Decarbonization Pathways and Policy Recommendations for the United States Steel Sector

Executive Summary

- Steel production is a significant greenhouse gas emitter, responsible for 2% of U.S. greenhouse gas (GHG) emissions, and 8% of global GHG emissions. To meet climate-change targets, the global steel industry must undergo significant decarbonization.

- The U.S. is already a leader in low-carbon steel production, with an average carbon intensity below that of other major producing countries. The ‘big four’ steel producers1 in the U.S. have recognized the need for further decarbonization, and all have pledged net-zero or near-net-zero steel production by 2050.

- Approximately 70% of the steel produced in the U.S. is made by remelting metallics, primarily scrap, in electric arc furnaces (EAFs). This is a relatively low-carbon route of steel production, which gives the U.S. a steelmaking carbon emissions intensity that is lower than other regions of the world. As electricity is the primary energy source for this process, further decarbonization via the use of clean electricity can be done with no additional capital spending or process changes. CRU estimates that converting current power consumption by all steelmaking (both EAF and integrated steel mills) to clean electricity would reduce carbon emissions by 35% from present levels.

- At the same time, the impurities found in scrap restrict the number of products that can be made using scrap; thus, 30% of steel continues to be produced by the blast-furnace-based integrated route. This route produces the highest-quality products that are sensitive to contaminants found in scrap.

- EAF production continues to take market share from integrated production, however, the volume and quality of scrap available is insufficient to fully replace integrated production for high-quality products. CRU estimates that roughly 30 Mt/y of high-quality ore-based metallics (OBMs) such as pig iron and direct reduced iron (DRI) will be needed to produce the forecasted volume of high-quality, low residual steel products. Even now, the U.S. imports roughly 5 Mt of OBM yearly for EAF production, and that will increase unless OBM production in the U.S. increases as well.

- Overreliance on imported OBM will increase the vulnerability of domestic steelmaking supply chains as well as export scope 3 carbon emissions, thus doing nothing to help with global decarbonization. A variety of policy measures could be implemented to counter this issue, such as tariffs or carbon taxes on imported OBM or requirements for federally funded infrastructure projects to use OBM produced in the U.S.

- Currently, high-quality OBMs in the U.S. are produced primarily in six operating integrated mills with coal-fired blast furnaces, along with three direct reduced iron (DRI) plants firing natural gas. To decarbonize the OBM process, production plants will need to be equipped with carbon capture and storage (CCS) systems or converted to DRI plants using green or low-carbon hydrogen. At current hydrogen prices, CCS is a more cost-effective technology and can provide significant carbon abatement (60% – 90%) but will struggle to provide full decarbonization.

- With decarbonization adding significant cost to the production process for a relatively low-cost, low-margin commodity material, some form of policy support will be necessary to provide additional incentives for decarbonization. Demand side incentives for green steel, such as requirements for green steel in federally funded infrastructure projects is one example. On the supply side, tighter environmental regulations such as those for hazardous air pollutants on integrated iron and steel production, as well as subsidies for lower-carbon production facilities are already underway. Carbon taxes, combined with a carbon border adjustment mechanism (CBAM) as used in the EU would be another option.

Decarbonization of the steelmaking process is critical to meeting global emissions targets

Steel is fundamental to economic development. It is an essential material in the construction of the consumer goods which maintain gross economic output, infrastructure like roads and bridges, and utilities that support existing and developing markets. Because steel production is essential to the economic success of the U.S. and many other countries, it would be unwise to lower emissions through a reduction in output or material substitution. Thus arises a need for realistic, economically sound abatement pathways which do not inhibit status quo manufacturing activity. The challenge lies in the fact that steel emissions are inherently difficult to abate due to the chemistry and physical constraints of the process.

The steel industry is a leading contributor to greenhouse gas (GHG) emissions, with iron and steel production accounting for 7-9% of global anthropogenic GHG emissions,2 and the U.S. steel industry accounting for 1-2% of total anthropogenic U.S. GHG emissions in 2023.3 Because of this, the industry has embarked on a challenging journey to reduce emissions through advancing carbon reduction technology and process efficiency. The pathways required to meet the “green”4 steel standard are complex and require further technological development. Thus, transition to a green steel market will require immense efforts from the entire steel value chain and support from policy makers.

The primary pathways for decarbonizing iron production involve either replacing natural gas with low-carbon hydrogen or capturing and storing CO2 emissions using carbon capture and storage (CCS) technologies. Low-carbon or ‘clean’ hydrogen can be produced through two main methods: electrolysis of water using low-carbon electricity, or the application of CCS to hydrogen production from natural gas. Each of these options present economic, operational, and emissions-related considerations that steelmakers must carefully evaluate. This report provides a review of the steelmaking industry in the United States, with a focus on current and future steelmaking pathways for decarbonization.

Regional dynamics and production methods in the United States steel industry

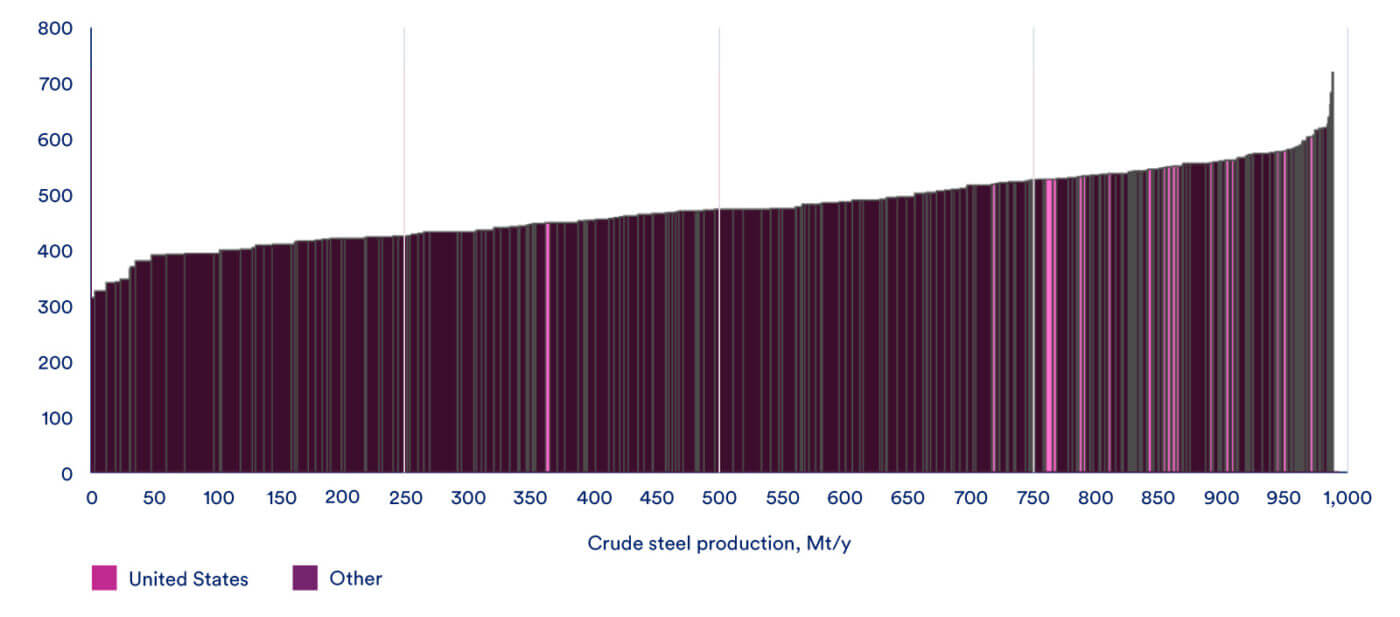

The United States steel industry is a well-developed, mature industrial market. In 2023, total steel demand in the U.S. was 88 million tonnes (Mt), equivalent to ~5% of the global market. The $100 billion industry sits below all other major steel producing countries on the global emissions curve found in Figure 13, but well above the global average site cost5 shown in Figure 1. This is, in large part, due to the value chain’s structure and the production routes it is built upon. Most of the crude steel (70%) is produced by remelting scrap in electric arc furnaces (EAFs). These facilities can be found all around the U.S., but a growing majority are in the South where scrap supply is strong, and manufacturing and construction demand is growing. The remaining 30% comes from integrated mills clustered around the Midwest and Great Lakes region. These are primary steelmaking facilities, which use the coal-fired blast furnace (BF) process to produce iron directly from iron ore, combined with basic oxygen furnaces (BOF) for steelmaking.

Figure 1: Global site costs, USD / t crude steel

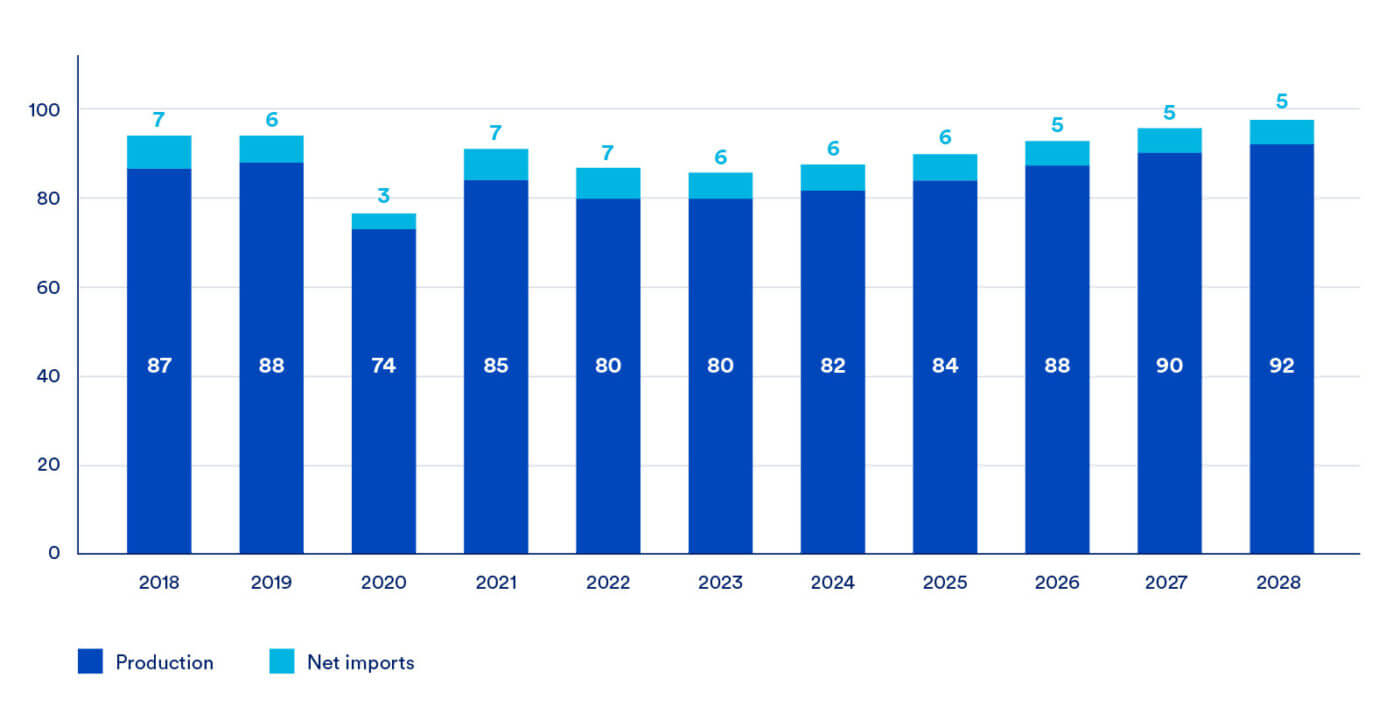

The United States does not produce sufficient steel to meet domestic demand and imports a net 8% of steel for domestic consumption.6 U.S. trade reliance occurs for a variety of reasons, including 1) the often-lower cost of imported steel, 2) tightly integrated United States-Mexico-Canada (USMCA) supply chains (the largest sources of imported steel are Canada and Mexico; these are also the largest importers of steel from the U.S.), and 3) the availability of semifinished steel for domestic processing.7 Imports also benefit from cost-effective transportation, as some regions may see lower transportation costs via ship-based imports rather than by trucking or railing from a distant U.S. mill. Although tariffs (including the 25% Section 232 tariffs8) have alleviated pressure to a certain extent on domestic producers, imports continue to maintain a significant share of the domestic steel market. Producing every type of steel may not be in the interest of the United States as comparative advantage strengthens cost and price structure. Using imports to fill supply gaps will continue to be a feature of the U.S. market in its current state, with the caveat that changes to tariff exemptions could raise costs of imports from Canada and Mexico.

Figure 2: U.S. finished steel production & imports (Mt)

Note: U.S. production includes finished steel products.

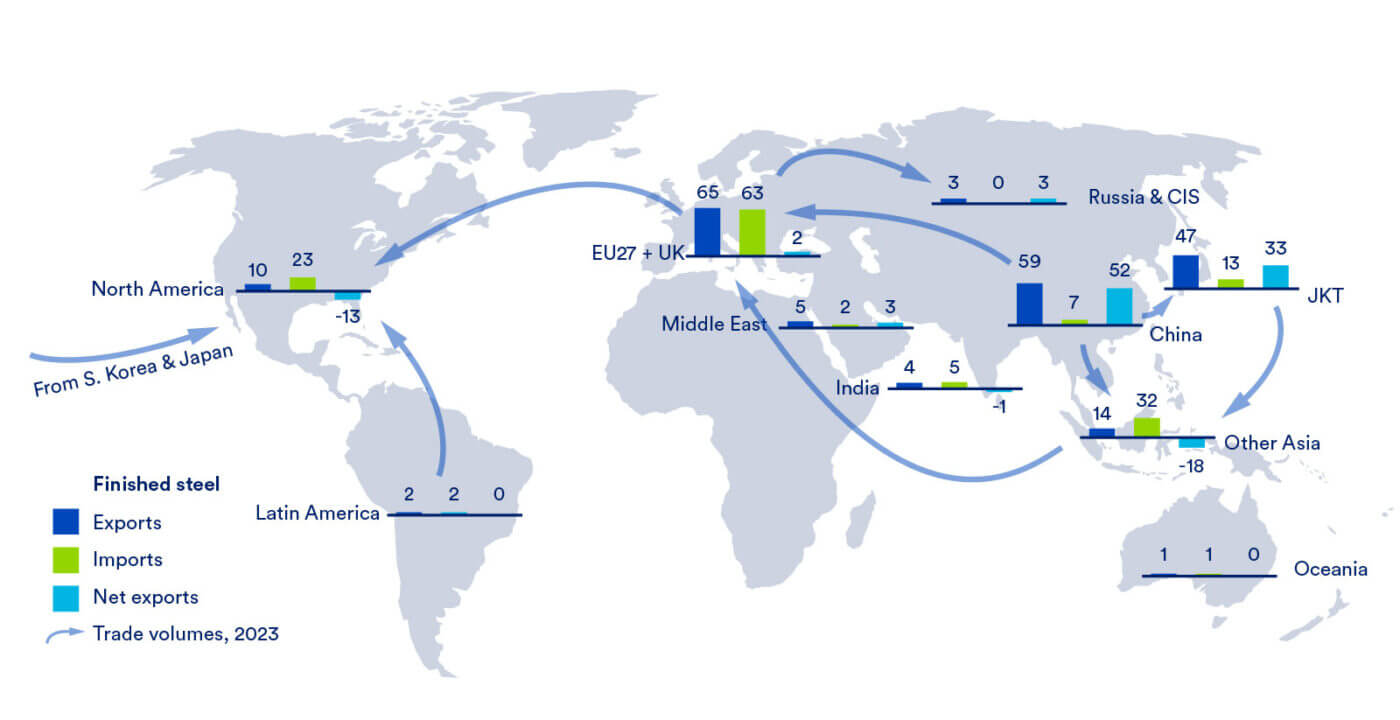

Figure 3: Global steel trade flows9 (Mt) 2023

As the carbon intensity of U.S. steelmaking is amongst the lowest in the world, imported steel and ore-based metallics (OBMs, produced directly from iron ore) are likely to have been produced via a more carbon intensive process. As a result, supply gaps in the steel value chain increase scope 3 emission levels for U.S. steelmakers that import these materials. Domestic content requirements of the Build America, Buy America Act10 will motivate reshoring, thus reducing import reliance, but its success is dependent on the replacement strategies steelmakers implement. If quality and origin standards drive the construction of new, domestic production capacity for OBMs, then emissions reduction will be realized. However, if scrap or OBM imports are used to fill the supply gap, the U.S. will effectively be importing foreign emissions, negating any climate benefit. Some regions (particularly Canada and the EU) are moving aggressively to reduce carbon emissions in steelmaking, which could alter U.S. trade flows to be more focused on reducing the average carbon content of the steel purchased.

