answer is complex. Several barriers exist that block the realisation of economically and technically viable projects such as market failures, insufficient financing, competing capital investment priorities, and lack of stakeholder coordination, leadership, and company engagement.

Why tackle methane emissions?

Methane is a potent greenhouse gas that traps 82.5 times more heat in the atmosphere than CO2 over 20 years, and 29.8 times more heat over 100 years.4 As a short-lived climate pollutant, methane has a disproportionate impact on short-term climate change, and cutting these emissions is one of the fastest and most cost-effective solutions to avoid passing irreversible climate tipping points. According to the IEA, 77% of methane emissions in the oil and gas sector can be eliminated with existing technology, and 52% can be eliminated at low or no net cost.5 Despite this, 2023 saw record high methane emissions from the energy sector, as well as increases in global gas flaring.6

Graphic 1: Methane Emissions in the Energy Sector (Source: IEA)

At the fundamental level, most companies and countries are simply not engaged in materialising these opportunities, which can be the result of a lack of internal funding or a perception that these projects deliver unattractive economic returns. This challenge is exacerbated by the lack of available external financing, high costs of capital, and risk perceptions in low- and middle-income countries. Even when these barriers can be overcome, contractual models between various partners in an oil and gas field may not incentivise cooperation, leading each actor to optimise their own gains, rather than align behind a collective approach.

Overcoming these challenges will be a formidable task, and at COP28, European Commission President Ursula von der Leyen announced the EU’s first steps to do so. Through “You Collect We Buy”,7 the EU aims to reduce methane emissions and gas wastage beyond its borders by supporting the purchase of collected gas from the EU’s trading partners. Successfully realising this vision will depend on overcoming an array of structural challenges – many simultaneously – and cooperation from a broad group of stakeholders.

This paper puts forth recommendations on how the “You Collect We Buy” initiative can catalyse the realisation of gas capture opportunities, considering actions within the direct control of the European Commission, as well as necessary actions that fall under the competence of key stakeholders such as partner governments, companies, financial institutions, and NGOs. As many essential incentives are not within the remit of the European Commission, such as a certification scheme, carbon credits and offsets, and price premiums for abated gas, the paper emphasises the need for a partnership framework to facilitate their development and uptake.

The paper builds on elements and suggestions collected during a stakeholder workshop in Paris in June 2024, which was divided into three consecutive discussions on the barriers and challenges to scaling gas capture projects. Participants first discussed issues related to pre-project development, then those related to economic feasibility and financing, and finally issues related to marketing and certification. Participants then split into three groups to discuss three separate case studies examining past and potential gas-capture projects, prepared by Capterio and Carbon Limits. These case studies covered projects in Nigeria, Egypt, Azerbaijan, and undisclosed locations, and encouraged participants to consider concerns specific to geographic regions, operational challenges, and collaborative efforts that may be required to move a potential opportunity to completion. This paper loosely follows the structure of the workshop, with notable observations from three case studies included where appropriate.

Graphic 2: Global gas flaring at upstream oil and gas facilities, and flaring intensity, 1996-2023

Barriers and solutions to pre-project development and identification

Barriers: What is holding back project development?

Capturing gas from legacy assets and placing it on the market starts with project identification and project development, which entails recognising, investigating, and understanding potential opportunities where significant quantities of gas are being leaked, vented, or flared.

Despite the immense economic and climate benefits that could be made possible by gas recovery and methane abatement, these opportunities often are not realised in part due to obstacles in identifying and developing potential projects from a concept to an investable opportunity that can be financed. Project development is a complex and often expensive process, which requires the financing of detailed technical and economic feasibility studies to determine whether a project is commercially viable, and therefore, financeable. These studies aim to identify and determine a path to mitigate potential operational or financial barriers that might prevent a potential project from succeeding.

Project development costs, encompassing these feasibility studies, can cost up to $500k USD depending on the size and nature of the project. These studies, as well as decisions on mitigation actions are typically project specific, and study costs vary significantly for a capital-intensive flare gas recovery project, compared with a leak detection and repair (LDAR) project. Irrespective of the type of project, however, these costs incur significant risk for companies and partners, as there are no assurances that the project will move forward. Since incumbent players are not necessarily interested in prioritising flare capture projects potentially attractive projects are not being developed on request of the operators. Some project developers have attempted to develop projects for operators on a speculative basis. Yet with no guarantees that the project would move forward, or involve the project developer, the investment is commercially risky.

What is already being done to tackle flaring and methane emissions

“You Collect We Buy” was not created in a vacuum – global momentum for methane emissions reductions has been steadily building thanks to several global and regional initiatives, partnerships, and funding mechanisms. These include the Global Methane Pledge, the Global Methane Hub (GMH), the Climate and Clean Air Coalition (CCAC), the Oil and Gas Methane Partnership 2.0 (OGMP 2.0), the World Bank’s Global Flaring and Methane Reduction Partnership (GFMR), the Oil and Gas Decarbonization Charter (OGDC), the Global Methane Initiative (GMI), and the global collaboration to develop a consistent framework for measurement, monitoring, reporting and verification (MMRV), led by the United States Department of Energy. In order to be successful and impactful, “You Collect We Buy” must be careful to be complementary to, and not duplicative of, these existing efforts.

Evolving regulatory frameworks, coupled with robust enforcement measures, are also essential to reducing emissions. Recent regulatory developments in the EU, US, Canada, Nigeria and Colombia all take steps in the right direction. As the EU’s new Methane Regulation will gradually impact all upstream producers selling fossil fuels into the EU market, “You Collect We Buy” could offer a pathway for producers to proactively abate their emissions while also capitalising on the benefits of placing this gas on the market.

These financial risks, along with high levels of competition for capital within companies, offer a partial explanation to why potential gas-recovery and methane abatement projects are not prioritised for legacy assets.8 Many oil and gas projects involve multiple companies in the ownership structure to share risk, resources, technical expertise, and to maximise profit and gain market entry. These operating models are known as joint ventures, with one company serving as the designated operator and the other shareholders acting as non-operating joint venture (JV) partners. Most JV contractual agreements lack legal clauses to responsibly manage methane and other greenhouse gases which presents yet another barrier deterring operators and JV partners from backing project development. The complexity of such arrangements varies greatly but, fundamentally, communication and alignment of partners is paramount to advancing any project.

Often, reduction of flaring, leaks and venting is either not a top priority for management, for reasons discussed below, or is not a priority of one or more JV partners. Internal alignment amongst JV partners is often critical for the sale of gas volumes, the use of infrastructure and pipelines, and other contractual reasons. A decision from one partner not to participate in a project can stop it from advancing.

This means that even when projects are technically feasible, the case must be well designed, substantiated and presented. Companies inevitably have long lists of potential activities and operations that require attention and funding, and investment decisions can be impacted or distorted by several underlying operational challenges. the structure of the workshop, with notable observations from three case studies included where appropriate.

Barriers: What obstacles arise at the operational level?

Understanding on-site operational challenges is essential because they shape the priorities of facility and operations managers, which consequently inform the priorities and decisions of senior leadership. As flaring, venting and leaks have unique driving factors, this section will cover flaring only, and operational obstacles for venting and leaks be considered separately below.