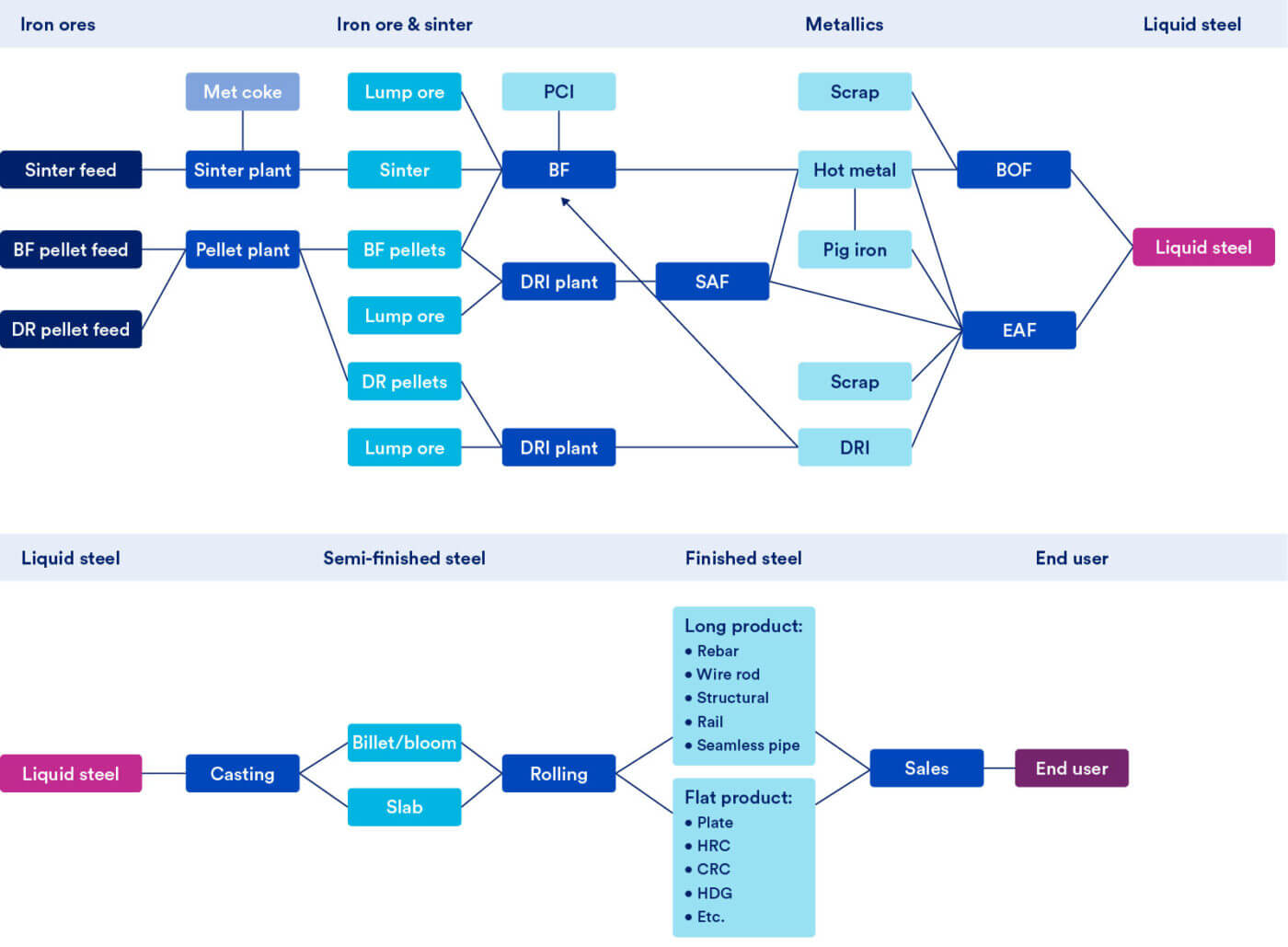

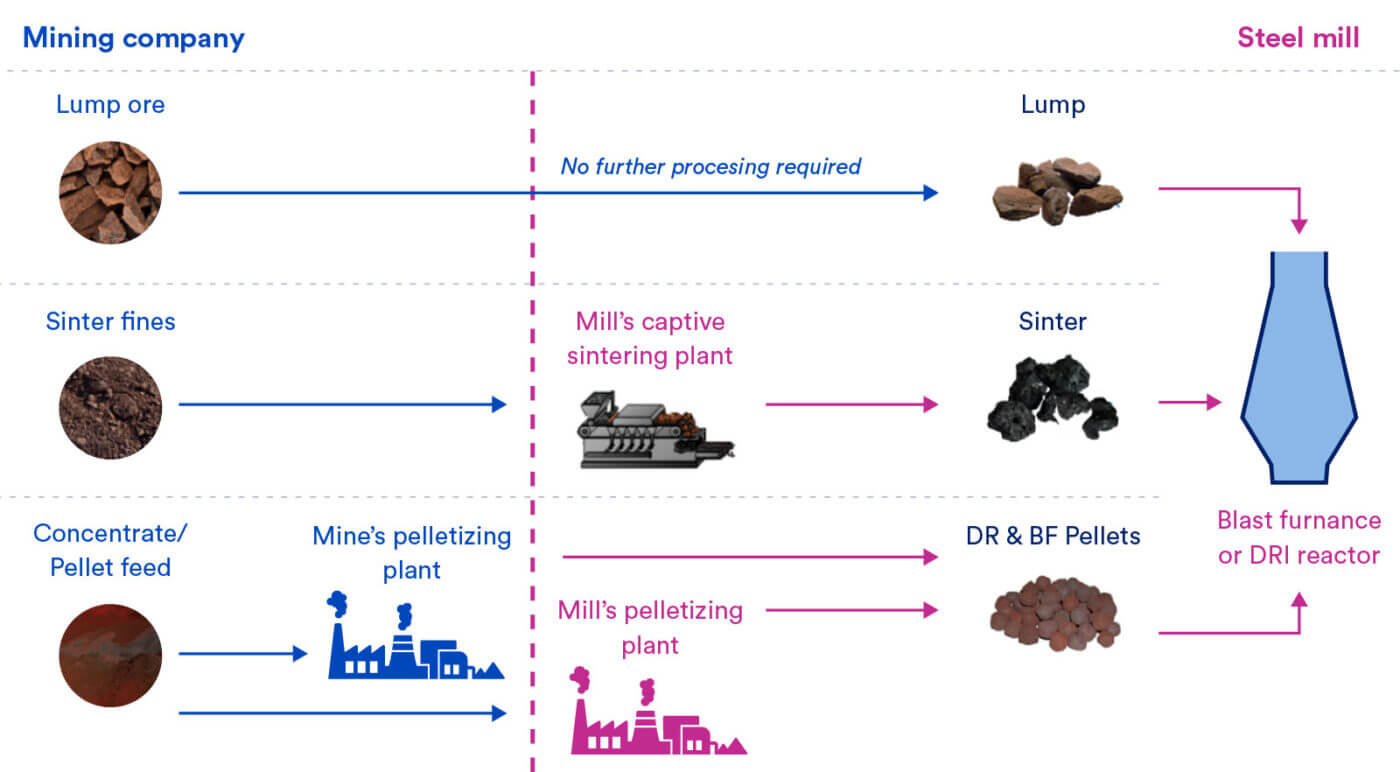

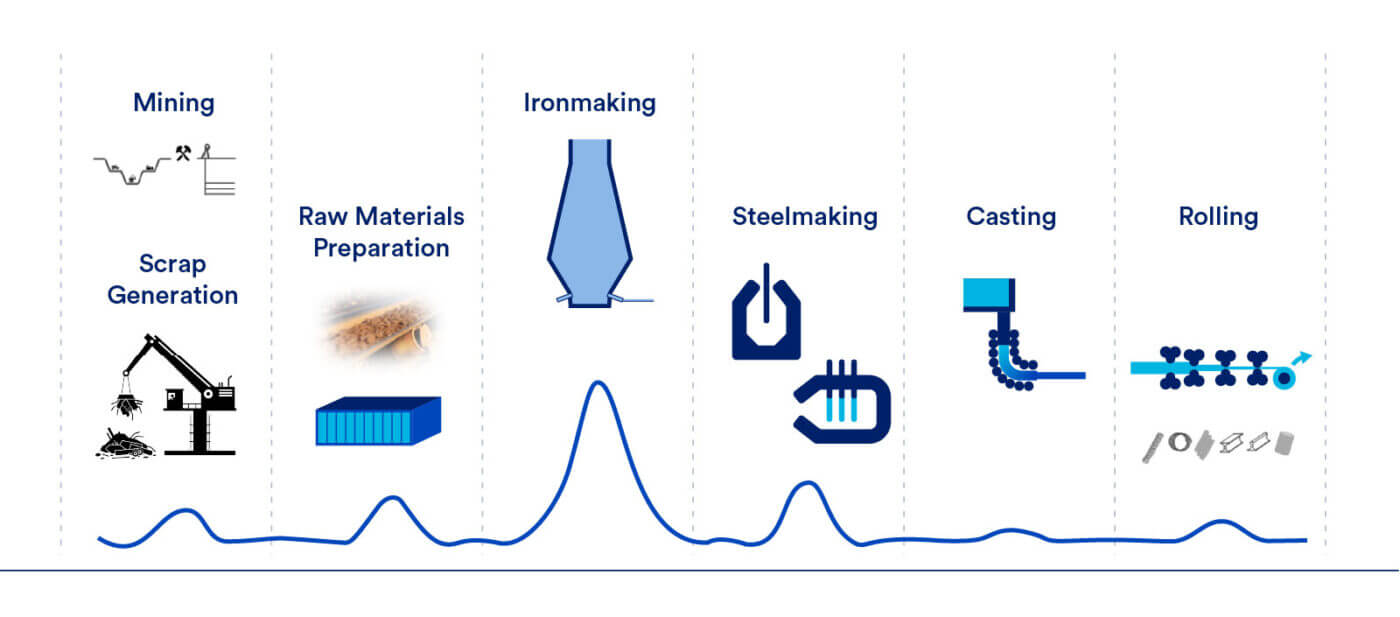

The following illustrations depict the steelmaking value chain: iron ore production followed by the ironmaking process (hot metal/pig iron and direct reduced iron (DRI)/hot briquetted iron (HBI)), and finally, the steelmaking process (via BOF or EAF).

Figure 4: Steelmaking value chain (left to right)11

Raw material processing methods

Production starts at iron ore mining and preparation, with some iron ore products requiring sintering or pelletizing before they can be used directly in a furnace. Compared to China, which uses sinter at a high rate, most iron units used in U.S. ironmaking are in pellet form. The pelletizing process differs between sinter, pellet, and other iron ore products as depicted in Figure 5 and can take place on site or at the mine, allowing for a more dynamic supply chain. Once transformed into its desired form, the iron ore is converted to liquid iron in a blast furnace to be used in integrated steelmaking; or is reduced in a direct reduction furnace to be used in EAF and submerged arc furnace (SAF) applications. Figure 6 and Figure 7 depict the ore to iron process.

Figure 5: Iron ore feedstock routes

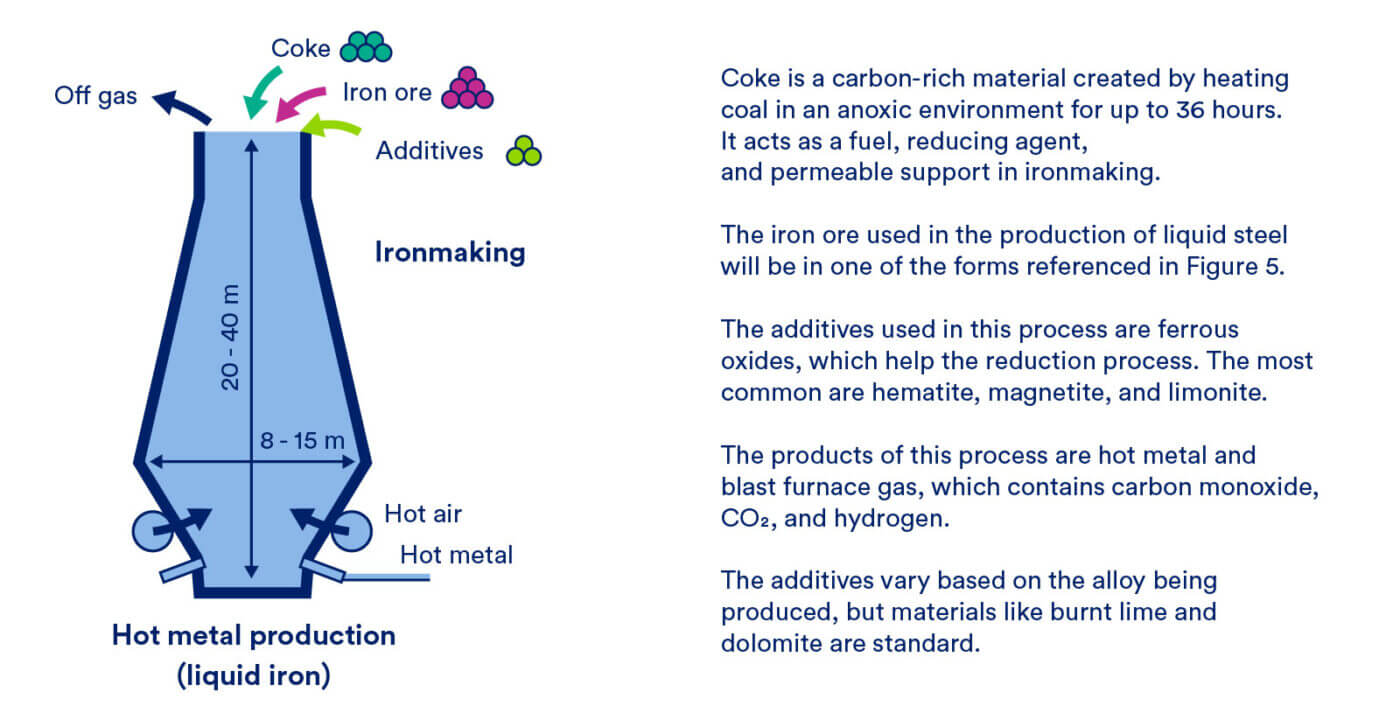

Figure 6: Liquid steel production in a blast furnace

In blast furnace (BF) ironmaking, iron ore, coke (a coal-based fuel), and flux are continuously fed into the top of the furnace, while hot air is blown into the lower section to enable chemical reactions which convert (reduce) iron oxide to elemental iron. This hot air is provided by hot stoves, which are fired with the ‘blast furnace gas’ produced by the furnace (pictured later in Figure 31). The blast furnace reduces the iron ore and removes impurities in a single processing stage. This stage produces the clean, higher quality hot metal or pig iron that will be used in traditional integrated steelmaking.

The blast furnace is a continuous operation that is difficult and expensive to slow or shut down. The lack of flexibility in operating a blast furnace is a significant detriment to the process, as mills are reluctant to take a furnace off-line during times of low demand due to the difficulty and cost of intermittent operation.

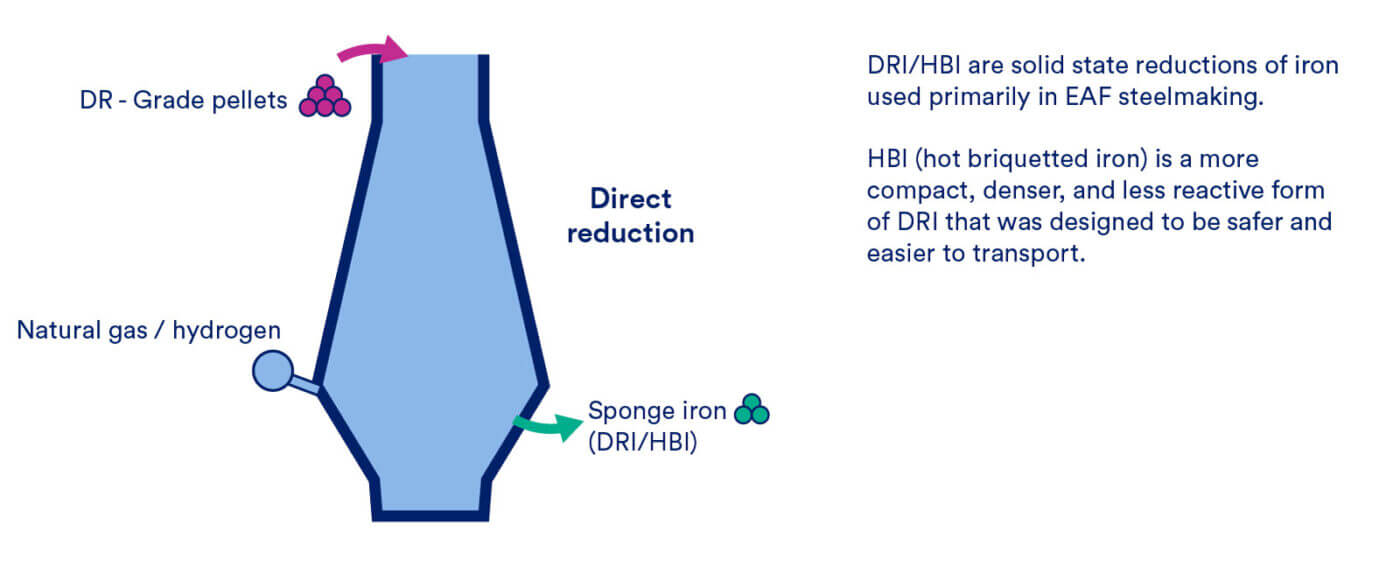

Figure 7: Direct reduced iron production

The direct reduction process differs from a traditional blast furnace in two key ways. First, the iron source for direct reduction, DR-grade pellets, needs to be of a much higher quality (67% Fe minimum). There are diverging pellet value chains, producing “high quality iron” at, or above 67% Fe, and regular or “low quality” iron below that level. These quality requirements are relatively inflexible, and facilities which choose to convert to DRI-sourced iron units must therefore also invest in DR-pellet production or outsource to the global market. Second, while a blast furnace utilizes coke to remove oxygen from the iron source, DRI uses a reduction gas (generally a blend of hydrogen and carbon monoxide). Although coal can be used as the precursor for the reduction gas,12 in the U.S. natural gas is exclusively used, with methane converted to hydrogen and carbon monoxide in a process known as reforming.

In contrast to the molten iron produced by a blast furnace, the process creates a solid ‘direct reduced iron’ product (also known as DRI) with a high iron content (>92%). Because DRI is porous and reactive to water, it can be difficult and dangerous to transport. Hot briquetted iron (HBI) is a denser, more compact, and less reactive form of DRI. HBI is created from DRI by compressing the hot (>650°C) DRI product into briquettes upon discharge from the furnace.Compared to a blast furnace, it is easier to slow, idle and restart a DRI plant. This flexibility is useful for steelmakers, as they can take short periods of downtime during periods of low demand. Plants in the United States have always operated at full capacity as demand for DRI exceeds current capacity. If DRI capacity exceeds potential demand in the future, plants will prefer to operate at a lower level for a longer period rather than toggle operation.

Steel production methods

Traditional basic oxygen furnace (BOF) steelmaking, or ‘integrated’ steelmaking is the globally dominant steel production route. Integrated steelmaking is a method in which the liquid iron (“hot metal”) from a blast furnace is charged with a small amount of scrap or OBMs and then refined into steel by blowing pure oxygen into the melt. With high-purity hot metal consisting of over 75% of the charge, the quality and cleanliness of the steel produced by this route is unsurpassed, allowing this process to supply steel for the most demanding of products.

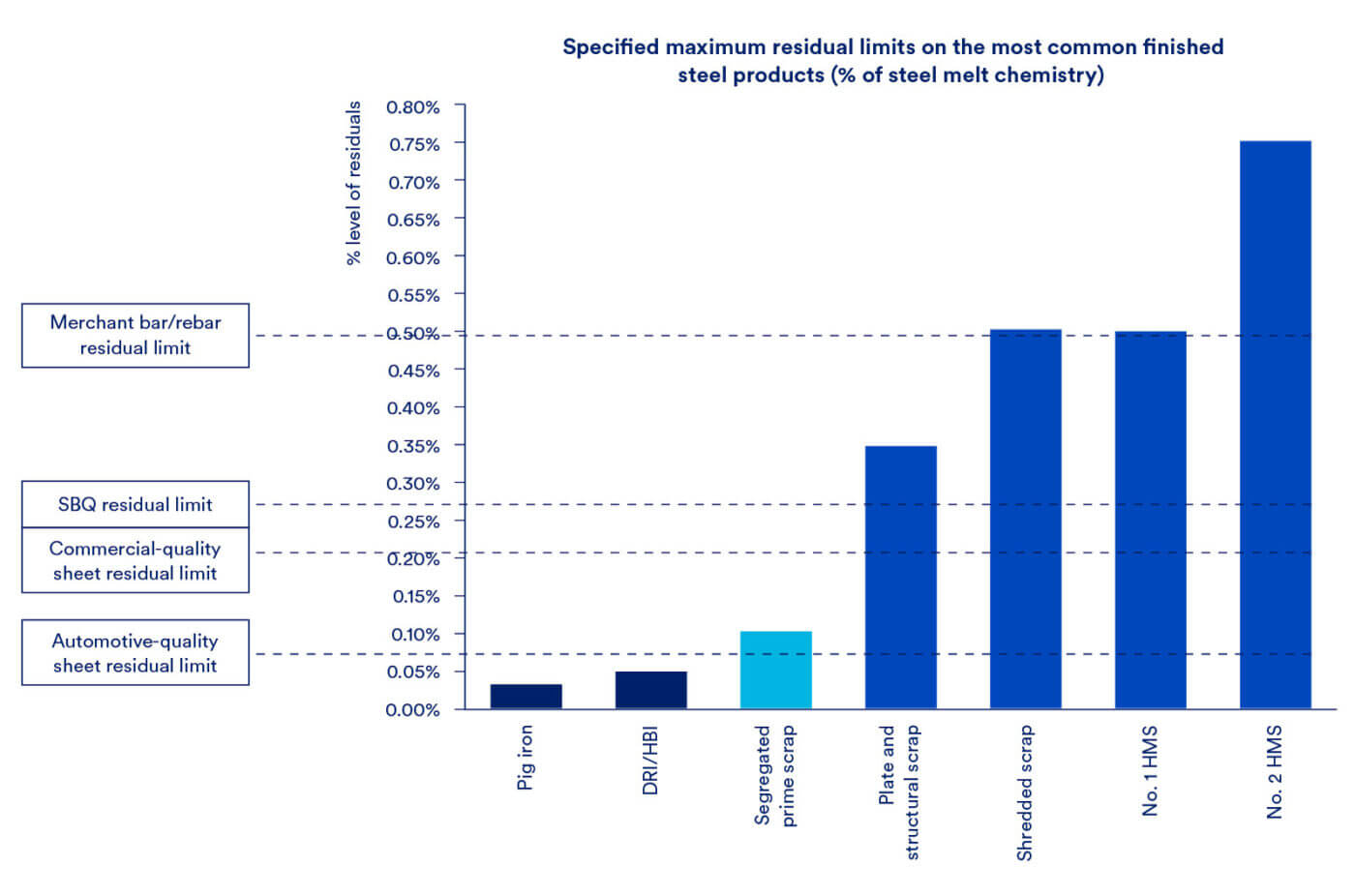

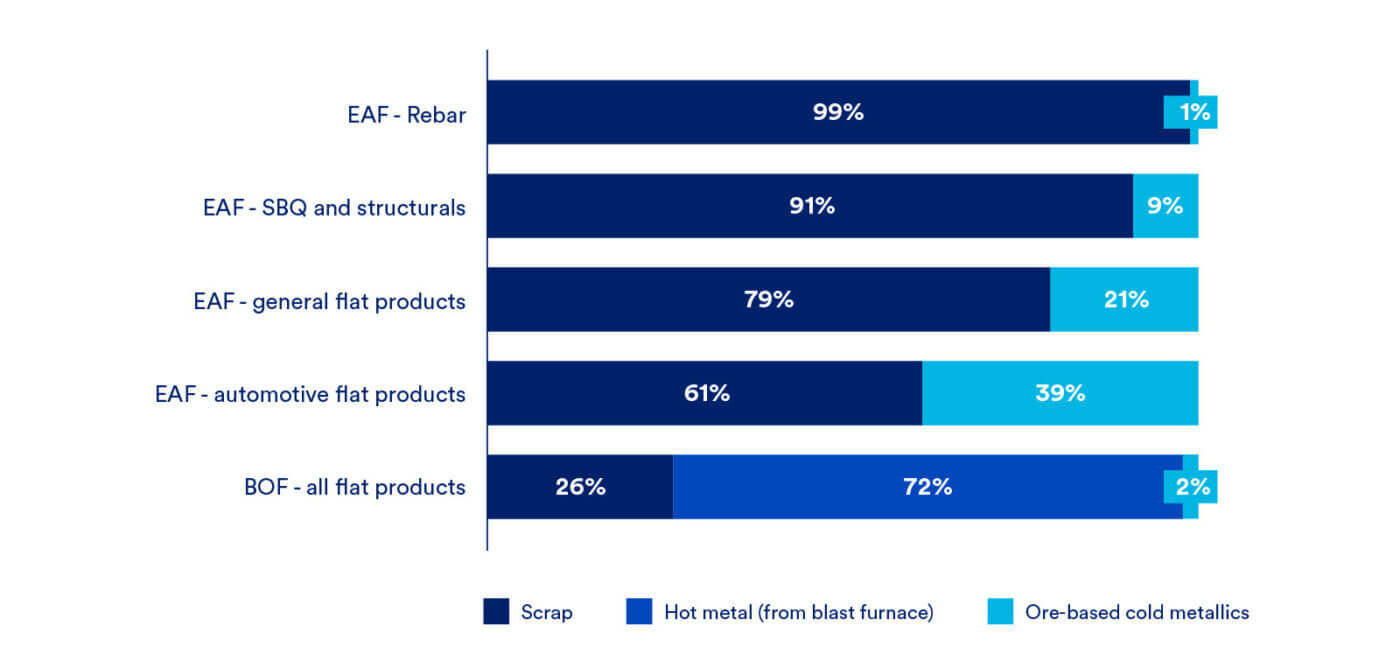

Electric arc furnaces (EAF) are the alternative processing route to the BOF furnaces used in integrated mills. They use electricity to melt scrap and OBMs like pig-iron and DRI to produce steel. EAFs are generally smaller than BOF facilities and service regional or localized markets. An EAF can produce steel using 100% scrap, but for non-basic grades of steel, such as those required for flat or special bar quality (SBQ) products, the addition of OBMs such as DRI/HBI is essential. This is because the level of residuals13 in non-prime scrap, and some prime scrap, are too high to maintain the desired melt chemistry for the desired output.

Figure 8: Specified residual limits for common finished steel products, % of melt chemistry (SBQ, special bar quality)14

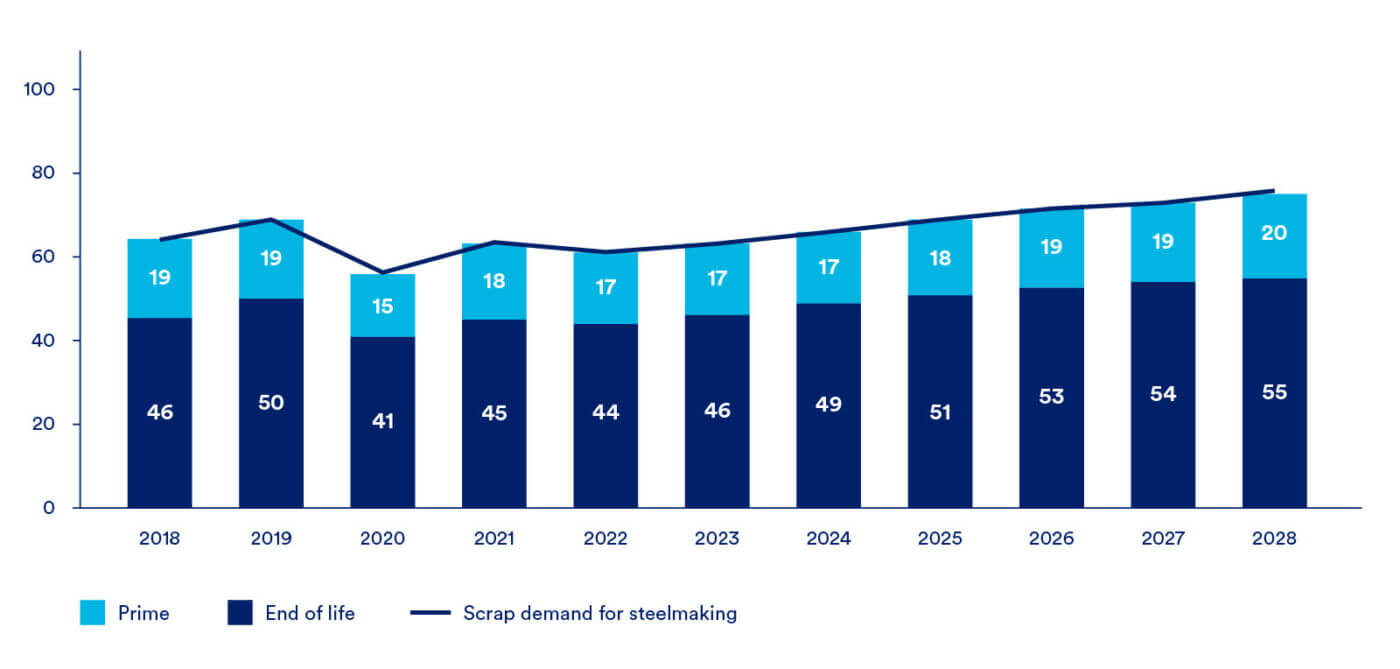

EAF steel value is directly correlated to the quality of scrap used in the steel-making mix. The quality of scrap consumed relates to its iron-to-carbon ratio, residual content, and the physical state or quality of the material. Thus, as EAFs increase their share of the market, the demand for cleaner, high purity scrap has risen. Not only does scrap availability restrict the expansion of EAF production, but increased scrap prices have incentivized mills to increase their DRI/HBI and pig iron consumption, much of which is imported. Continued growth in scrap demand will drive ongoing investments to increase collection and sorting efficiency, which will slightly increase the available supply of scrap; that said, there is likely not much more scrap to be collected. Later in the report, Figure 39 helps quantify the forecasted scrap availability and shows little to no increase over the medium-term.

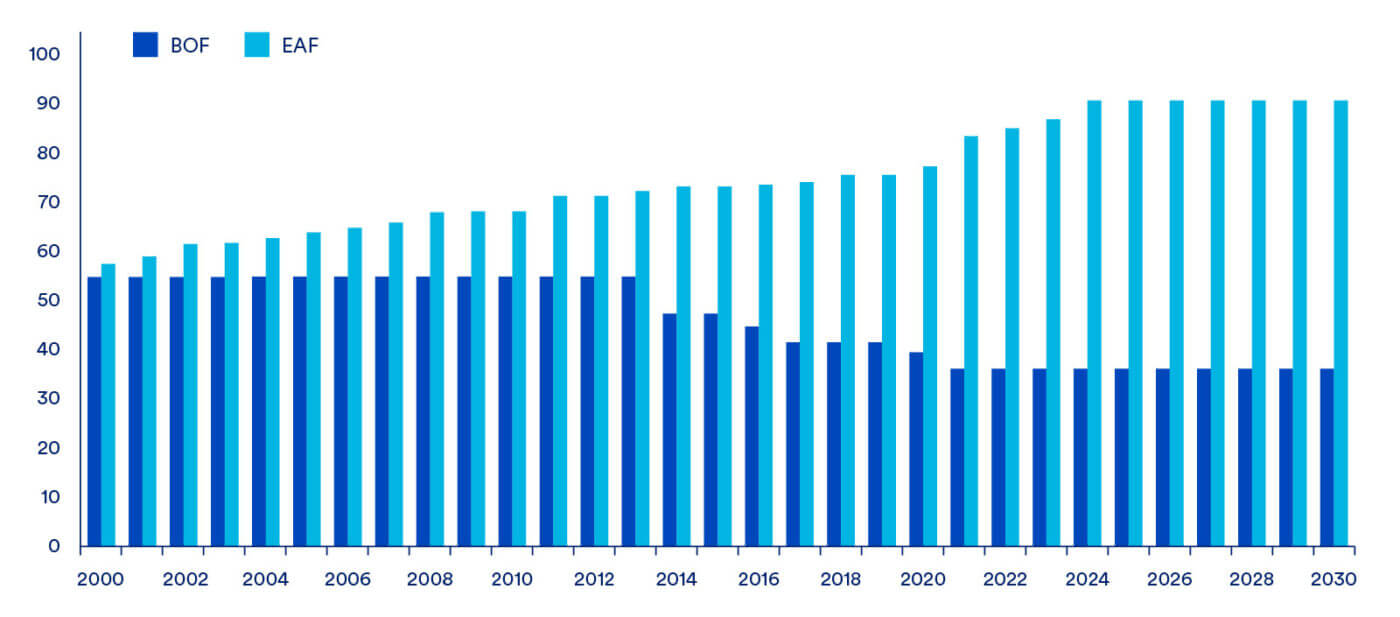

Crude steel production capacity for EAFs in 2023 was 85 Mt, while BOF capacity was 24 Mt. Over the past ten years, EAFs have overtaken integrated mills to become the main steel production route in the U.S. Availability of scrap being a key factor in this change in production.

Table 1: Advantages/Disadvantages of domestic steelmaking production routes, 2024

| Advantages | Disadvantages | |

|---|---|---|

| BF/BOF | Low OpEx High productivity Excellent quality control Can produce most commercial steel grades | Less flexible operation High CapEx High CO2 emissions, particularly from coke production Reliance on coke supply |

| EAF | Flexible production Lower CapEx Less polluting Can produce small amounts of special grades cost effectively | Susceptible to scrap quality High electricity costs Steel quality control Cannot produce all grades using scrap alone |

Long product production is more suitable for scrap-based EAF production, while many flat products require higher purity melt provided by DRI or BF/BOF steelmaking

Steel products can be broadly categorised as ‘longs’ and ‘flats’, with differing production routes and applications. In 2023 the U.S. produced 80 Mt of steel from 8 integrated mills equipped with BF-BOFs, 85 EAF mills, and 3 DRI facilities. EAF mills were responsible for 100% of longs production and 50% of flats production, totalling to 70% of all steel produced domestically. BOF mills produced the remaining 30%, with all their activity focused on the flats industry.

Long products are the backbone of critical end use markets including construction, engineering, industrial manufacturing, transport infrastructure, and energy infrastructure. Examples of these products include rebar, wire rod, bar products, rail, structural steel and seamless pipes and tubes.

Produced via the rolling of hot steel into the semi-finished product known as ‘slab’, flat products include hot rolled coil (HRC), cold rolled coil (CRC), galvanized sheet, tin plate, welded pipe, tube, and plate. Flat products are more easily recycled, making them a key scrap input for EAF steel production. Common end use markets for flat products include construction, machinery, automobiles, infrastructure, ships, white goods, energy, and defense. Despite slowing growth in some HRC and CRC end-use markets, the products will see additional demand from developments in renewable energy as well as higher infrastructure spending. Wind turbines and solar installations are flat steel intensive, both utilizing up to 40-50%15 iron and steel in their fabrication and installation.