First, one simple, yet fundamental, challenge is the lack of quality data. Flaring is often unmetered and underestimated, if not entirely unreported, and incomplete or poor data inevitably lead to misconceptions about the economic benefits of addressing these emissions. The quality of flare data can vary significantly, as upstream flares often lack continuous measurement for flare gas quality and combustion efficiency, creating uncertainty around baseline measurements and the quantification of any eventual mitigation. While many leading companies maintain that they have a good view of their flaring, according to the experts participating in the workshop, this oversight is sometimes patchy at best for operated assets and can be poor or non-existent for non-operated assets. Furthermore, at the operational level, the various factors driving flaring are sometimes poorly understood, particularly the differences between routine and upset flaring. Having clear visibility on the reasons for all existing flares is essential to reducing non-emergency flaring.

Second, the workshop’s participants noted that flaring is often not a priority for facility managers, who are more likely to prioritise production targets and safety. Facility managers may be hesitant to highlight flaring issues for fear of being perceived as negligent, and in some cases the specialised skills needed to manage gas is not available on site.

Graphic 3: Map of flares in Nigeria, dark blue circles showing onshore flares and light blue circles showing offshore flares. The Sapele, Oben, Oredo, and Oki field cluster are marked with a pink square.

At the next level up, operations managers may not prioritise flaring reduction due to the perceived low return on investment and are more likely to focus on core business investments such as drilling operations. These operators sometimes hold no rights to associated gas emissions, and therefore have little incentive to pursue a project that would only generate additional work with little return.

Combined, the lack of quality data, sub-optimal asset performance, lack of internal incentives, and missing capacity all discourage facility managers and operations managers from prioritising potential flare gas capture projects. Insufficient data across facilities makes it challenging for top-management to justify potentially risky investment decisions and expensive pre-project technical and economic feasibility studies.

Specific Barriers to project development in Nigeria

Challenges to gas-capture vary widely on a country-by-country basis. To analyse and understand these differences, case studies were prepared detailing potential and past projects across Nigeria, Egypt, Azerbaijan, and other undisclosed locations.9 Nigeria notably launched its Flare Gas Commericialisation Programme (NGFCP) in 2016, which aims to drive investments to monetize flared gas, and has several projects in development.

One of the opportunities considered in Nigeria explored capturing flared gas from the four nearby fields of Sapele, Oben, Oredo, and Oki, which would generate 0.4 BCM per year, or an estimated $160 million USD in annual revenue at current export prices. This gas could be transported to the ANOH gas processing plant and power generation facility using the new Obiafu, Obrikom, Oben pipeline (OB3), which is under construction and nearing completion. Despite the proximity of the flares to existing pipelines and facilities, such as Nigeria’s GTL plant at Escravos, investments to capture the gas have not been made because no project had been proposed and presented, along with solid financial analysis. While the Oredo and Oben fields have been previously targeted for flare reduction projects through the development of gas processing facilities, significant flare volumes remain.

Further complications arose from the recent divestment of International Oil Companies (IOCs) to state-owned industry. Whereas there was previously one IOC managing several fields, there is now a different operator at each field, making it necessary to align even more stakeholders to advance projects. Getting site-level information is challenging when companies are protective of their operations, and it was noted that some companies in Nigeria have reported zero routine-flaring, despite satellite data showing otherwise. These challenges can be addressed by a stakeholder coordination platform and risk-mitigation consortium, which will be discussed in detail below.

Solutions: What can be done to improve identification and development of gas-recovery projects?

Building momentum to spark the development of gas-recovery projects starts with improving data on flares and fugitive emissions. Flares should be regularly monitored to provide daily flaring volume data, with a high enough degree of granularity to understand the cause of both upset and routine flaring events, as well as measurements of the gas flow and flare combustion efficiency. Similarly, sources of vented and fugitive emissions should be identified and tracked through robust measurement, monitoring, reporting and verification (MMRV) and leak-detection and repair (LDAR) programs. Uncertainty about methane emissions can also be reduced through use of satellite or other remote sensing measurements of vent and leak emissions.

Second, of equal importance, is building engagement at each level of the company to increase the visibility of these data, its implications, and the potential opportunities. This can be done through both ‘top-down’ and ‘bottom-up’ approaches. From the ‘top-down’, companies can set flaring and methane reduction targets for both operated and non-operated assets, and regularly benchmark progress against these goals. As an example, the 12 companies in the Oil and Gas Climate Initiative (OGCI) set targets, and according to company reporting collectively reduced emissions by 50% – for operated assets – between 2017 and 2022.10 It is also important to leverage the ambition of companies that have made climate commitments, such as joining the Oil and Gas Decarbonization Charter (OGDC). Another ‘top-down’ approach looks to extend and embed methane management across a company’s entire portfolio of JV operations – both operated and non-operated. Companies can address the lack of contractual obligations to manage methane at the inception of new operating arrangements and strive to improve internal governance frameworks that promote communication, stakeholder alignment and decision making directly related to methane abatement e.g., establishing a technical committee or filing a board resolution.11 Such efforts collectively create the internal culture and processes needed to improve data quality and quantity, and establish emissions reduction targets.

From the ‘bottom-up’, efforts should be made to empower and engage facility managers, who must have sufficient capacity and incentive to elevate upset and routine flaring events or emissions data to their operations managers. Facility managers and local operators are crucial to successful implementation of projects – increasing their capacity, as well as capacity for maintenance programmes, planning, and communication between departments can also address issues with sub-optimal asset performance. In the simplest terms, the buy-in and collaborative engagement of facility managers is paramount.

At the next level, operations managers must justify investments in methane reduction, including by finding value for the gas, which can be challenging in regions where the gas has limited market value, or where operators don’t own associated gas emissions at all.12 This could be solved with a market demand signal, clear criteria for a certification scheme, and potential financing schemes, all of which will be discussed in later sections. Ensuring that operations managers are aware of potential solutions to the business case challenge will be essential to getting them on board.

Finally, securing engagement from top management requires comprehensive data over a number of facilities. It was noted that methane and flaring reduction activities shouldn’t be limited to facility and operations managers – involving top management in these efforts was highlighted as an essential component to success. This requires providing them with detailed data on emissions sources. Top management plays an important role in shifting corporate culture, where methane is perceived as an important risk that must be managed, similar to a safety risk, and included as part of key performance indicators. Management can also consider positive reinforcement strategies akin to existing production and safety bonus frameworks, but instead providing bonuses for addressing methane emissions. These types of incentives are invaluable to raising awareness within the company and engaging all employees.

In summary, each level of management must have sufficient data, resources, and incentive to successfully advance a project to the next level, ending with top management justifying the investment decision to shareholders. This notably requires a culture of collaborative engagement and strong communication, as well as each parties’ independent ownership of the data.

Unique operational considerations for venting and fugitive emissions projects

While addressing methane emissions from flaring, venting, and leaks share many of the same underlying challenges related to lack of prioritization within companies, they require different solutions at the operational level. In contrast to flaring, methane leakages mainly occur from worn out or malfunctioning equipment and can happen at any facility. While flare gas-capture projects may cover a smaller subset of facilities, regular leak detection surveys should be carried out across all facilities. Upfront costs, including purchasing an optical gas imaging camera (or similar device) and training staff on how to conduct surveys, are relatively low compared to flare abatement projects. However, ongoing costs for regular leak detection surveys and repairs must be incorporated into regular operations and maintenance budgets. Thus, planning, financing, and operations of leak mitigation looks different from flare abatement projects.