Figure 9 shows average raw material charges to meet the previously stated end-quality specifications. Within the five outlined product types there can be variation.

Figure 9: Raw material inputs for finished steel products, minimum acceptable limit, %

United States steel production has not historically met domestic demand, leading to its position as the largest steel importer in the world. The listed capacities in Figure 10 are likely overreported by steel producers, as utilisation has not exceeded 85%, even when the demand and prices for steel were relatively high. Due to the cost benefits from consuming steel products from countries with comparative advantages in certain products, the U.S. is the fourth largest crude steel producer in the world behind China, India, and Japan.

Figure 10: U.S. Crude steel production, capacity,16 and demand, (Mt) 2023

The U.S. has a strong pipeline of new steel production facilities under construction, with semi-finished steel capacity forecasted to rise at a compound annual growth rate (CAGR) of 4.5% over the next five years. In the flat steel market, the most notable of these projects will be U.S. Steel’s Big River 2 and Nucor West Virginia, both of which are EAF-only facilities, which will each add 3.0 Mt/year of sheet capacity, and ArcelorMittal’s Calvert EAF, which will add 1.5 Mt/y of slab capacity and displace imported slab at their Calvert finishing mill. Long product supply will increase, driven by new mini and micro mills and higher utilization rates at current operations. Whilst these increases in capacity will be low emissions, as they are largely scrap-based, they will have no impact on global carbon emissions. This is because they will be using scrap that is currently exported to international steelmakers. This will redistribute where emissions are produced (to outside the U.S.), not reduce them.

In the global landscape the United States will continue to be one of the largest steel producers. The implementation of carbon border adjustment mechanisms will place EU producers (who are struggling to compete with imports into the EU market due to domestic carbon taxes) on a more equal footing with imports, giving them a better chance to maintain domestic production. This may also shift the source of imports into the EU, as suppliers of low-carbon steel (such as the U.S.) will have an inherent advantage given a CBAM. China is expected to produce less steel over time as its domestic demand decreases. Chinese demand for crude steel will fall by an estimated 2% CAGR through 2028. Developing regions will experience the largest increases in demand and evolving trade patterns as countries strive to find the most cost-effective sourcing.

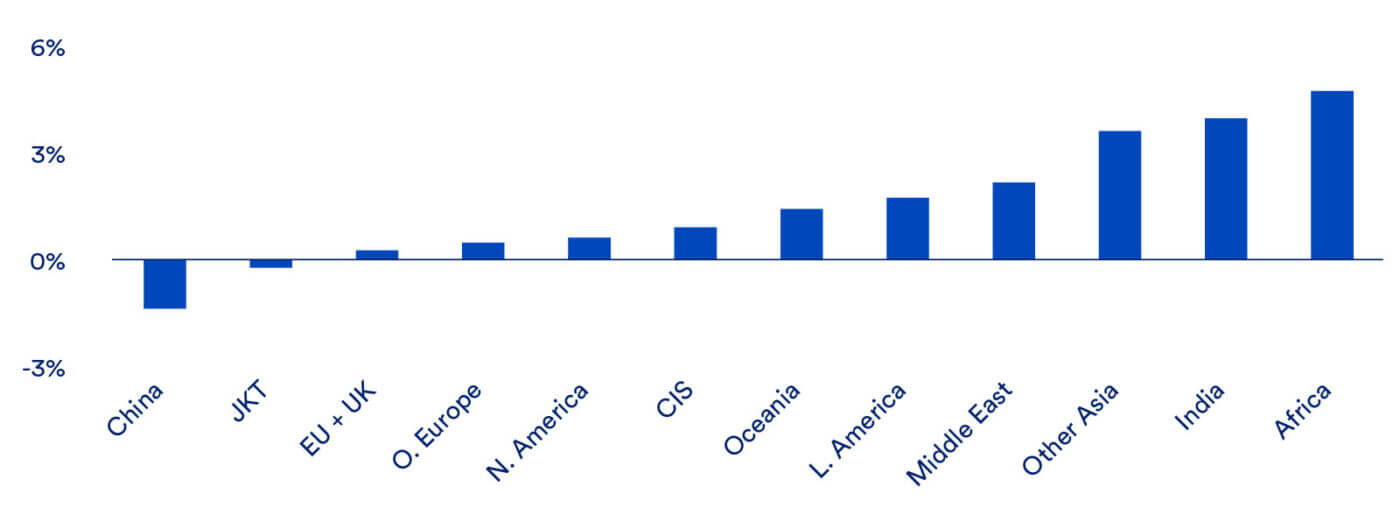

Long term steel demand growth to 2050 in North America is expected to be small, less than 1% year-over-year, and exhibit little change in its share of global demand.17 India and Africa will experience the highest growth in demand year-over-year, between 4-5%, contributing to an over 10% change in global demand by 2050. China, on the other hand, will see declining demand and a reduction in its share of global demand as it transitions out of an industrialization period and international trade policies tighten.

Figure 11: Long-term steel demand growth, y/y %

Steel demand historically tracked with economic growth

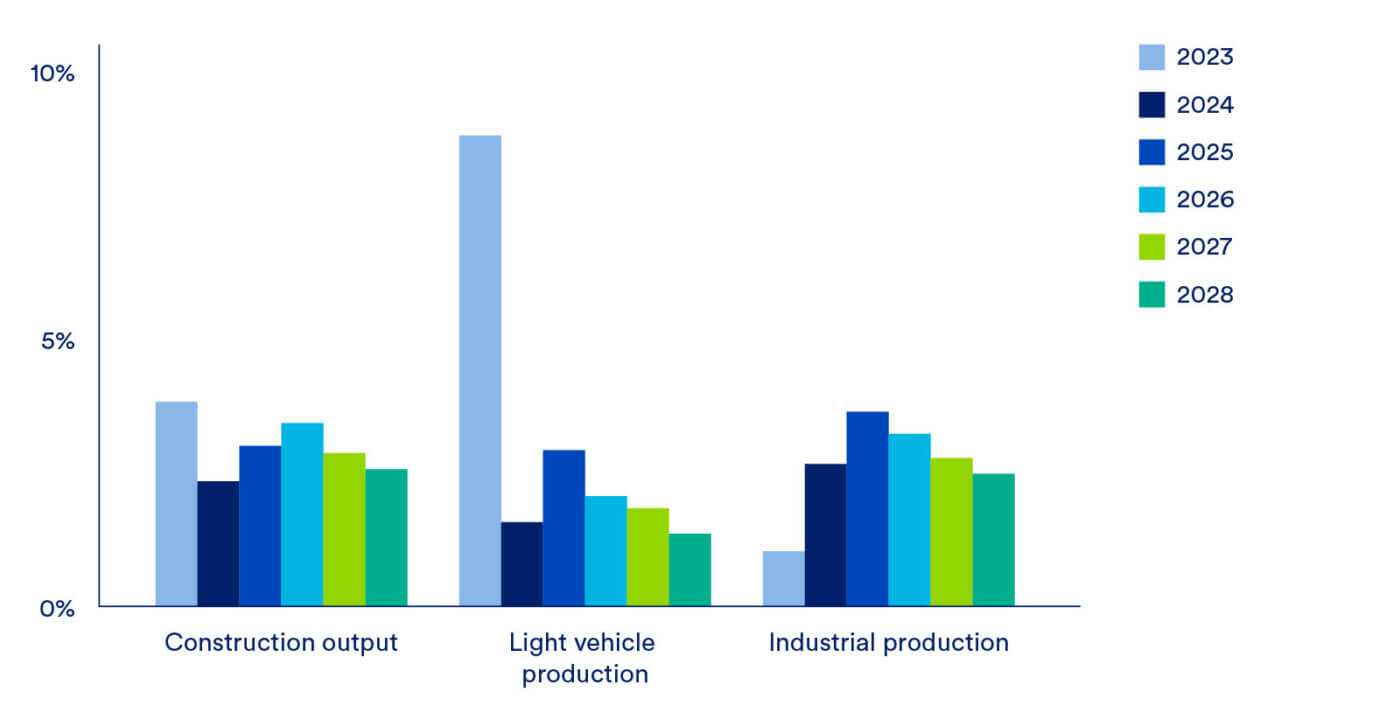

Steel has a wide range of uses and is key for economic development. The largest consumers of steel are the construction industry, followed by the automotive and manufacturing industries. As economies grow, the construction and transportation sectors both increase their respective outputs. Historically, the demand for steel has been tied to these industries as direct indicators, and CRU estimates these industries will continue to be the primary drivers of steel demand. The following chart shows the growth in these three sectors with global economic indicators: construction output, light vehicle production, and industrial production. Over the next five years the growth indicators all forecast positive year-over-year growth between 2-4 percent. The positive, yet moderate, forecasted growth for the economic indicators is reflected in the overall crude steel demand forecasts.

Figure 12: Global economic indicators, y/y change %, 2023

Note: CRU expects overall economic growth to be supportive of steel demand in the medium term as all main steel consuming sectors will expand between 2024–2028.

Other notable uses of steel include consumer goods and appliances, the energy sector, and electrical equipment. As countries around the world begin to decarbonize, other industries will experience slight increases in steel demand. The electrification of the transportation sector will bring about more electric vehicles that demand more infrastructure and energy related equipment. The development of the power grid and charging network to support the additional vehicles will require more steel. The production of more renewable energy will add to medium-term demand in the steel industry.

It is important to note that changes in demand that arise from decarbonisation and the green energy transition will not change the key historical drivers of steel demand. Wind turbines and (to a lesser extent) solar panel racks will drive some additional steel demand, but the amount is relatively small when compared to steel demanded from construction and infrastructure projects.

The U.S. steel industry is less carbon intensive than other major regions

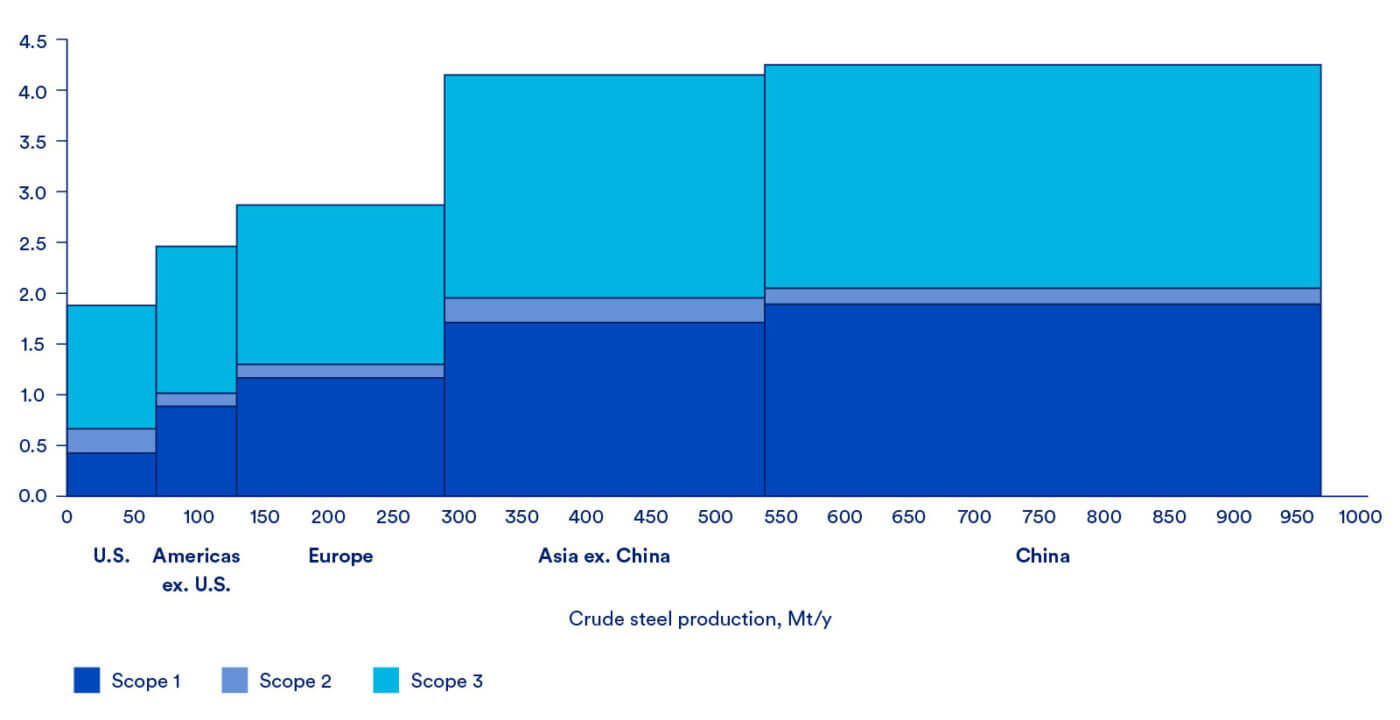

Steel producers in the U.S. have some of the lowest CO2 emissions intensities in the world, as shown in Figure 13. This carbon advantage reflects the high share (~70%) of scrap-based EAFs operating in the U.S. as compared to ~30% for the rest of the world. The ability to operate this level of scrap-based EAFs is largely due to the U.S.’s mature economy, providing ready access to large volumes of scrap. China and Asia excluding China are the highest emitting regions, with Europe placed between Asia and the Americas. Steelmakers in Europe are actively making improvements to their steelmaking processes with decarbonization a clear goal of the industry.

Figure 13: Calculated scope 1, 2, and 3 CO2 emissions by region, t CO2 /t crude steel, 2023

Note: Scope 3 emissions do not include upstream emissions from coal or natural gas production.

Figure 14 shows the differences in emission intensities between EAFs and integrated steel mills. There is a delineation in the emissions intensities of U.S. integrated and EAF mills. The separation between the two processes would be more drastic if only analysing scope 1 and 2 emissions. However, adding scope 3, which are defined as third party input purchases, provides a more accurate comparison. Readers should note that methane and CO2 emissions from the coal or natural gas supply chains, which can be quite significant, are not included in CRU’s scope 3 figures due to the large variability in potential emissions depending on source of fuel and assumptions. See Section 11.2 for a discussion of these emissions and their impacts. CRUs methodology and definitions for each scope are included in the glossary.

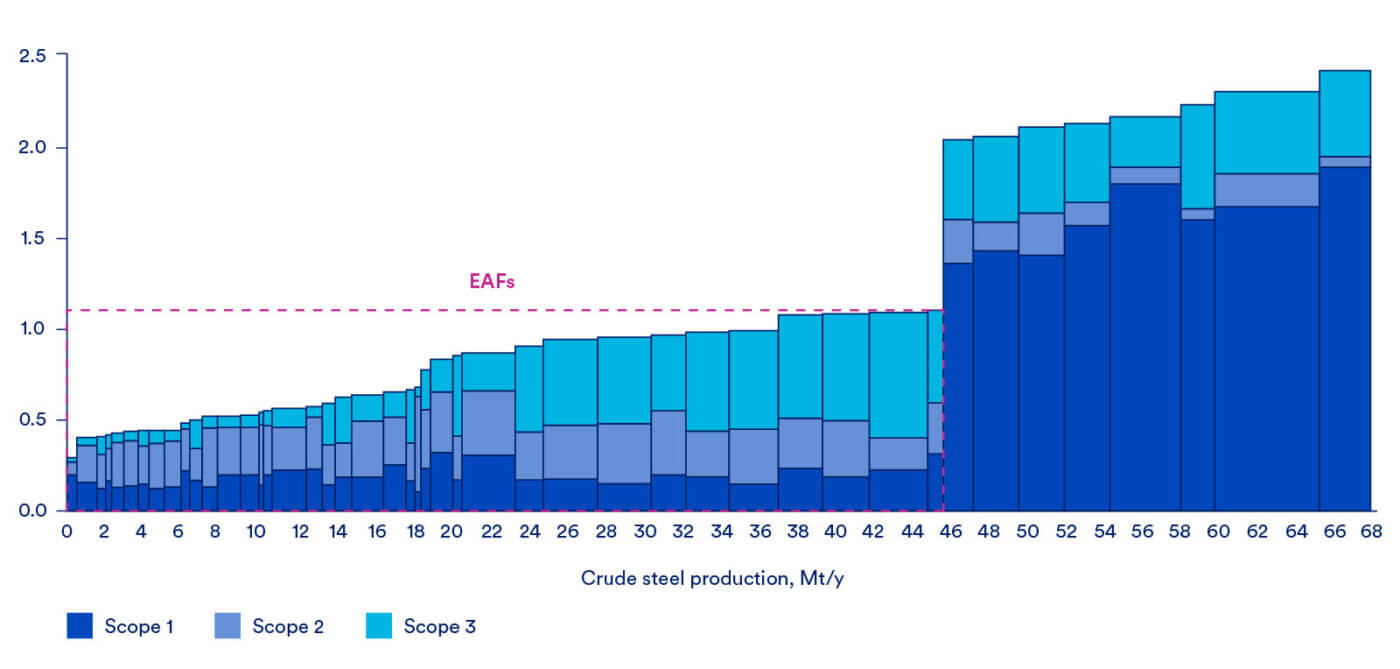

Specific emissions for the integrated facilities can be found in Figure 23. Amongst the EAF facilities there is more variation due to the quality of steel being produced, and these differences are outlined more clearly in Figure 28. EAF mills that are required (for quality reasons) to utilize OBM have higher emissions, specifically scope 3, as the iron reduction process is emissions intensive. The group of EAFs producing higher-quality steel and using more energy intensive inputs can be found in the middle of the figure below, between ~24 and ~46 Mt/y on the x-axis. EAFs located further to the left-hand side produce products that do not require OBMs.