Similarly, venting emissions occur from equipment that is designed to vent, such as tanks without controls and natural gas-driven pneumatic controllers and pumps. This equipment must be properly maintained to ensure that it is not venting more than designed, and it should be replaced with up-to-date equipment that does not vent, or complemented with the installation of control devices, such as vapor recovery units.

Solution: How to mitigate pre-project development risks?

Even after projects are developed, they are not guaranteed to move forward for several reasons, such as diverging priorities between JV partners, who may not have the same level of interest in managing flaring or methane emissions. One potential solution to mitigate this risk is for highly interested JV partners to formally build internal alignment around methane reduction goals within the partnership. This could be facilitated by building partners’ understanding of the importance of tackling emissions, as well as through initiatives such as a written charter for the JV’s governance committee or through a board resolution to reduce emissions and capitalise on gas-capture opportunities.13

Additionally, it is necessary to mitigate risk incurred with pre-project development financing. One solution would be to create a consortium to pool risk for pre-project financing, which would involve profit sharing structures, grants, or loans.

Once opportunities have been identified, this consortium, which could be led by the International Finance Corporation (IFC), would co-finance costs for feasibility analyses, technical mappings, and economic assessments, thereby reducing risk for companies and partners. This consortium would also serve as an information sharing platform for stakeholders to exchange sensitive, but non-proprietary, information that might accelerate the development of other projects.

Risks associated with pre-project development can also be mitigated through the development of regional or country-specific studies that deepen companies’ understanding and trust in the feasibility of gas-recovery projects. As some gas utilisation projects could benefit nearby facilities, a broader regional or basin analysis of potential opportunities could prove more valuable than examining each facility in isolation. These studies could be co-sponsored by the “You Collect We Buy” initiative or the World Bank’s Global Flaring and Methane Reduction Partnership, as well as by company-led initiatives such as the OGCI.

Mitigating project risk is also closely linked to marketing and certification schemes, which will be discussed further below. Commercial incentives, as well as clearly defined criteria for certifying the project’s gas, play a role in incentivising project development and guaranteeing projected revenues. The clearer the business case and the path to the project’s success, the less risk it will face.

Building visibility of past gas-capture successes

One take-away from the case study focusing on Egypt was the importance of celebrating successful past projects as a way to build momentum for new projects. The “You Collect We Buy” initiative could initiate a platform to provide visibility to completed projects, with a view to exploring potential synergies or emulating successful models. This could be created as an online platform, where non-proprietary details of past projects can be shared between companies, financial institutions, and governments that have committed to join the “You Collect We Buy” initiative. Capterio published a paper on the importance of celebrating successful projects, as well as a paper on past successes in Egypt.

Conclusion and next steps for pre-project development and identification

Identifying and developing technically and financially feasible projects is the first step towards recovering and marketing gas that would have been otherwise vented or flared. Due to the costs and associated risks, securing the funds and buy-in for a project to be developed can be an uphill battle, particularly when there is a lack of quality data on existing flare volume and methane emissions, and thus uncertainty about the potential returns from the project.

Tackling these issues requires a multipronged approach to improve the quality of emissions data, and then build engagement across the company to guarantee the visibility of this data at each level of management. Moreover, building alignment amongst JV partners in support of gas recovery projects and methane reduction is imperative. While much of this engagement must be done internally within companies, “You Collect We Buy” can build momentum in the short-term by creating a platform to increase the visibility of successful projects, which could drive engagement through increased awareness.

While a risk-sharing consortium could prove useful to support project development financing, this will likely fall outside of the scope of the “You Collect We Buy” initiative due to the core competencies of the European Commission, raising a key question as to who would lead this initiative.

Table 1: Barriers and solutions to pre-project development and identification

| Challenge | Solution |

|---|---|

Project-development costs and risks | Risk-mitigation consortium Establishing clear demand and certification criteria Build alignment amongst JV partners |

| Flaring and methane emissions reduction not a priority or not on companies’ “radar” | Improve data quality, ownership, and visibility Improve engagement and communication across all management levels Flaring and emissions reduction targets; KPIs tied to bonuses |

| Sub-optimal asset performance | Improve capacity, maintenance programs, and equipment redundancy |

| Lack of awareness of gas-capture opportunities | Platform to celebrate successfully completed projects |

| Uncertainty about data on flaring volume or methane emissions | Metering of flares and/or monitoring flaring with satellites Satellite or other remote sensing measurements of methane vent and leak emissions. Transparent and consistent reporting of flaring, venting, and fugitive emissions. |

| Lack of technical skills and capacity | Capacity building and training across management and operations Leverage technical expertise of JV partners Join regional and/or global initiatives |

Barriers to economic feasibility and financing

Barriers: What are the most common financial challenges holding gas-capture projects back?

Once potential projects have been identified and scoped, the most important factors that determine whether it will move forward are the project’s initial capital expenditures (CAPEX) costs, annual operating expenditures (OPEX) costs, the net revenues that the project may generate and whether the investment costs could deliver higher returns if invested elsewhere. In most cases, the economic viability of a project is first determined based on whether it demonstrates a neutral Net Present Value (NPV),14 effectively meaning that it will bring in as much revenue as costs. Even when projects have neutral or negative costs, however, they are weighed against potentially more profitable investments, creating a need for additional incentives.

Several factors determine a project’s NPV and overall profitability, such as tax and profit sharing regimes, long-term operational challenges, the state of regulatory enforcement and penalties, the use-case for the gas itself, and the cost of capital to finance the project itself. In some of the potential projects analysed in the workshop’s case studies, projects were economically viable before taxes, however incurred net losses after taxes would be applied. Across this suite of examples, a project’s estimated internal rate of return could decrease between 5% to 8% after tax assessments, which may be too costly in regions that face higher borrowing costs and harsher risk assessments.

A project’s eligibility for carbon credit or climate finance schemes can also impact its overall net cost, although these schemes only provide financial support after a project has been implemented and carbon credits have been issued and sold. This creates a need for bridge financing as CAPEX financing is needed several years earlier. Furthermore, carbon credit schemes have strict additionality requirements restricting support to projects that wouldn’t be possible otherwise. Marketing carbon credits coming from the upstream oil and gas sector can also be challenging, and recent increased scrutiny on many of these schemes could exacerbate this.

Weak economic feasibility can be exacerbated by an ineffective regulation, which may aim to require a prescriptive or target-based measure to reduce emissions, but ultimately fails to do so. The effectiveness of a regulation may be diminished by a limited scope, lack of coordination between government agencies, or a lack of independent oversight and enforcement. Lack of enforcement can distort potential opportunity costs of not addressing methane emissions – if penalties on methane leakage and flaring are too low or not enforced, the net cost of the project is automatically increased, making it less attractive. For example, in Nigeria it was estimated – based on data reported by Nigerian authorities – that the government has under collected flaring penalties on the scale of several hundred million USD per year.