Figure 14: Emissions intensities for U.S.-based steel producers, t CO2 / t crude steel, 202318

Note: Production is less than U.S. total due to omitted production of facilities without emissions data. Scope 3 emissions do not include upstream emissions from coal or natural gas production.

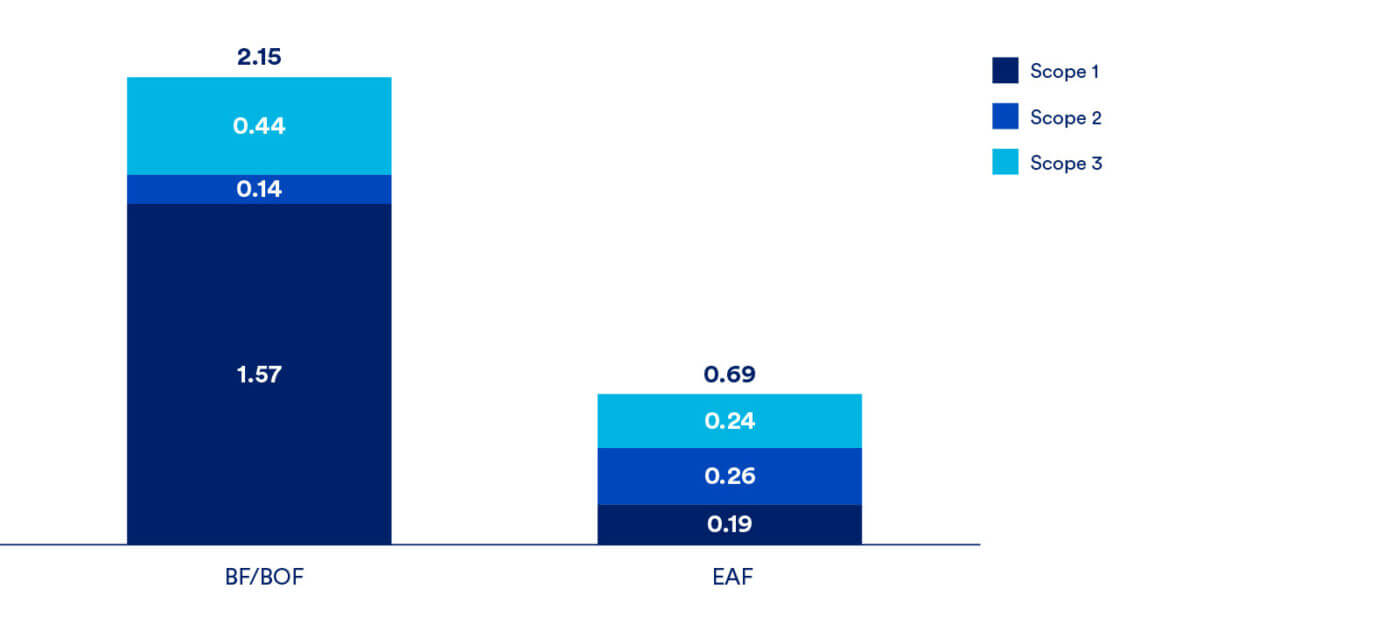

The following figure summarizes typical emissions intensities for both steelmaking pathways. Emissions intensities for EAFs are nearly three times less than the integrated mills. For an average EAF, scope 2 emissions are the most significant contribution, and are associated with generation of power. Switching to a clean electricity source could reduce the carbon intensity of the steel produced by roughly a third.

Figure 15: Average emissions intensity by scope, t CO2 / t crude steel, 2023

Note: Scope 3 emissions do not include upstream emissions from coal or natural gas production.

The primary difference between integrated mills and EAFs is in the lack of the carbon-intensive ironmaking process for EAFs. The figure below shows the relative sources of emissions for various iron and steelmaking processes. Integrated mills produce high emissions in the process of reducing iron ore to reach the steelmaking step, while EAFs start from steelmaking via the reuse of steel. The carbon intensity of scrap charged into the EAF is considered to be zero, even though most scrap originated from a carbon intensive integrated mill.

Figure 16: Relative scale of emissions for ironmaking and steelmaking pathways

Note: Actual emissions by process are found in Figure 23 and Figure 28.

Raw material processing includes processing and transport of iron ore products. Raw material processing contributes 10-20% of total emissions. If a facility has an onsite coking plant, then the emissions from coking are also included. Most raw material processing emissions come from the coking and pelletizing facilities. Variation in emissions exists across facilities due to different raw material inputs.

Ironmaking is the primary driver for emissions related to steel production. Responsible for 40-50% of total emissions, the efficient but carbon-intensive blast furnace results in higher intensities relative to other processes. Emissions from ironmaking are a result of the reduction process.

Steelmaking is the process of converting scrap, OBM and liquid pig iron into the final, liquid steel of the desired chemistry. Steelmaking is more carbon intensive for EAFs due to the large energy demand, as much of the feedstock material is in solid form, whereas a BOF starts with mostly liquid iron. However, this value can vary greatly for an EAF based on the associated electricity emissions. EAFs using clean electricity will significantly reduce their carbon intensity.

Auxiliary and fugitive emissions are difficult to abate, and specific to a plant’s supply chain. Although these emissions, excluding those from the natural gas and coal supply chains, comprise a small fraction of total emissions while looking at all scopes, it remains a hurdle to reach net-zero steel production. For some of these processes, such as the production of burnt lime and dolomite, carbon capture could be implemented. Production of industrial gases (such as the high-purity oxygen needed for the BOF) is another example of a process that could decarbonize via the use of clean electricity. Most difficult to abate are fugitive emissions, which are greenhouse gasses which escape during industrial activities, such as mining ore. Since both domestic integrated producers operate their own iron ore mines, they have control over this step of the operation. New technologies which reduce emissions from direct emissions sources will lead to industry-wide carbon reduction, but they are costly. The steel industry in the U.S. is making progress towards adopting new technologies and processing capabilities as incentives evolve. Integrated mills and EAFs in the U.S. continue working toward lower emission steel due to potential emissions standards and evolving consumer preferences. A transition to low- or zero-carbon steel will depend on the primary steel supply chain reducing emissions across the entire steelmaking process.

U.S. steelmaking has shifted over time from integrated mills to EAF mills

Steel production in the United States is largely carried out by EAF facilities, but this was not always the case. The traditional steel making route utilizing blast furnaces represented most of the production until 2005. Standalone EAF production has lower CapEx and raw material costs due to its simplified supply chain, utilizing scrap, and high-quality iron to eliminate the ironmaking process partially or entirely. EAFs can choose their location more freely as they are not restricted by coal and iron ore supply, but instead by energy cost and product demand. Their supply chains are less constrained as scrap and HBI can be efficiently transported, and production is flexible as they can more easily start up and shut down as necessary, unlike a blast furnace.

The production of liquid iron in integrated steelmaking is responsible for most of the cost associated with the process. Most integrated steel mills in the U.S. are in the Great Lakes Region due to the proximity to iron ore and coal mines, which reduces transportation costs and risks from exposure to low-cost seaborne imports. The Great Lakes-centric supply chain creates synergy between ore producers and steel makers. Captive domestic ore producers sell almost exclusively to U.S. and Canadian mills, as pellet exports require shipping costs of over $30 per tonne of iron ore, reducing competitive advantage in foreign markets.

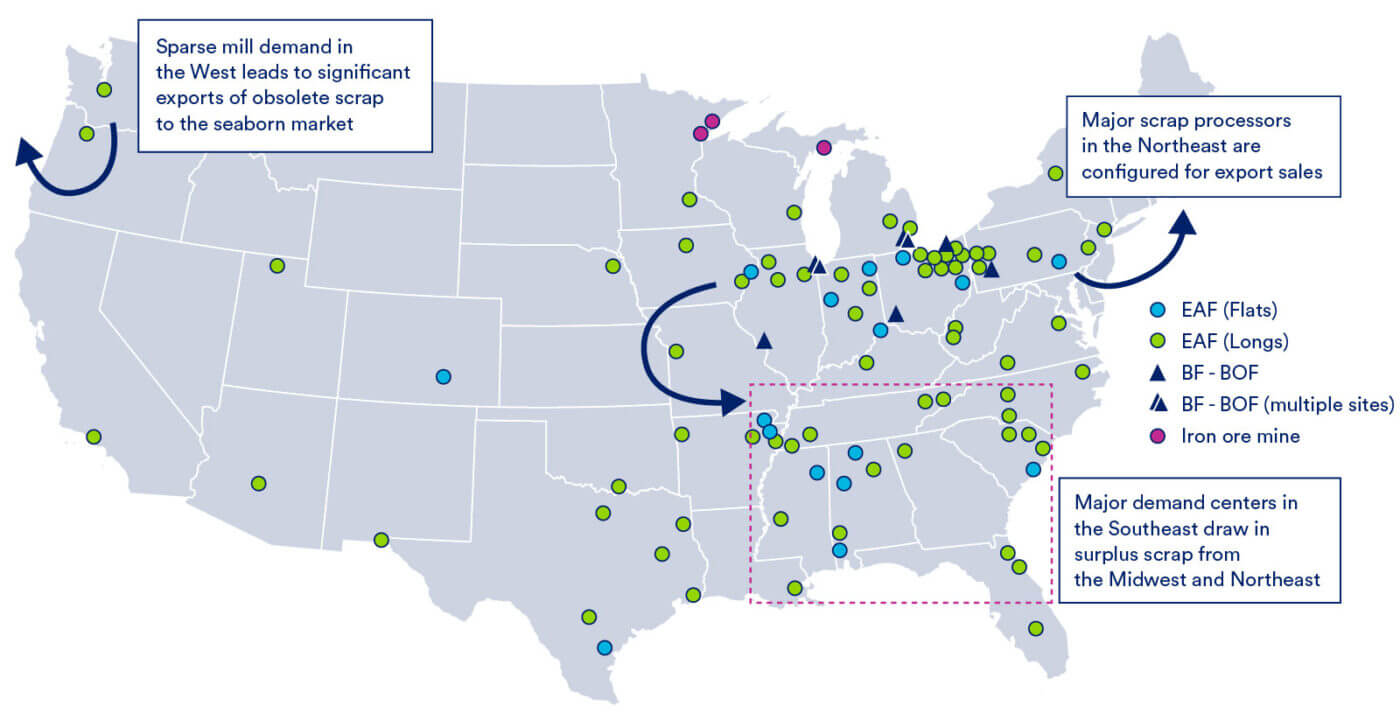

EAF locations are not constrained to the Great Lakes region because they do not source iron in the same fashion as for BF-BOF production. The locations of EAFs are influenced by scrap availability and local demand for steel products. As a developing industrial and auto manufacturing hub, the South/Southeast hosts major demand centers that independently generate scrap and draw surplus scrap from the Midwest and Northeast. Furthermore, growing activity in the South drove the expansion of the hot briquetted iron (HBI) market, which was created to improve the shipping quality and safety of DRI. Production capacity in the South is comprised entirely of EAFs, with the last blast furnace in the region idled in 2014 (U.S. Steel Fairfield) and replaced by an EAF. The southern United States will produce over 74% of total U.S. steel by 2030.

Figure 17: Major U.S. steel mills, 2024

EAF operators such as Nucor, Steel Dynamics, and Commercial Metals Company have invested heavily into scrap processing facilities. Using their own scrap as an input in the EAFs helps reduce cost, guarantee supply, and control quality. Last year Nucor reported that they recycled 18 Mt of steel scrap. Over 90% was used in their own operations with the remainder sold externally with the help of Nucor subsidiary DJJ, the largest ferrous scrap broker in North America.

The shift to EAFs took off in response to ideal market conditions which supported capacity expansions without disrupting cost flows or established supply chains. New EAF capacity additions continue to fill the supply gap resulting from BOF shutdowns in the Midwest. Additionally, EAFs continue to add capabilities to produce higher quality and specific grades of flat steel products. EAFs can match the quality of integrated steel production given the use of sufficient quantities of very high-quality scrap and OBMs.

Along with factors such as available scrap and favorable energy costs, the Southeast began to attract significant amounts of new manufacturing investment (including EAF-based steel producers) due to these states being “right to work,” reducing the likelihood of unionization. The new, low-cost, highly automated steelmaking capacity constructed in this region placed significant economic pressure on older, higher-cost (and higher emission) steelmaking, much of which was in the East and Midwest regions, leading many of these facilities to eventually shutdown.

Figure 18: United States BOF and EAF capacity, Mt

EAF steel production will continue to grow in the U.S., backed by competitive cost structures, available scrap, ESG driven decision making, and government support. Improvements in efficiency, cost, and production capability have bolstered EAF’s competitiveness in steel markets, most importantly, flat products. These mills will benefit from growing demand for steel and its use in solar, wind, and an upgraded electrical grid.

Integrated BF/BOF steel production facilities will continue to draw value from the well-developed Great Lakes supply chain

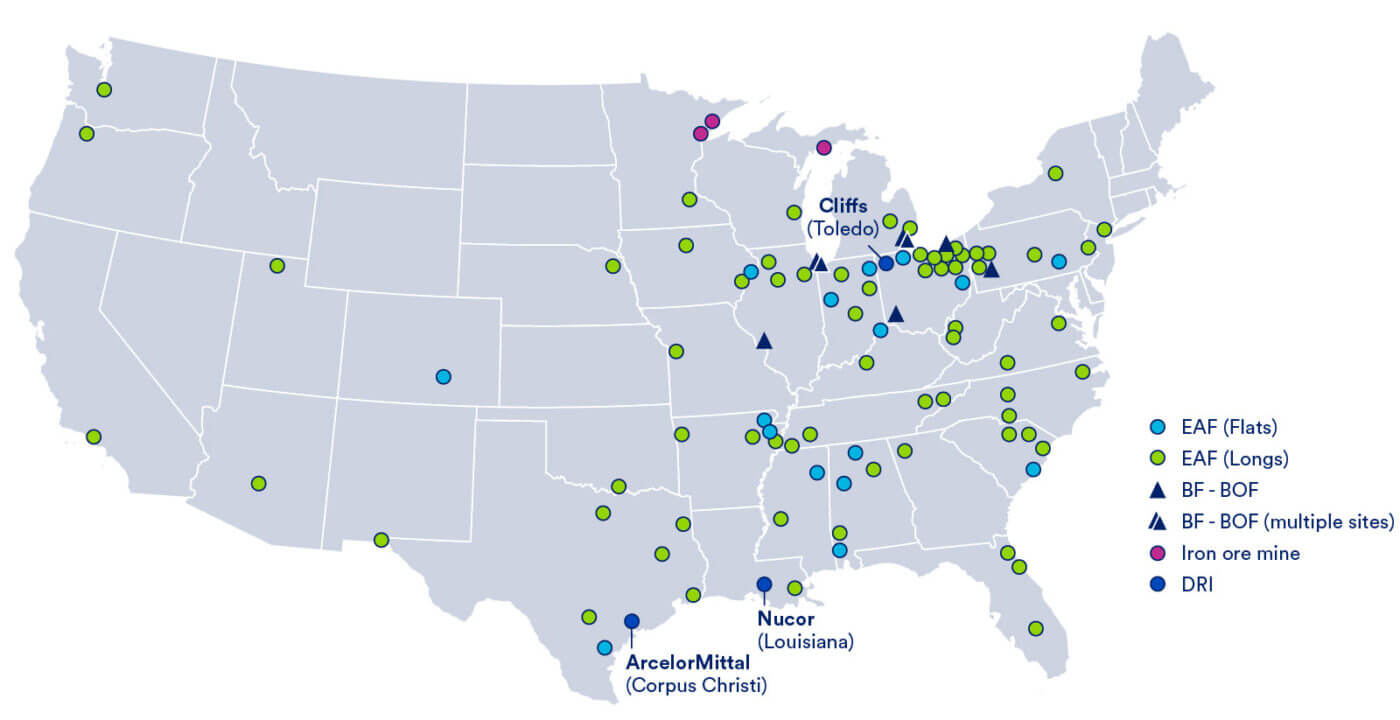

Figure 19: Distribution of U.S. BF/BOF facilities, 2023

Note: Cleveland Cliffs Dearborn facility is limited to BF, BOF, and caster only. Granite City is idled indefinitely.

In 2023, the United States had eight integrated mills with iron and steelmaking capabilities. The U.S. BF-BOF market is controlled by two companies, Cleveland Cliffs and U.S. Steel, each of which have four facilities. Production from the eight active integrated mills totalled ~23 Mt in 2023, comprising 28% of annual production. Of those eight plants, U.S. Steel idled its Great Lakes facility in 2019, followed by its Granite City facility in 2023 (although both are still operating finishing facilities). While these two facilities are unlikely to restart, the potential acquisition of U.S. Steel could change operating plans, particularly with regards to Granite City. Each facility varies in configuration and size, but collectively they supply high-quality products with a range of end-use demands.

U.S. iron ore miners and U.S. steelmakers developed a co-dependency due to logistical difficulties and freight costs associated with pellet imports to the Great Lakes region. Domestic miners have faced little competition from external suppliers; however, these same issues make it difficult to export pellets. While U.S. iron ore miners benefit from this market structure and competitive advantage when supplying pellets to domestic customers, they are at a competitive disadvantage when attempting to sell product outside the region. The logistical barriers to enter the Great Lakes iron market allows the region’s suppliers and buyers to develop pricing mechanisms distinct from those in the international market. Cleveland Cliffs and U.S. Steel are both vertically integrated and operate their own iron ore mines that supply most of the iron ore used in their operations.

The following profiles summarize each U.S. integrated mill operation. Profiles are provided for the eight facilities that were active in 2023. Written profiles of each facility are found in Appendix 1: U.S. Integrated Mill Profiles.

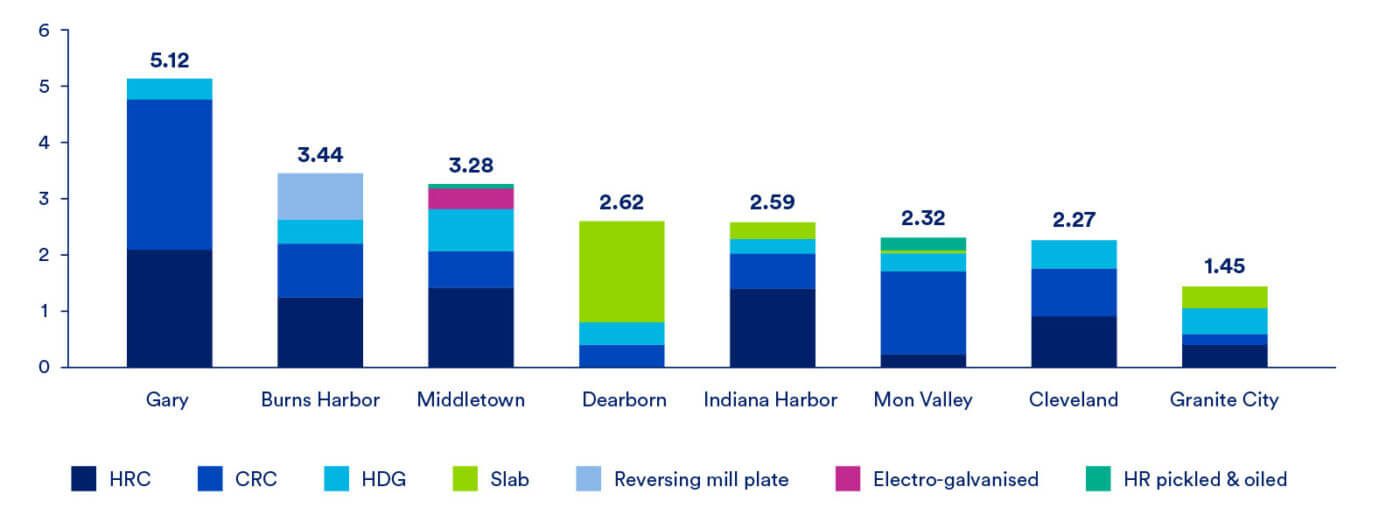

Figure 20: Finished production split, Mt/y, 202319

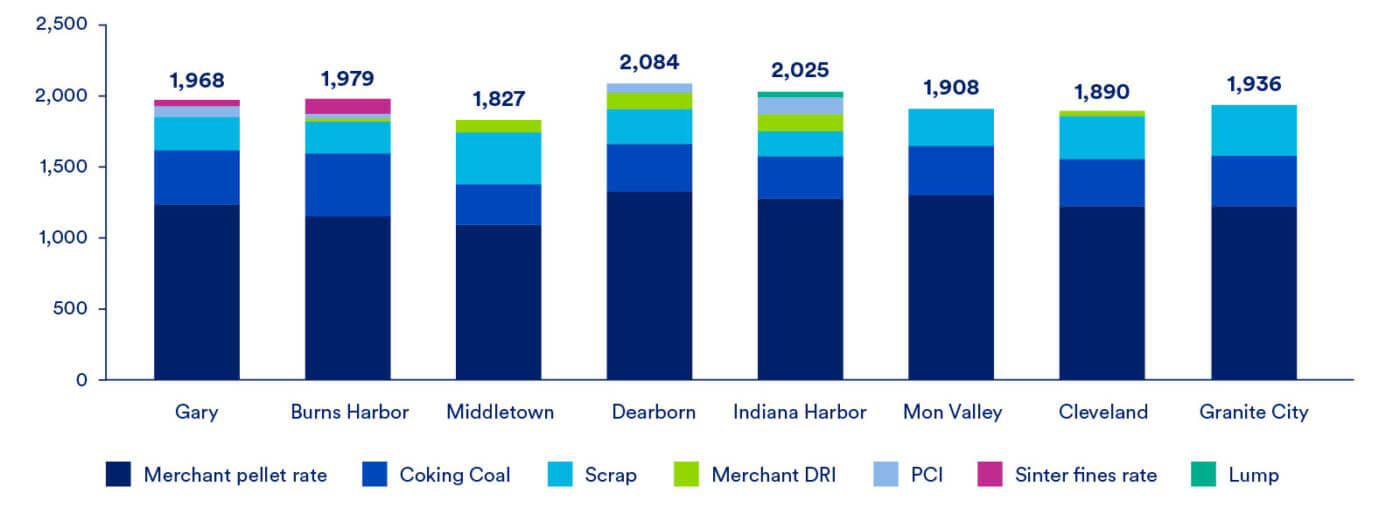

Figure 21: Raw material inputs, kg/t crude steel, 2023

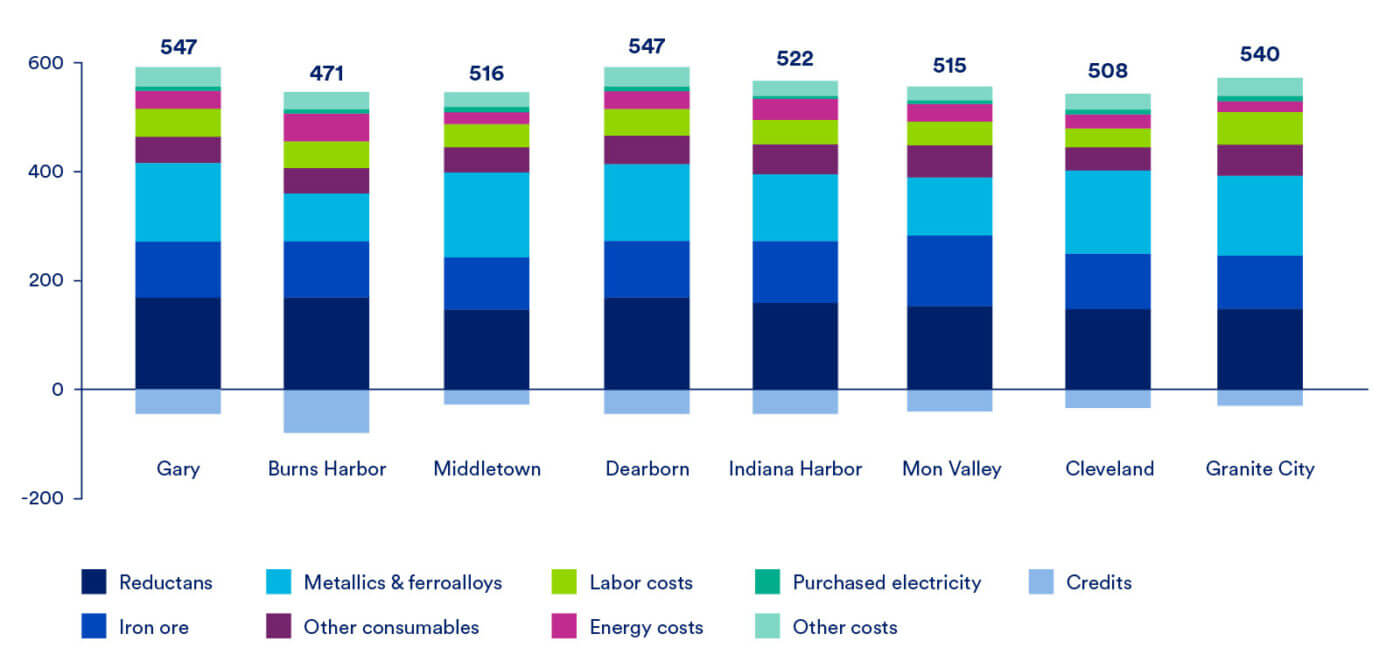

Figure 22: Site costs, USD/t crude steel, 2023

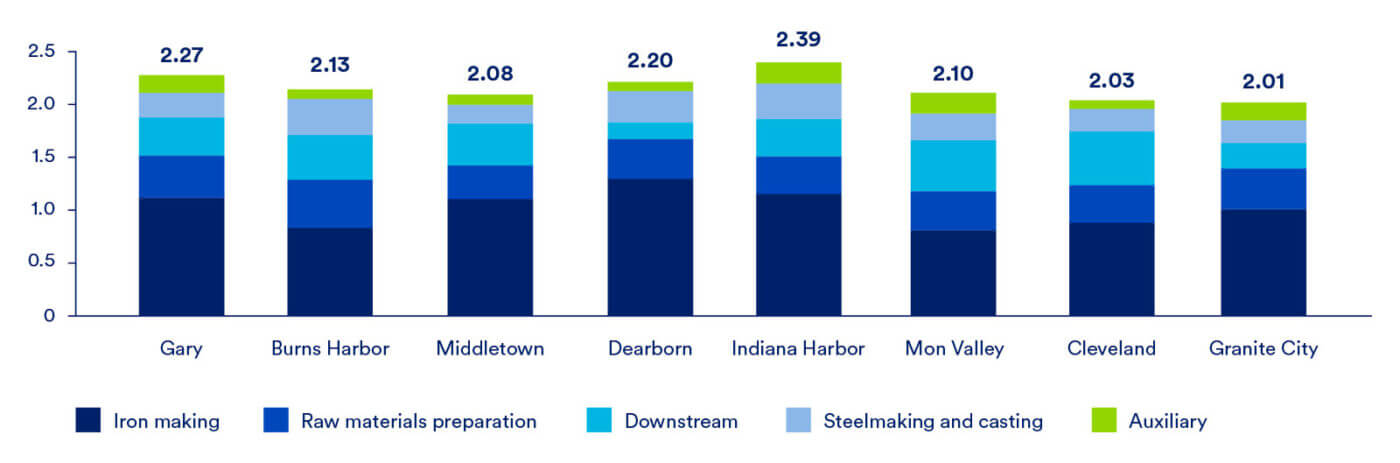

Figure 23: Emissions intensities20 by process, t CO2 / t crude steel, 2023

EAFs steel production facilities are distributed across the U.S. and less concentrated than BOFs

Figure 24: Distribution of United States EAF facilities, 2023

Table 2: Summary statistics for EAF flats and longs mills

| Product | Total mills | Capacity (Mt) | Final products | End use markets |

|---|---|---|---|---|

| Flats | 16 | 51 | Sheets, plates | Automotive, construction, transportation |

| Longs | 69 | 37 | Rebar, pipes, casts, bars, wire rod | Infrastructure, industrial, manufacturing, machinery, automotive |

The 85 U.S. EAF mills supply a larger and more diverse market than the BF/BOF producers. EAF steel production is the predominant route for the U.S., totalling 70% of the market. Unlike BOFs, which cover a wide product distribution area, EAFs are generally smaller and service regional markets. EAFs rely on the quality of scrap and the availability of OBMs used to meet product specifications. Higher quality metallic inputs (either high-quality scrap or OBMs) equate to higher melt efficiency, as well as higher-quality output. As an example, rebar is a relatively simple, easy to produce product with little in the way of chemistry requirements, allowing it to be produced in an EAF charged almost entirely with scrap, whereas flat products require a greater share of OBMs to produce high-quality steel with low residual elements.