Another factor that impacts the economic feasibility of the project, which ties into the following section on marketing and certification, is the use-case of the captured gas. Captured gas can be effectively used in multiple ways, for example providing on-site electricity, supplying domestic gas markets, or supplying exports for buyers abroad.15 The use-case determines the project’s potential revenues and net cost, and it may be impacted by the producing country’s current energy mix and demand. Consequently, in the absence of an opportunity to export the gas, a low market value of gas in domestic markets can impact the economic feasibility of projects, whereby investment costs of a gas-recovery initiative may not be recovered.

Barriers: What are the obstacles to financing a project?

Another financial barrier discussed during the workshop – which can also tie into the estimated economic feasibility of a project – is potential high costs for companies to borrow the necessary capital. In most JVs, based on previous projects, IOCs are responsible for providing the CAPEX of the project and borrowing the funds required, whereas National Oil Companies (NOCs) typically hold ownership rights to the gas or infrastructure. Profit-sharing agreements are generally required, whereby the IOC can obtain a profit from recovered gas. In these cases, it was emphasized that bridge financing is often imperative when ownership of the gas lies with the asset owner, as it can be difficult for investors to commit when ownership and revenue are divided.

For IOCs, the pool of available lenders willing to lend the necessary CAPEX has grown smaller in recent years. With many multilateral development banks (MDBs) cutting financing for projects in the fossil fuel sector or introducing strict prerequisites that require projects to fully align with the Paris Agreement’s objectives, accessing inexpensive capital is inarguably more challenging than in the past. For example, the European Investment Bank (EIB) has ended all its fossil fuel related projects, and while the European Bank for Reconstruction and Development (EBRD) notably financed flare-reduction projects in Russia and Egypt in 2009 and 2015 respectively, it has not financed similar projects in recent years.16

While gas recovery projects inherently result in a net emissions reduction, the potential need to build new pipelines or infrastructure to put associated gas on the market often triggers internal alarm bells. Banks and investors are concerned with inadvertently supporting fossil-fuel lock-in, whereby companies could use the new capital on their balance sheet to divert other funds to further fossil fuel expansion, thereby resulting in a net increase of methane emissions.

Therefore, for several MDBs, current rules would require that new infrastructure doesn’t process new oil or gas, as this would not meet the 1.5 degree Celsius carbon budget. In some cases, providing financing could be conditional on a company’s commitment to net zero. Even with such potential commitments, reputational risk and shareholder views must also be taken into consideration.

Solutions: How can stakeholders increase the economic feasibility of gas-capture projects?

Addressing the challenges associated with financing gas recovery projects starts with a simple first step – reducing the total net costs and maximising its economic feasibility and bankability. The World Bank’s GFMR,17 which aims to collect $255 million USD from donors, will be an important partner in this regard. The GFMR will provide grants that can typically cover 5%-10% of a project’s CAPEX to help it achieve a neutral NPV, making it financially viable, and more broadly will focus on data collection and analysis, project identification, skills development, and financial mobilisation.

Other stakeholders, including the governments hosting oil and gas operations also have a role to play, notably by revising tax policies with carve-outs specifically designed for gas-recovery projects, and by developing and enforcing effective regulations. For companies with large operations, where associated gas revenues may add just a fraction of a decimal point to overall revenues, regulations may be the only useful incentive to get companies to consider it seriously.

Governments can also support the development of voluntary carbon markets and carbon credit programmes, which can help cover project costs, increase their economic viability, and facilitate rapid project implementation. Existing carbon credit programmes, such as the one currently negotiated under Article 6.4 of the Paris Agreement, can be leveraged for flaring, venting, and LDAR projects. Due to challenges marketing credits coming from upstream oil and gas, the way in which these credits are promoted on carbon markets requires specific attention, especially regarding how potential “additionality” is defined and measured. This could be addressed by providing assurances to the buyers of the carbon credits, such as through a specific certification linked to the “You Collect We Buy” initiative.

Further clarity on the provisions under Article 6.4 of the Paris Agreement could support wider eligibility of gas recovery projects in compliance markets, such as ETS schemes. The Article 6.4 Supervisory Body could do this as it reviews and revises existing project evaluation methodologies under the Clean Development Mechanism (CDM), as part of the transition to the new Paris Agreement Crediting Mechanism. Specifically, this would mean swiftly revising the existing CDM methodology for recovery and use of gas from oil fields that would otherwise be vented or flared18 and securing the eligibility of these projects in the new centralised crediting mechanism.

Solutions: How can stakeholders increase the availability of inexpensive capital for gas-capture projects?

Three potential solutions could increase the availability of inexpensive capital, while also maintaining high consideration for lenders’ evolving climate and environmental standards. First, MDBs and other investors should revisit broad measures prohibiting investment In the upstream oil and gas sector, and create a set of criteria for methane abatement projects that could be eligible for financing. These criteria can include conditions, for example restricting funds from projects that would contribute to fossil-fuel lock-in, or any oil and gas extraction that would not have otherwise occurred. Changing these internal policies will require cultivating a deeper understanding of the near-term impact of methane emissions, and the high climate cost of inaction.

The second solution would be to consider bulk sovereign lending directly to partner governments. This would envision lending a significant amount, for example between $500 million to $1 billion USD, to a country with upstream operations, in exchange for flaring and methane emissions reductions. This solution would support more flexible financing of smaller methane-abatement leak projects, which can cost as little as $50,000 USD, and require aggregation.

Sovereign lending could also envision supporting complementary investments in alternative renewable energy production, allowing for partner countries to reduce pressure on domestic demand and allow for the export of surplus gas volumes.

The third solution proposed would be to develop sustainability instruments and bonds to provide loans directly to companies, which would provide programmatic funding under a set of conditions to meet specific methane reduction targets, whereby interest rates and capital costs are tied to meeting annual targets. This framework could be developed around absolute emissions reduction targets, as well as prescriptive measures mandating the implementation of best practices.

Sustainability instruments offer more flexible programmatic funding rather than project-based funding, albeit with more strings attached related to company performance in terms of reducing methane emissions. These instruments could also mitigate investors’ increasing concerns of methane leakage, as companies would be required to reduce their overall emissions, regardless of the outcome of a specific project.

Graphic 4: Cost-benefit analysis of selected LDAR gas-recovery project

Size and scale: Specific challenges financing fugitive emissions projects

Projects to reduce vented and fugitive typically require less financing than flare gas capture projects, however the size and quantity of potential projects can play a role in securing financing. One of the workshop’s case studies focused on developing projects for fugitive and vented emissions, which looked at past and potential projects in Azerbaijan and other undisclosed locations. As illustrated in graphic 5, potential captured gas volumes from these sources are significantly lower than flaring, at 76 BCM for venting and 31 BCM for leaking, globally. However, while such projects deliver smaller quantities of gas than flare-capture projects, there are a far greater number of potential projects, often with relatively low CAPEX costs. Harnessing this opportunity can be difficult, as a large number of small projects is harder to finance and develop, and less appealing to development banks.

In the case study example focusing on developing projects for fugitive and vented emissions, which looked at past and potential projects in Azerbaijan and other undisclosed locations. Due to smaller gas volumes recovered, these projects may also be perceived as financially unattractive. In this case study, two completed projects were only financially viable due to upstream emission reduction credits (UERS), which provided revenue for the first year to kick-start the projects. In the first project, which recovered gas through systematic LDAR, CAPEX costs were less than $200,000 USD and OPEX costs $200,000 USD per year for 0.005 BCM of gas, bringing abatement costs to $ -1.1 per ton of CO2 equivalent. LDAR projects require significantly less upfront capital costs as the main expense is purchasing equipment such as optical gas imaging cameras and training staff to detect leaks, with subsequent operating expenses arising from regular surveys and repairs.

In the second project, which recovered gas by mitigating emissions from storage tanks, CAPEX costs were estimated at $5.5 million USD and OPEX costs at less than $400,000 USD per year for 0.0095 BCM of gas, bringing abatement costs to $10-20 USD per ton of CO2 equivalent. While abatement costs are negative in the first project, and low in the second, these projects typically may not be attractive to operators without additional incentive.

Graphic 5: Comparison of available gas volumes from flaring, venting, and leaking

Conclusions and next steps for mobilising financing

Addressing financing challenges for gas recovery projects requires a multifaceted approach. In many cases, net project costs must be reduced, through possible grants, tax breaks or subsidies, and proceeds from carbon credit markets.

Second, costs of capital must be reduced, with inexpensive financing made available to support CAPEX costs. This is increasingly challenging due the propensity of MDBs to avoid providing any financing for the fossil fuel sector due to climate and reputational risks. However, these obstacles can be overcome in three ways. Banks can change restrictive policies to create exceptions for abatement projects, consider sovereign lending streams directly to governments, including investments in alternative clean energy sources, or they can consider sustainability instruments to provide financing tied to specific flaring or emissions reduction targets. Private finance can be similarly mobilised through bonds tied to specific performance indicators.

Considering the noted reputational risks associated with directing financing towards the upstream fossil fuel sector, both solutions would benefit from a public communication effort to clarify how gas-recovery projects can slow near-term warming and potentially prevent new greenfield expansion under the right conditions. This could come in the form of a political agreement between MDBs and their major shareholders, companies, and partner governments to acknowledge the near-term impact of continued methane emissions, with a commitment to rapidly finance gas-recovery opportunities.

| Challenge | Solution |

|---|---|

Economic feasibility and net project cost | Leverage GFMR for projects struggling to achieve neutral NPV Improve tax regimes Leverage climate offsets and climate finance |

| Lack of interest in carbon credits coming from upstream oil and gas | Providing assurances to buyers of carbon credits, such as through a certification of emissions reductions and guarantee of the project’s participation in the “You Collect We Buy” initiative |

| Investor concerns over financing fossil-fuel lock-in and lending stipulations | Sustainability instruments to tie funds to methane reduction targets Sovereign lending to governments Banks set conditions for financing exemptions for gas-capture projects |

| Investor concerns related to reputational risk financing upstream oil and gas | High level political agreement on role of gas-recovery projects in slowing near-term warming |

| Sheer number of fugitive emissions projects | Bundle smaller projects together to facilitate financing |

Barriers to marketing and building demand

Barriers: What are the challenges to creating a sustainable market for abated gas?

Creating and sustaining market demand for gas that would otherwise be vented or flared presents several challenges, starting with the development of a reliable certification scheme that buyers can rely on for assurance of their purchase’s credibility. The process of certifying such gas, proving its trustworthiness to buyers, and avoiding double counting while tracking physical volumes, are key obstacles that must be addressed.

The certification process for abated or lower-intensity gas is notably time-consuming and complex. For example, in the United States, certification efforts began four years ago, with the first entities achieving certification only two years ago. This timeline underscores the substantial time investment required to establish a credible certification system, which must develop the trust of buyers and regulators.

A challenge that the certification system must address is the risk of double counting. This occurs when the same volume of gas is recorded multiple times in different parts of the supply chain, effectively resulting in multiple sellers advertising and taking credit for the same supposedly abated or low-intensity gas. Nevertheless, accurate tracking of specific volumes across complex and global supply chains is difficult. While it is not possible to trace physical gas through systems due to intermingling in pipelines, establishing systems that can monitor and verify the flow of money from purchaser to producer and thus ensure that incentives flow to those truly investing in capture of gas without double counting is critical. Failure to do so risks crippling the credibility of the certification scheme and creating a dangerous potential for net increase of greenhouse gas emissions.

According to the workshop’s participants, credibility risks are a major concern for buyers in the market for abated or low-intensity gas. If the certification process is not perceived as robust and reliable, buyers will be reluctant to participate. Ensuring that the certification is perceived as methodologically sound is therefore crucial, which can be challenging in the absence of clear emissions and flaring data. The slow uptake of MMRV frameworks in particular poses a serious challenge to certifying projects in many countries.

Finally, beyond the establishment of a robust certification scheme, creating the necessary demand from buyers, as well as the marketing of recovered volumes of gas may also face significant barriers. For example, in the absence of strict regulations requiring importers to report emissions and flaring, or pay fees for cargoes with methane intensities above a certain threshold, buyers may not be sufficiently incentivised to purchase low-intensity or abated gas. Buyers’ decisions can be complicated by contractual hurdles, particularly when volumes need to have a range of allowed uncertainties.

Optimising surplus energy between exports and national demand

Export and marketing of surplus gas volumes may also be complicated by energy demand in the producing country. With energy demand increasing in several emerging economies around the world, optimising the division of surplus energy between potential exports and domestic use is vital. This optimisation merits scrutiny because of the potential risk that countries increase their use of higher-polluting fossil fuels for domestic consumption to allow for increased gas exports, thereby resulting in a net emissions increase. In the workshop’s case study that focused on Egypt, it was noted that Egypt moderately increased oil consumption for its power-generation in 2022 to allow for higher gas exports.

It was recently announced that Egypt was looking for over 17 LNG cargo deliveries in 2024 to meet its energy demand, putting the ideal allocation of any surplus gas volumes into question. In situations such as these, which could arise with any producing country, efforts should be made to ensure domestic supply while also meeting export demand for surplus volumes – without sparking unintended consequences, such as increased domestic oil consumption for power-generation, resulting in a net increase in emissions. This would require increasing investment, deployment and substitution of baseload renewable energy, or improving the efficiency of gas-fired power generation.19 It should be noted that across Africa, integrating variable renewable energy into power girds remains problematic, and therefore substituting baseload gas for variable renewable energy can present negative secondary consequences.

Solutions: What are the building blocks of a credible yet flexible certification system?

To address these challenges, several solutions have been identified. Implementing hybrid systems that combine tracking with digital tokens or certificates is one promising approach. These systems would enable the tracing of gas from production to end-use using purchase and sale agreements, without the need to track molecules physically. By linking certificates to specific quantities of gas and ensuring these certificates are only used once within the market, hybrid systems can help prevent double counting and maintain credibility.