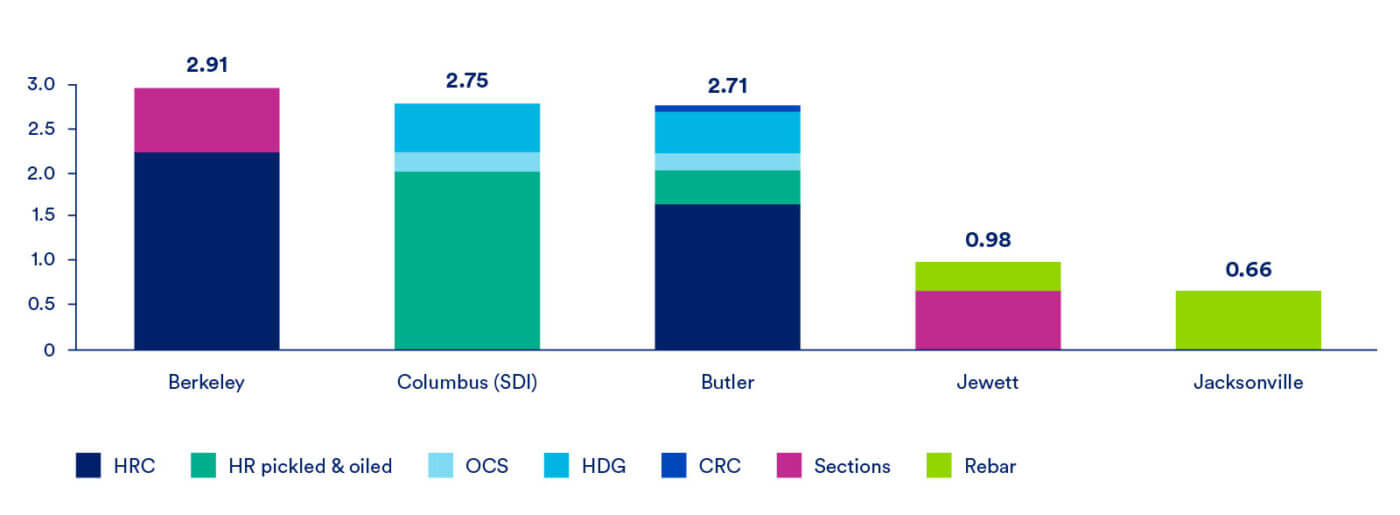

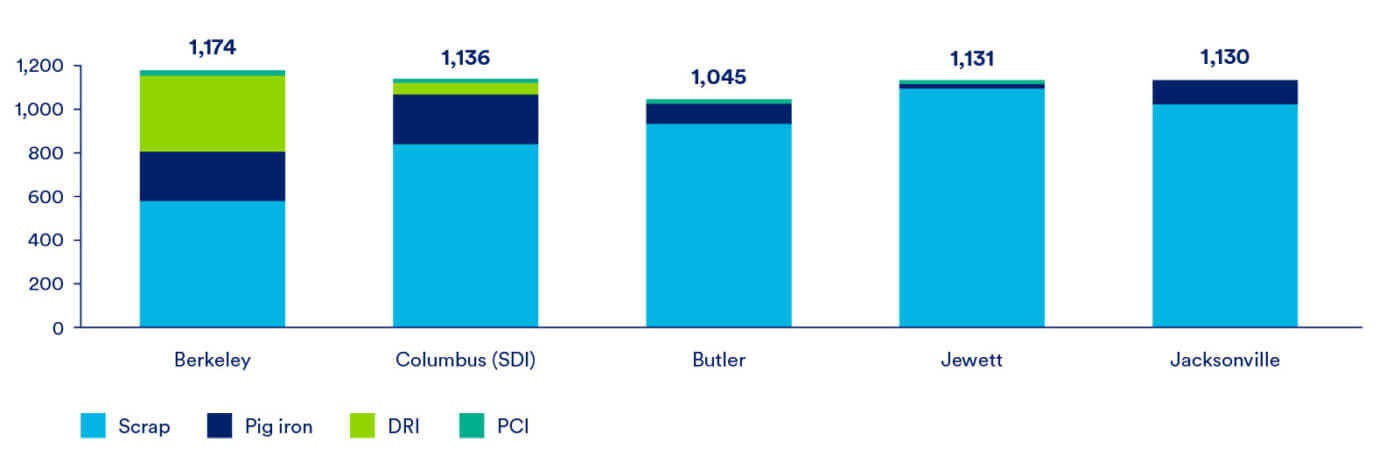

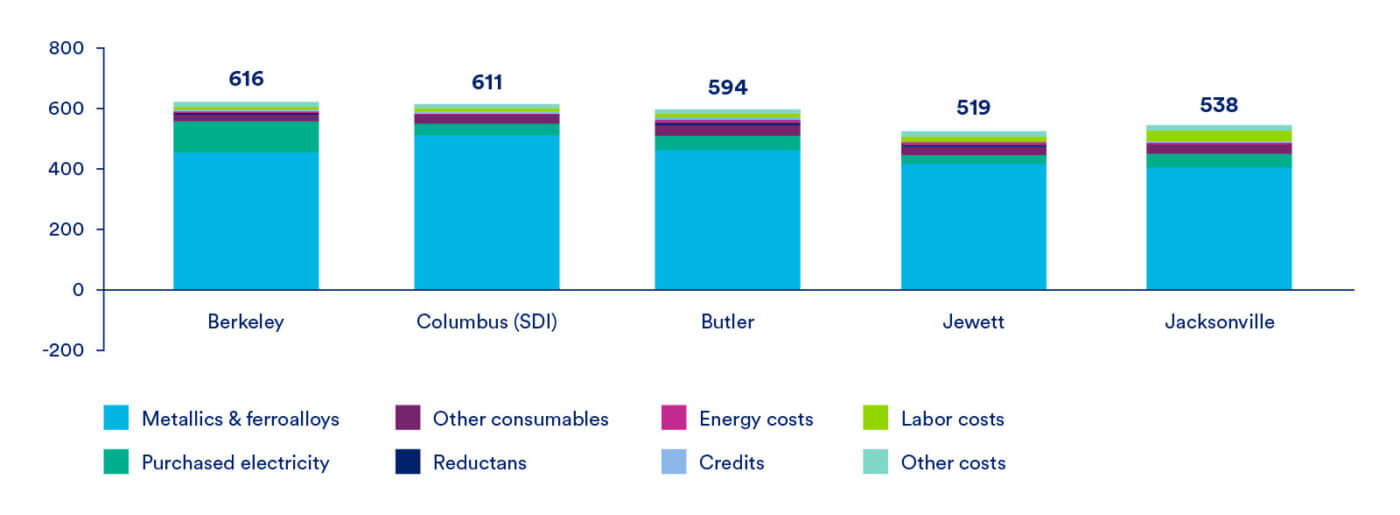

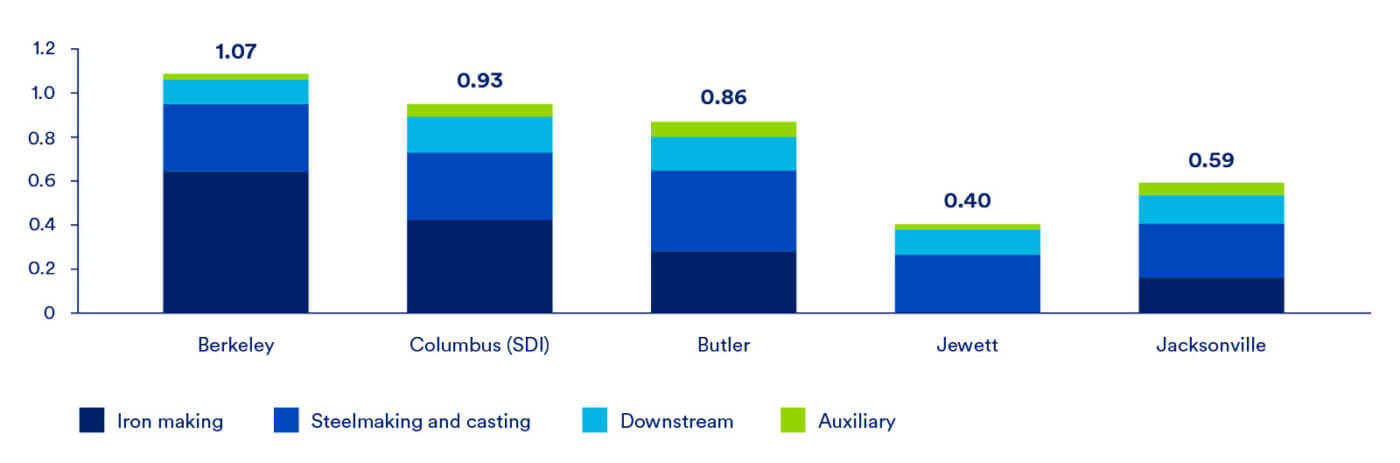

CRU has identified five representative EAF mills to create a cross section of all U.S. EAF facilities. The selected mills show product diversity between flat and long production and subsequent end markets. Jacksonville and Jewett represent long product facilities with less variation in material input and end-product. The remaining facilities represent flat production with significant differences in production split and raw material inputs. Written profiles of each EAF facility can be found in Appendix 2: U.S. EAF Profiles.

Figure 25: Finished steel production, Mt/y, 2023

Figure 26: Raw material inputs, kg/t crude steel, 2023

Figure 27: Site costs, USD/t crude steel, 202321

Figure 28: Emission intensities22 by process including scope 3 ironmaking, t CO2 /t crude steel, 2023

Product requirements dictate the charge-material mix for EAFs

Flat-rolled products generally require higher-quality raw materials than long products. Flat products consume OBMs at much higher rates, with charge percentages between 20% to 40%. The Columbus and Berkeley facilities utilize this elevated split. OBMs comprise 25% and 49% of Columbus and Berkeley’s charges, respectively. The Berkeley plant produces HRC to be used in the automotive industry, so their OBM consumption rate is high. Columbus is similar to Berkeley, but charges much less DRI and relies heavily on the use of high-quality, prime scrap.

Butler represents a unique class of EAF as it produces five different product types, both long and flat. It has the lowest raw material input due to access to high quality scrap from the Great Lakes region as well as a 0.35 Mt rotary-hearth type DRI/SAF plant.

The Jewett and Jacksonville facilities are longs producers. Both locations produce rebar, with Jewett differing in its production of sections for the construction industry. Despite similar product mixes, the Jewett facility uses nearly no OBM. The high percentage of scrap and lessened importance of OBMs allows these two facilities to have lower emissions compared to the flat producers.

The longs producing facilities are smaller than flats facilities. Smaller EAFs, less than 1 Mt/y, such as Jacksonville are gaining popularity and have received the title of “micro mills”. The rebar-centric production is reflected in the plant’s raw material mix, with over 90% of the melt being scrap. Scrap quality is not a major concern for rebar producing facilities, but still impacts the efficiency of the operation. Despite producing a lower-quality product, a small amount of an OBM – specifically cold pig iron – is charged in the furnace to increase efficiency.

Direct reduced iron provides a lower-carbon source of high quality metallics

Direct reduced iron (DRI) is an ore-based metallic (OBM) that plays an important role in decarbonizing the steel industry, as it provides new iron units with low impurities. This material can be used in combination with steel scrap in an EAF, charged into a BF to increase yields and reduce coke usage or remelted and refined in a submerged arc furnace (SAF) and then charged into a BOF. DRI has become more important as blast furnaces have been idled, as it provides the OBM units needed to produce high-quality products. As discussed below, domestic OBM demand has averaged roughly 30 Mt a year, a number expected to remain stable over the medium term. Most DRI/HBI is produced with natural gas as a fuel source and reductant, although with additional upgrades and expenditures, other fuel sources such as hydrogen could be utilized.

The combination of clean (low-carbon) electricity and low-carbon hydrogen could provide a near carbon-neutral iron product. Facilities such as Cleveland Cliffs Toledo have installed infrastructure that can utilize either natural gas or a mix of natural gas and hydrogen. The option to start with natural gas and switch to hydrogen as it becomes available makes DRI even more appealing and, combined with the availability of inexpensive natural gas, will make it likely that DRI will take share from blast furnaces as ironmaking facilities are upgraded.

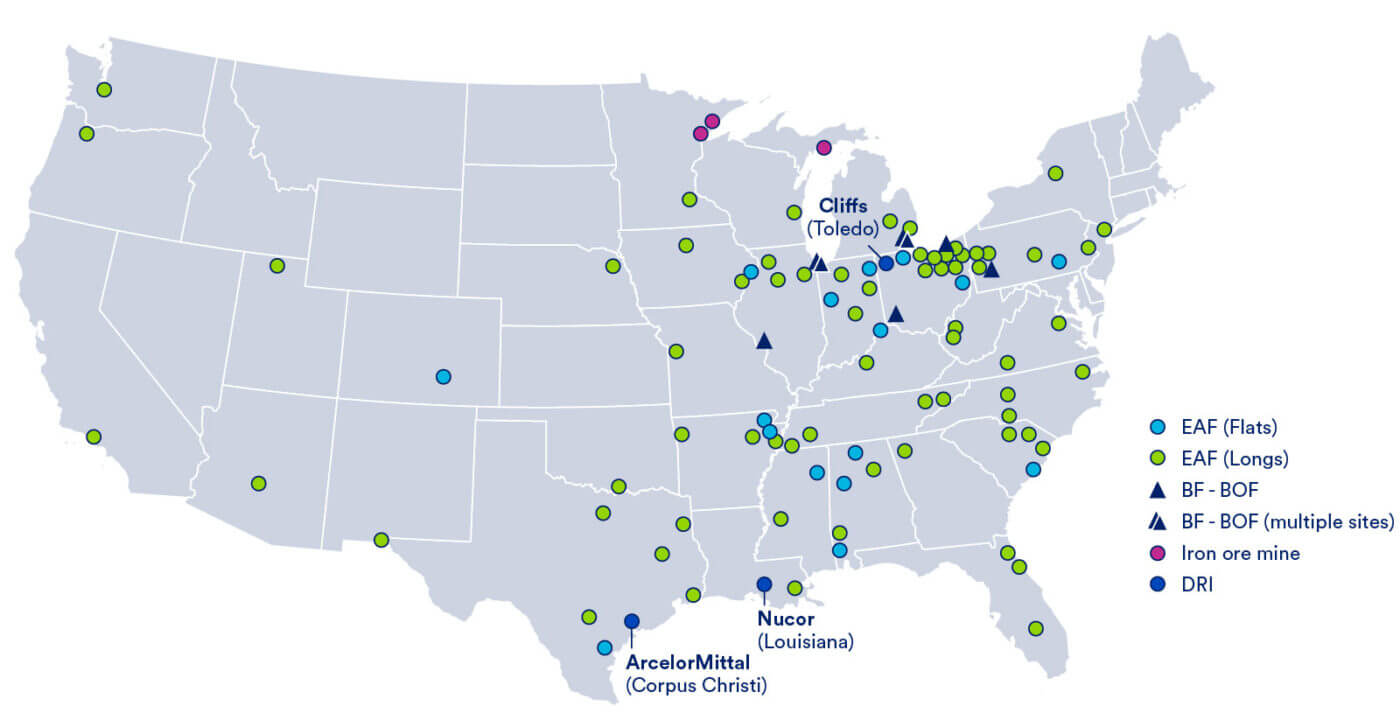

Figure 29: United States DRI facility locations, 2024

Louisiana HBI

Nucor steel owns and operates the Louisiana DRI/HBI plant located in Louisiana. The plant has been operating since 2014, with an annual capacity of 2.5 Mt. The plant’s location along the Mississippi river allows for efficient distribution of material. Equipped with barge loading/unloading, the facility allows for deepwater ships to offload iron ore that is transferred to the processing plant. Once the reduction process is finished, the DRI is sent back to barges for distribution to steel mills.

The energy source for the plant is natural gas and utilizes the Energiron process as opposed to the other plants utilizing Midrex reduction technology. Energiron captures part of the CO2 in the off gas as a feature of the process, making CCS for this technology somewhat easier. Nucor announced a partnership with ExxonMobil to implement a carbon capture system at this DRI facility starting in 2026. The plan is to capture up to 800 kt of CO2 per year, or upwards of 65% of total carbon emissions.

Corpus Christi HBI

The Corpus Christi HBI/DRI plant is in Texas. The plant’s deepwater port allows for access to transportation routes throughout the Americas and globally. The plant was constructed in 2017 by Voestalpine using Midrex technology with an investment of $1 billion dollars. In 2023, ArcelorMittal acquired an 80% share in the plant, with Voestalpine retaining the remaining 20%. The plant has a nameplate capacity of 2.0 Mt/y of HBI, with production at 1.6 Mt in 2023. Voestalpine was previously using the HBI in their own steel operations, with offtake agreements in place that have since expired. During the acquisition by ArcelorMittal, a long-term offtake agreement with Voestalpine was created to supply an annual volume of HBI relative to Voestalpine’s 20% stake for its steel mills in Austria. The remaining balance is delivered to third parties and ArcelorMittal facilities. Current production utilizes direct injection of natural gas, but the facility can be converted to solely use hydrogen. ArcelorMittal plans to utilize green hydrogen DRI to deliver a decarbonized steel product but has not announced any firm plans for when the transition might occur. In 2023, the University of Illinois was awarded just under $4 million dollars from the U.S. Department of Energy’s (DOE) Office of Fossil Energy and Carbon Management, with ArcelorMittal as a subrecipient, to conduct a front-end engineering and design (FEED) study for a commercial-scale CCS project which aims to capture 95% of emitted CO2 from the HBI plant using a Pressure Swing Absorption (PSA) system assisted with Cryocap™ technology.23

Toledo DRI

The Cleveland-Cliffs Toledo direct reduction plant has been operating since 2020 and has a capacity of 1.9 Mt/y of HBI. The Toledo plant is one of the most modern of the U.S. direct reduction facilities and utilizes the Midrex process. Unlike the other direct reduction plants, Toledo is in the Great Lakes region; it utilizes domestic, HBI-grade iron ore pellets and transports material directly to Cleveland-Cliffs’ operations in the region. The operation is presently fuelled by natural gas, but the configuration allows for 30% to be replaced by hydrogen with no changes to the facility. With equipment modifications, Cleveland-Cliffs estimates that hydrogen usage could rise to 70%.

Middletown DRI (proposed)

In March 2024, Cleveland-Cliffs was selected to receive a DOE Office of Clean Energy Demonstration grant of “up to $500 million” to replace its Middletown blast furnace with a 2.5 Mt/y “flex-fuel” DRI plant and two 120 MW electric melting furnaces (EMFs).24 The DRI plant will be fed with lower-quality BF-grade iron ore pellets (sourced internally), with the solid, low-quality DRI melted and refined in the EMFs and then charged into the plant’s existing BOF furnaces. At startup, the DRI plant will be run using natural gas, with the option to switch to a mix of hydrogen and natural gas or hydrogen alone in the future. Cliffs claims a 50% reduction in carbon intensity using natural gas and 90% using green hydrogen. The total cost could be $2.1 billion, with the new facility requiring an additional 170 employees.

Pig Iron Metallics

A further opportunity to generate high-quality metallics involves the casting of ‘cold’ pig iron via a pig caster, which is fed with hot metal from a traditional blast furnace. This is an easy-to-implement process that has been performed routinely for decades. U.S. Steel recently installed a pig machine (capacity 0.45 Mt, $60 million, startup May 2022) at its Gary plant, with the pig iron offtake used in U.S. Steel’s EAF facilities. Pig iron sourced from an unabated blast furnace is a high-carbon raw material, leading to higher scope 3 emissions for EAFs that utilize the material. Equipping the blast furnaces at Gary with CCS would reduce the carbon impact of producing this cold pig iron, providing a high-quality, low-carbon feedstock for use in EAFs.