Graphic 6: Egypt’s gas consumption, production, and net potential export

(Analysis by Capterio, data from Energy Institute Statistical Review)

One practical example of a similar system is the Guarantees of Origin (GOs) electronic certificate system used in renewable electricity markets.20 In this model, companies like Microsoft and Google purchase renewable electricity for their data centres using certificates from wind, hydro, or solar power sources. Although these sources are not directly connected to their facilities, the certificates ensure that the amount of renewable energy equivalent to their consumption is added to the grid. The EU’s cross-border use of GOs to incentivise renewable energy use should not be overlooked. A legal framework for GOs is set out in the RED II Directive, which mandates that Member States create national frameworks for the issuance and transfer of GOs.21 Similar concepts helped to kick-start the voluntary certified gas market in the U.S. in 2021, in which low methane certified producers can demonstrate their methane credentials to gas buyers such as utilities or large industrial users – tracked via attributes (certificates) in a digital registry, such as the MiQ registry.

This model can be adapted for abated gas, using certificates to verify that gas marketed truly originates from flaring and methane emission reduction projects. Such a certification system would build on a simpler “book-and-claim” model and involve connecting supply chain dots and verifying documents such as a bill of lading to establish a credible pathway from the project to the end-user. A centralized database tracking certificates could be set up to prevent misclaims and ensure no volume of gas is claimed twice for certificates.22

As noted above, any certificate is not worth the “paper” it’s printed on without trust, as buyers would need to justify their purchases to several stakeholders. To earn this trust, a robust certification system for methane emissions relies heavily on a MMRV framework, which is key to establish baselines for emissions reductions. This should enable the tracking of new emissions sources on a yearly or monthly basis and be further complemented with transparent and rigorous methodologies to continuously monitor, verify, and validate projects. It should be emphasised that in efforts to build trust with buyers, establishing these measures is only half the battle – it is also essential to educate buyers, requiring regular communication of benchmarks and continuous efforts.

A final element of the certification scheme previously discussed in the first section is the development of eligibility criteria – a clear scope for what can be certified is critical to unlocking project development. Defining the scope for projects under “You Collect We Buy” raises the critical question of whether only abated and non-flared gas should be certified, or all gas that meets a specific low-intensity threshold. Should certification only cover the former, a second question is raised as to how long gas emendating from a gas-recovery project should receive the certificate. Once a flare is abated, for example, there is a noticeable surplus in gas volumes, but over time becomes part of the steady supply.

Timeframes and future regulatory considerations

The EU Methane Regulation came into force in August 2024, and the various obligations on imported fossil fuels will come into effect in phases in the six subsequent years. Key milestones include:

- May 2025: data reporting requirements are enacted whereby importers will need to provide information on emissions and abatement measures associated with fossil fuels brought in from outside the EU.

- From 2027: importers must demonstrate that imported fossil fuels are compliant with the EU’s MRV requirements or meet an equivalent standard.

- From 2030, imported fossil fuels must meet a methane intensity performance standard.23

This timeframe requires consideration of the multi-year outlook of the “You Collect We Buy” initiative, as new regulatory standards should become standard operating conditions for all operators exporting fossil fuels to the EU. Abated gas may be less marketable in the EU after 2030, when all imports are required to meet an intensity standard. In the near-term, deepening stakeholders’ understanding of the forthcoming import standard could also be useful to develop the value proposition of certified abated gas, and build demand for the scheme and product. Effective education on the evolving global regulatory landscape will be essential to build engagement amongst buyers, suppliers, and partner governments.

Solutions: What incentives could be created for buyers to stimulate demand?

Developing a clear value proposition for buyers is essential to stimulate demand, which requires building awareness of the long-term benefits of purchasing low-emission gas. An illustrative example is the case of some European companies that emphasise the importance of proof of sustainability over the price of gas itself. This proof adds significant value within the established regulatory structure of the EU, showing a clear pathway for gas producers. However, achieving this goal remains a long-term objective, and significant efforts are needed to reach this level of market integration.

Environmental Social and Governance (ESG) practices and reporting in line with the Corporate Sustainability Reporting Directive (CSRD) are also factors influencing market dynamics. Many companies may adopt low-emission gas practices because they align with company values, while others may act to meet the pressure of investor and stakeholder expectations. Regardless of the incentive, however, companies are generally interested in proving and showcasing their sustainable decisions. Developing a Corporate Sustainability Reporting framework that reflects purchase of abated gas and efforts to reduce methane emissions could provide companies with these reputational advantages. While some companies will be motivated by corporate sustainability goals, others will require further economic incentives, such as tax breaks or subsidies to participate in the market for certified gas, or some form of mandate.

Creating a new market for certified gas involves several key actions, including regulatory support, economic incentives, and pilot projects. Regulatory frameworks that mandate certain standards for methane emissions can drive demand by ensuring compliance. Providing economic incentives, such as tax breaks and subsidies for buyers, can further encourage market participation. Educating both buyers and suppliers about the benefits and processes of certification is also essential. Detailed guidelines and workshops can help stakeholders understand the system’s importance and functionality.

Solutions: How can demand markets help incentivise development of gas recovery projects?

Demand markets could also potentially create economic incentives for producers in the form of price premiums for gas that meets certain sustainability criteria. These would need to be established by private stakeholders at their own will, as it would fall outside the competence of regulators or the European Commission to set a price premium. Nevertheless, the “You Collect We Buy” initiative could prove useful as a platform where buyers and sellers interact and mutually agree on price premiums. If a price premium cannot be established, it would be useful to establish a pre-sales agreement, whereby buyers commit to a price range they feel is adequate, sending a price signal to incentivise project development.

Initiating pilot projects in strategic locations can demonstrate the feasibility and benefits of certified gas. These projects can serve as proof of concept, showing that the systems in place can effectively track, certify, and commercialise gas that would otherwise be flared. To be most effective, pilot projects should focus on recovered gas rather than the entire production. This focus ensures only appropriate volumes of captured gas are certified, while aligning with the broader goal of reducing methane emissions. As part of these projects, continuous monitoring and performance evaluations are crucial to maintaining credibility and demonstrating effectiveness. Pilot projects should include meaningful information about the source of the gas, ensuring that the abated gas is clearly identified and tracked from production to end-use.

Conclusions and next steps for marketing and building demand

Building a sustainable market and sufficient demand for abated gas requires several components, including a credible certification scheme, a transparent platform to signal demand, and incentives for buyers to participate in the market. This requires a multifaceted approach and the active involvement of multiple actors, starting with building trust in the abated or low-intensity gas product, ensuring that gas volumes meet specific criteria and are not double counted. Hybrid certification systems that combine tracking with digital tokens/attributes could be a solution, but success will inevitably require stakeholders to commit to robust MMRV frameworks to create the foundation for credible emissions baselines. Successful pilot projects that demonstrably prove the effectiveness of the certification scheme will be essential.

Building demand amongst buyers for recovered gas requires further action. This requires continuous education as to the benefits of certified gas, which can range from meeting corporate sustainability goals, to meeting shareholder expectations, or a desire to be an industry leader in the fight against climate change. Buyers can also be incentivised by tax breaks, subsides, and evolving regulations. The ability for buyers to signal demand, and potential willingness to commit to a price premium, will be key to building upstream engagement in project development.

The “You Collect We Buy” initiative can develop, or support the development of, several of these solutions. In the near-term, project-development can be facilitated by encouraging clarification on the scope of gas volumes that are expected to fall under the umbrella of the initiative. While the creation of a certification scheme will fall outside the competence of the European Commission, the issuance of guidance and recommendations could be useful for other stakeholders to catalyse the establishment of the scheme.

Table 3: Barriers to marketing, certification, and building demand

| Challenge | Solution |

|---|---|

| Clear certification and tracking to avoid double counting | Implement a hybrid system that combines tracking with digital tokens |

| Difficult to build buyer trust in certification system | Ensuring all participants comply with MRV requirements compatible with the EU Methane Regulation Setting transparent eligibility criteria, baselines and verification processes Educating buyers of all efforts and evolving regulatory landscape |

| Lack of incentives for buyers to purchase low-emission gas | Economic incentives such as tax breaks, subsidies or price premiums Develop a Corporate Sustainability Reporting framework to reflect abated gas purchase and methane reduction |

| Need to optimise surplus gas between exports and national demand | Consider swaps, i.e. scaling investments and deployment of renewables to export surplus gas |

Final conclusions, recommendations, and outstanding questions

Gas recovery projects for legacy assets aren’t exactly new – successful projects have been developed and executed around the world over the past two decades. Despite these successes, it’s no secret that gas recovery projects aren’t wildly popular, apparent by the sheer volumes of gas that continue to be leaked, vented, and flared every year. Harnessing this opportunity could bring an estimated 267 BCM of gas to the market, over 70% of the EU’s annual consumption, and would deliver enormous climate benefits due to the powerful near-term warming potential of methane.

Unfortunately, this major opportunity isn’t sufficiently prioritised by companies, banks and governments. This is in part due to poor data on flaring and methane emissions, the lack of internal incentives to prioritise their reduction, and high competition from other company priorities. Even when gas-recovery opportunities are identified, project development can be expensive and carry risks, as there is no guarantee it will move forward. Projects often need buy-in from multiple joint venture partners, and they may need to overcome contractual hurdles related to gas-ownership or existing gas sale agreements. Building alignment between all partners and stakeholders is critical.

While the technical feasibility of many gas recovery projects is often certain, the economic feasibility is not – and it can be hampered by tax regimes, expensive borrowing costs, and ineffective enforcement of existing regulations. The financial incentive to invest in a project, or lack thereof, may be the most significant barrier for many companies, and this is inherently tied to the development of a sustainable market for gas that would have been otherwise vented or flared, including a credible certification system to track volumes, and the possibility for a price premium.

Taking the first steps towards capitalising on potential opportunities starts with understanding current market failures, building interest, engagement and coordination amongst key stakeholders, and deepening their understanding of available opportunities.

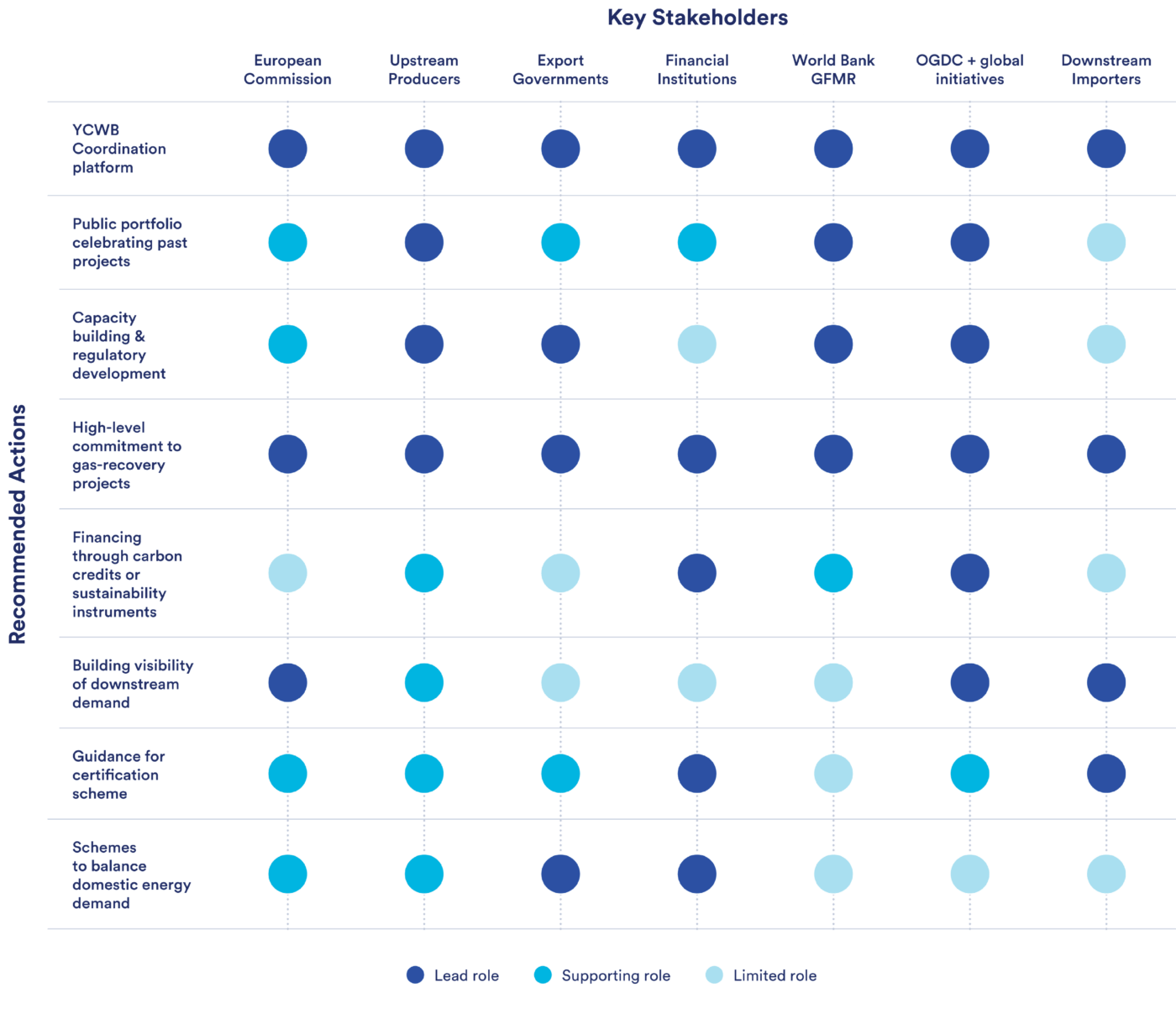

Inevitably, capitalising on these opportunities will require action from a number of stakeholders, there are several ways in which the “You Collect We Buy” initiative can enable the coordination and engagement required. In specific terms, the initiative could add value by leading or supporting the following activities:

Establishing a “You Collect We Buy” Coordination Platform: This platform would bring key stakeholders together on a regular or semi-regular basis, with the goal of identifying opportunities and removing barriers to their execution.

Building and promoting a portfolio of successful gas-recovery projects: This would highlight past successes, with a view to building interest in the attractive returns such projects can offer, as well as showcasing best practices in project design to improve uptake.

Capacity building and technical assistance to prepare for projects and develop regulatory frameworks: The initiative should focus on supporting development of regulatory MMRV frameworks and technological uptake in producing countries, including by partnering with the GFMR, international organisations and NGOs to lay the foundation for successful gas-recovery projects and the EU’s import standard obligations.

Securing high-level political commitments from banks, companies, and governments to prioritise gas-recovery projects: This could come in the form of joint statements or public commitments, which should leverage data to tackle negative perceptions around financing gas-recovery projects in the upstream oil and gas sector. This can include support for an investment framework, sustainability instruments, or carbon credits tied to specific commitments.

Providing visibility of downstream demand: This should be a principal function of the “You Collect We Buy” initiative and could come in the form of a transparent digital platform. This should allow producers to see demand prospects for abated gas and determine if there is a price premium available for the product.

Providing guidance for certification criteria: While the development of a certification scheme likely falls outside the scope of the “You Collect We Buy” initiative, guidance and recommendations could be provided for how such a scheme could be developed.

Schemes to balance domestic energy demand in producing countries: Gas exports shouldn’t compromise domestic baseload energy security. These schemes could propose or promote investments in gas-fired power generation efficiency and innovative energy swaps, where deployment of renewables that can provide baseload power is accelerated to allow for the export of surplus gas volumes.

Table 4: Matrix of recommended actions and competences of key stakeholders

Footnotes

- Analysis by Capterio based on data from World Bank (2024), IEA Methane Tracker (2024), and IPCC (2022).

- Revenue estimates depend on gas pricing. The IEA’s estimated in 2022 that the roughly 210 BCM of gas available in 2021 could bring revenues of $90 billion, based on higher gas prices. For more, see, IEA. “The energy security case for tackling gas flaring and methane leaks.” 2022. Available here.

- Throughout this paper, leaks are also referred to as fugitive emissions.

This is the GWP for fossil sourced methane. Non-fossil sourced methane has a GWP of 79.7 over 20 years, and a GWP of 27.0 over 100 years. Source: IPCC, more information available here.

IEA (2024). “Global Methane Tracker 2024.” Available here.

World Bank. “Global Gas Flaring Tracker Report.” 2024. Available here.

European Commission. “Press Release: EU Announces €175m financial support to reduce methane emissions at COP28”. 2023. Available here.

It is important to note that for most new greenfield projects, solutions to minimise or capture flared gas are generally considered.

The case studies covering Nigeria and Egypt were prepared by Capterio, and the case studies covering Azerbaijan and other undisclosed locations were prepared by Carbon Limits.

OGCI companies collectively reduced absolute upstream methane emissions by 50% and cut flaring by 45% for operated assets. For more, see, Oil and Gas Climate Initiative. “Tackling Methane Emissions.” Available here.

Methane Guiding Principles. “Resources: Joint Ventures”. Available here.

It was noted that starting pilot projects with joint ventures may resolve some contractual challenges, as associated gas and emissions are more likely to be co-owned.

Methane Guiding Principles has produced a number of resources for JV partners interested to help influence their partners to reduce methane emissions, including this Joint Venture Playbook. They have also produced a model GHG Charter to assist development of a written charter for JV governance committees, and a model GHG Board Resolution to manage and reduce emissions in JVs. For more, see Methane Guiding Principles. Influencing Partners. 2024. Available here.

Net present value is the difference between cash inflows and cash outflows, and is used to calculate a project’s projected profitability.

Value from captured gas can be created in several ways, for example used to power on-site operations and services, can be sold as pipeline gas, CNG or LNG, or be used to produce petrochemicals. For more information, see, Capterio. “Flaring – the $20 billion decarbonization opportunity.” 2021. Slide 14, available here.

Many gas-recovery projects financed by the European Bank for Reconstruction and Development can be found on their website, for example providing a $40 million loan to the oil and gas group Merlon Petroleum El Fayum in Egypt in 2015 and providing a €90 million loan to the Irkutsk Oil Company in Russia in 2009.

The Global Flaring and Methane Reduction Partnership succeeds the Global Gas Flaring Reduction Partnership, and is a multi-doner trust fund focused on helping developing countries cut carbon dioxide and methane emissions generated by the oil and gas industry. For more, see, World Bank. “GGFR to evolve to the GFMR partnership.” 2024. Available here.

UNFCCC. Methodologies. “AM0009: Recovery and utilization of gas from oil fields that would otherwise be flared or vented – Version 7.0.” Available here.

President Biden announced such an investment package at COP27. The EU, Germany and the US committed to provide a $500 million package to deploy 10 gigawatts of renewable energy by 2030, while also capturing 4 BCM of natural gas from flaring, venting and leaking. No further details on this package have been announced. For more see, The White House. “ Remarks by President Biden at COP27. 2022. Available here.

A Guarantee of Origin (GOs) is an electronic certificate that provides proof that 1 MWh of electricity has been generated from a renewable energy. A company that wants to use GOs for Corporate Social Responsibility (CSR) reports, or to simply back-up their renewable energy claims, would need to ensure that it has enough GOs in its portfolio to match its electricity consumption. These certificates can be purchased independently by companies, or bundled together with energy contracts.

For more, see Article 19 of the RED II Directive, at Journal of the European Union. “Directive (EU) 2023/2413 of the European Parliament and of the Council of 18 October 2023 amending Directive (EU) 2018/2001, Regulation (EU) 2018/1999 and Directive 98/70/EC as regards the promotion of energy from renewable sources.” 2023. Available here.

Under recital 89 of the RED II Directive, the European Commission is to set up a database to track and prevent double counting.

The EU’s obligations on imported fossils are detailed in Articles 27, 28, and 29 of the Methane Regulation. For more, see, Official Journal of the European Union. Regulation (EU) 2024/1787 of the European Parliament and of the Council of 13 June 2024 on the reduction of methane emissions in the energy sector. 2024. Available here.

Credits

Authors

Brandon Locke, Julia Kislitsyna, and James Turitto

Acknowledgements

This whitepaper builds on the elements collected during a workshop co-organised by the European Commission, the International Energy Agency, and Clean Air Task Force on 21 June 2024 in Paris, France. This workshop brought together a diverse array of stakeholders including oil and gas companies, industry experts, financial institutions, and NGOs in a dynamic roundtable centred around the implementation of the “You Collect We Buy” initiative.

The workshop sought to develop a robust understanding of the operational, financial, and market barriers obstructing gas-recovery projects, while also considering what solutions could resolve these challenges and lay the groundwork necessary for all stakeholders to seize the gas-capture opportunity. This workshop was followed by a series of follow-up meetings with participants, as well as additional stakeholders who could not attend the in-person meeting to further refine the whitepaper’s content and suggestions. This whitepaper, therefore, does not represent an endorsement of the entirety of its content by any of the organisations that contributed to its elaboration.

As the workshop was held under Chatham House Rule, there is no attribution to any participant, and the contents of this whitepaper reflect a summary of the discussions and recommendations put forth, and not necessarily the views of any specific contributing organisation. The authors and workshop organisers are deeply grateful for the time and contributions of the following participating organisations [in alphabetical order]: DiXi Group; Environmental Defense Fund; European Commission; European Bank for Reconstruction and Development; Capterio; Carbon Limits; ICA Finance; International Energy Agency; International Methane Emissions Observatory (IMEO); Islamic Development Bank; MiQ; Nigerian Upstream Petroleum Regulatory Commission; Oil and Gas Climate Initiative; Shell; State Concern Turkmengas; World Bank.

Featured in the Media

Euractiv Webinar: Developing an Implementation Plan for ‘You Collect We Buy’