Carbon capture technology review

Carbon capture for integrated steelmaking

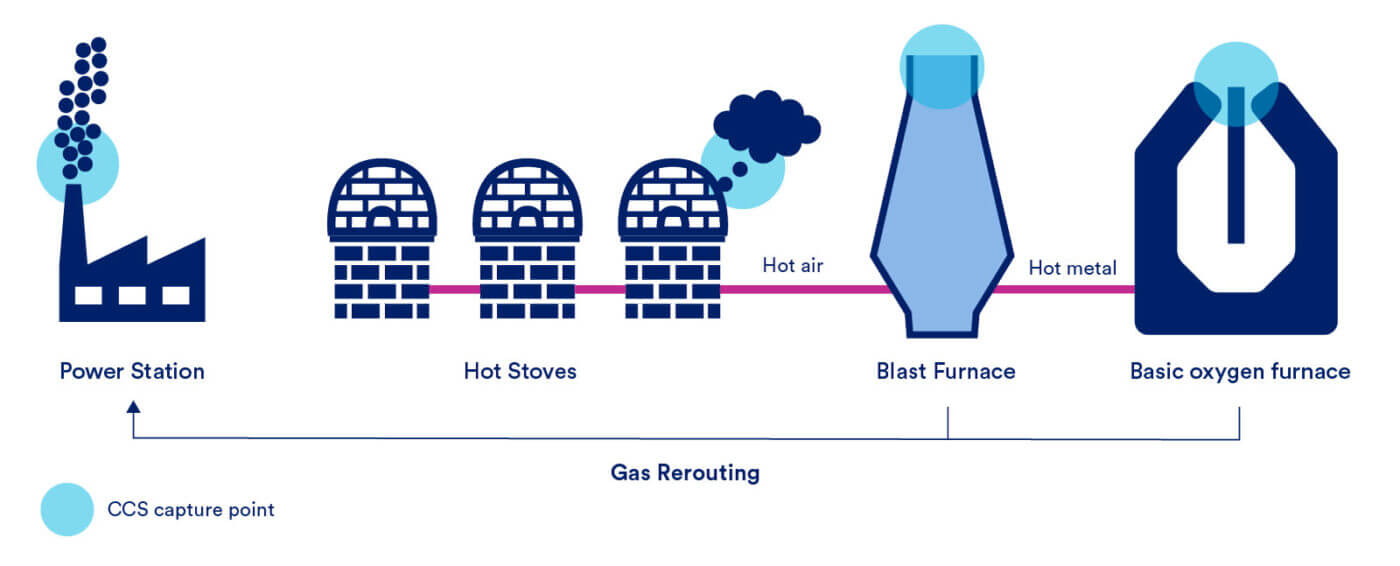

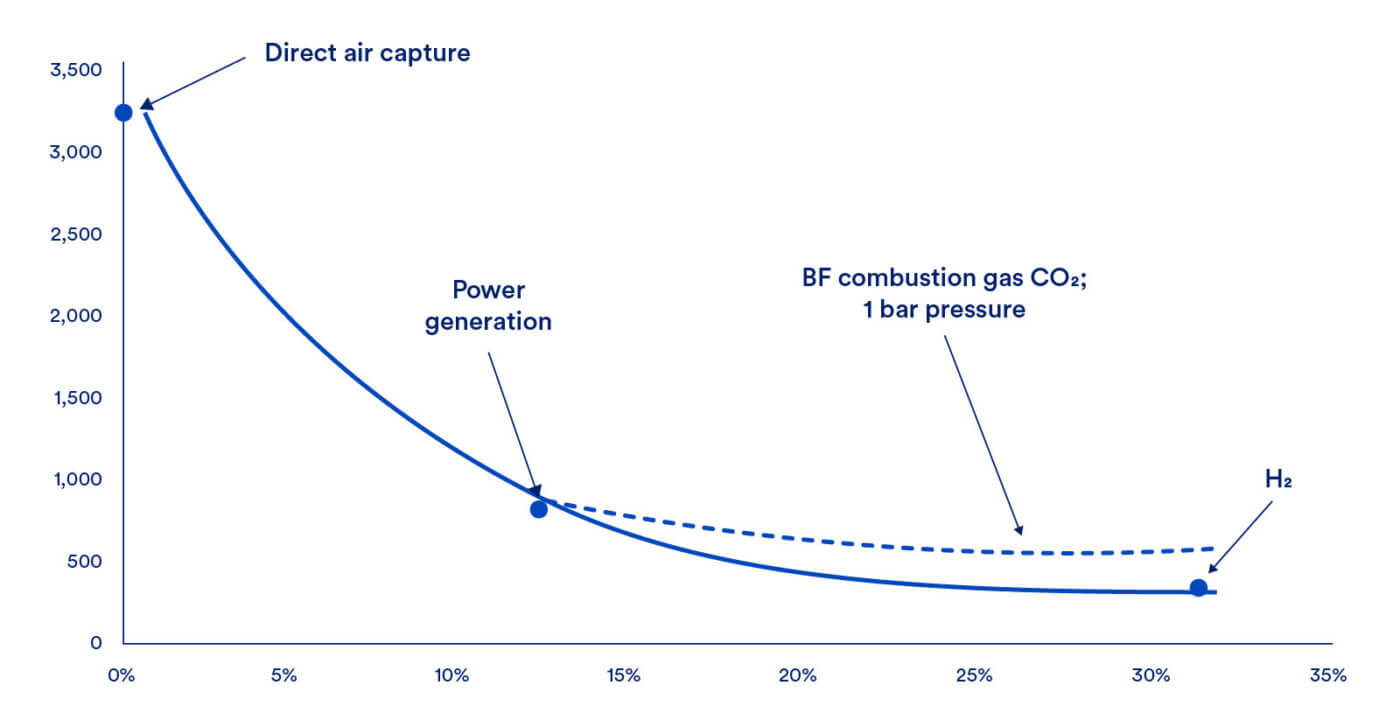

CCS requires the separation of CO2 from exhaust gases, allowing it to be transported and injected into deep geological formations for permanent storage. CCS can significantly reduce the carbon footprint of an integrated steel production facility, but the approach will be challenged as the level of desired decarbonization increases beyond a certain point. Integrated steel mills have multiple emission sources, requiring carbon capture to be installed at various points in the facility, each providing increased abatement, and increasing cost. The process off-gasses produced by a coke battery, blast furnace and basic oxygen furnace contain a significant amount of energy content. Various amounts of this gas can be used for heating processes within the plant, sold on the open market, or flared for safety or process configuration reasons. However, these off-gases are often routed to a power plant, where it is used to produce steam and electricity for use at the steel plant. The fact that these off-gases are routed to a central location allows for a large single point-of-capture for a CCS system.

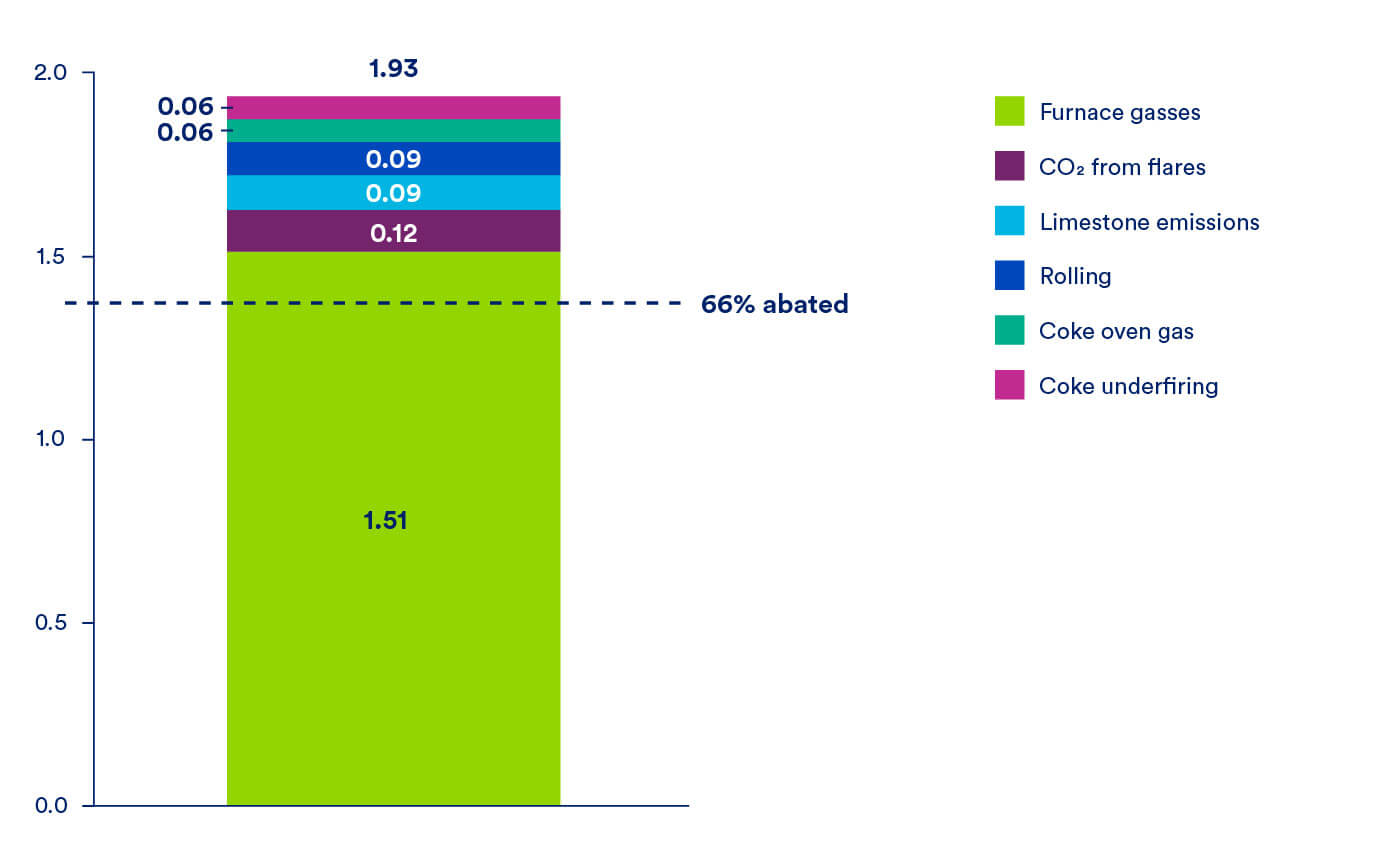

Figure 30: BF-BOF CCS capture scenarios at 85% efficiency on the treated stream. Mt CO2, %

Note: Model assumed a 15% scrap rate and therefore may have higher direct emissions than a typical U.S. integrated mill. Excludes emissions from upstream coal production.

Figure 31: CCS installation points for BF-BOF integrated mill

By maximizing the redirection of off-gases from the blast furnace and BOF to the on-site power station, and installing CCS at the power station (capture rate of 85%), integrated mills could abate up to 66% of their total direct carbon emissions as shown in Figure 30. Given that most, if not all integrated mills have a power station, this route will not be unique to a single mill or group of mills.

The blast furnace hot stoves represent another large source of CO2 emissions. However, a 90% capture rate on the blast furnace hot stove would only result in a reduction in total direct plant emissions of up to 20% due to their isolated nature. Unlike the furnace off-gases, hot stoves exhaust cannot be rerouted to the power station effectively; so separate capture equipment would need to be installed locally to abate their gasses.

The continuous and pressurized flow of gas direct from a blast furnace offers the potential for lower-cost separation of CO2(i.e., pre-combustion capture) but, by itself, a direct-to-furnace installation can only achieve a 30% reduction in emissions, based on blast furnace gas properties and available capture technology. Again, this approach would increase the required cost to reach full abatement as additional capture equipment would need to be installed on the other emissions points.

Although integrated mills could install CCS on their blast furnace off-gas system alone, CRU expects rerouting of carbon intensive off-gases to a CCS-equipped power plant to be a more cost-effective approach on a per-ton basis. However, ultimately, the desired rate of capture will vary according to internal goals and regulatory requirements and, if blast furnace capture alone can meet a mill’s abatement goals, then it will likely be the chosen approach.

In addition to the actual steel production process, thought needs to be given to ancillary facilities such as coke batteries, sinter plants and pelletizing plants (which provide iron ore pellets for both integrated and DRI plants). In the case that these facilities are not on site, they would require individual, separate carbon capture to fully decarbonize. The overall emissions from these facilities will be low and so the unit cost of necessary capture facilities will be high given scale economy effects. Thus, this route has not been considered here.

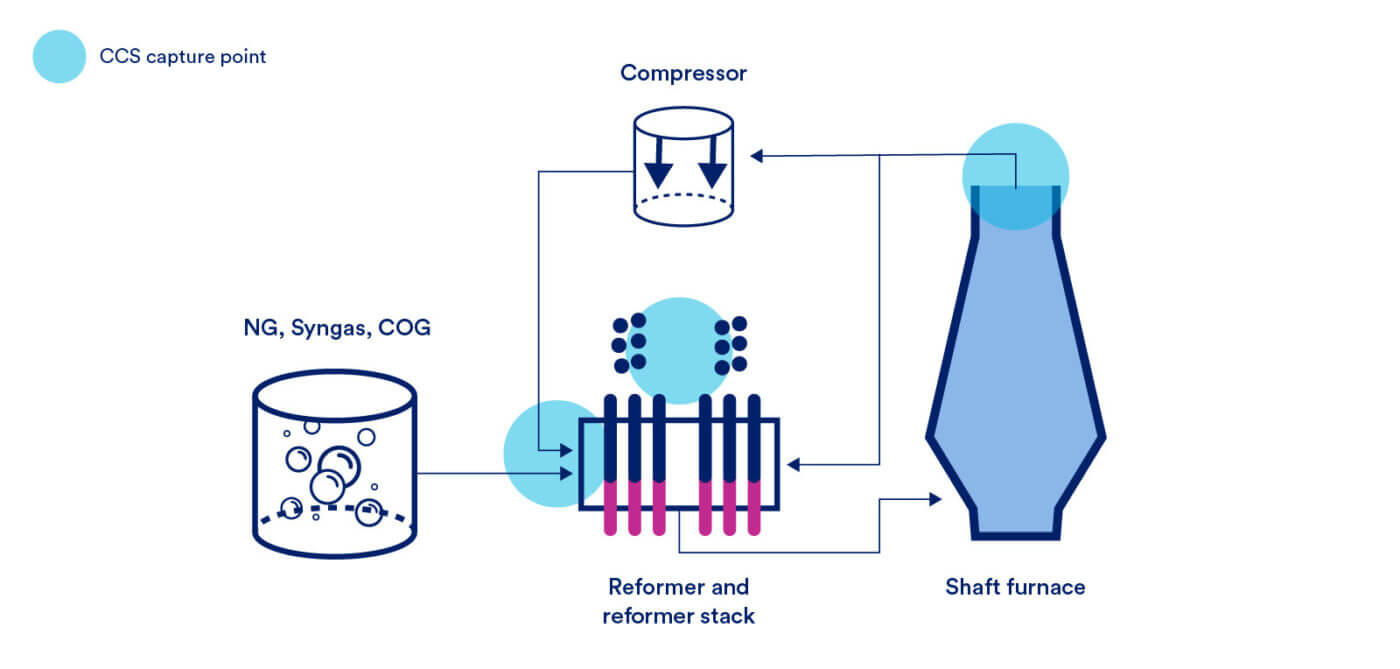

Carbon capture for natural gas and hydrogen DRI

The demand for DRI will continue to grow as EAF and SAF steelmaking require a steady supply of ore based metallics. Thus, the steel industry must address scope 1 emissions from DRI production that will comprise most of the EAF and SAF scope 3 profile. Although hydrogen-based reduction will likely be one of the long-term solutions to this issue, the speed at which this technology will be integrated on a large scale is likely to be slow, given costs, hydrogen availability and technology readiness. In this case, CCS is considered a potentially viable abatement method for DRI and blast furnace iron production as it could provide significant carbon reduction in the nearer term.

There are two main DRI production technologies, Midrex and Energiron, but how the CO2 is handled differs by process. In a Midrex facility, natural gas is first converted to CO and H2 in a reformer. Around 25% of the input energy is used for heating; the remainder is involved in the reduction reaction and so is contained in the process gas at the top of the shaft furnace or is contained in the product DRI (~15%). Process gas is scrubbed on exit from the shaft, and some is recirculated to the reformer as a heating gas, producing CO2 which is emitted via the reformer stack. The remainder of the process gas is mixed with the natural gas input to the reformer, where the CO2 content takes part in the reforming reaction to produce CO and H2. The proportion of process gas recirculated through the reformer is controlled to manage the stoichiometric ratio of inputs and optimise the process. Ultimately, however, all CO2 produced by the process is emitted via the reformer combustion stack.

In contrast, Energiron does not have a separate reformer and reducing gases are produced from natural gas ‘in situ’ in the shaft furnace. CO2 is removed from the process gas on exiting the shaft to control the CO2 level, before the remaining process gas is recirculated back into the shaft via a gas heater. Some process gas is also diverted to the gas heater before CO2removal to provide further control of the process gas composition. Thus, partial CO2 removal is an inherent component of the process, which makes CO2 capture of this component an easier option. Ultimately, ~65% of the CO2 is emitted from the process via the inbuilt CO2 removal system and 35% is emitted from the process gas heater combustion stack. The concentration of CO2 in the heater stack will be low and so would require larger, higher cost equipment.

If a plant is fitted with Energiron DRI technology, which captures, recycles, and utilizes furnace gasses to enhance efficiency, only a compressor and associated equipment would be required to reach ~60% CO2 reduction. Both Energiron and Midrex facilities can be modified to be 100% hydrogen adaptable, allowing for true net zero emissions in the long-term. Only one of the three plants in the U.S. is equipped with such technology, the Nucor Louisiana HBI plant, and Energiron cannot be retrofitted. For Midrex plants, a CO2 removal system could be retrofitted on the process top gas stream (where the higher concentration of CO2 allows for relatively low-cost capture), but this would only allow ~55% of CO2 to be captured. A capture system on the reformer stack would allow more complete capture, but the lower concentration of CO2 in the stack gas would require larger equipment, incurring additional costs.

Figure 32: CCS installation points for DRI

A few production pathways define the most likely methods of future steelmaking in the U.S.

BF-BOF: The blast furnace to basic oxygen furnace route, sometimes referred to as “integrated steelmaking”, has been the primary route for producing steel globally since the 1950s. It utilizes coke (heat processed coal) and sinter and/or pellets (processed iron ore) to produce a pure iron product in liquid form (hot metal) that is used in an oxygen furnace to make steel. The U.S. currently has 8 BF-BOF facilities (six of which are operational) that will look to develop decarbonization strategies through one of the following pathways.

BF-BOF with CCS: Integrated mills can utilize carbon capture and storage to reduce their carbon emissions by installing a system on one or more of the key emissions points outlined in Figure 31.

Submerged arc furnace (SAF) / Electric melt furnace (EMF): The SAF or EMF is a type of electrically powered melting furnace, like an EAF. In the context of steelmaking, these furnaces take solid iron from a DRI plant and melt it into liquid iron, which can be used in a BOF or EAF in a manner almost identical to the way that hot metal is used from a blast furnace. When installed in an integrated facility, the steel production process from the BOF to final product is unchanged, requiring no other changes to the mill’s equipment while maintaining the same product portfolio. SAF furnaces are also more capable of removing high levels of slag than an EAF, which allows the DRI plant to utilize lower quality, blast-furnace grade iron ore pellets. Because the process consumes DRI, steelmakers will have the choice to utilize hydrogen or natural gas in the ironmaking process, resulting in diverging pathways.

Modern installations can take hot DRI directly from the plant (at roughly 650°C) and charge it directly into the SAF or EMF, saving significant amounts of energy. SAF/EMF technology is very mature, having been used for many years in the production of steelmaking ferroalloys, but there are only a small number of installations in use for high-volume steelmaking. In the U.S., Steel Dynamics uses an SAF at its Iron Dynamics facility in Indiana to melt solid DRI and feed it into a standard EAF.

DRI-SAF-BOF with CCS: Carbon capture can be installed on the SAF pathway on a few different points. Both the DRI plant and the basic oxygen furnace can be equipped with carbon capture, providing varying levels of abatement depending on the melt chemistry and number of capture systems. For the analysis below, the capture system is installed on the DRI and BOF.

Traditional EAF: The EAF is responsible for around 70% of steel production in the U.S. The process has an inherently lower emissions level as it removes coal mining, coking, blast furnaces, and the basic oxygen furnace from the steelmaking process. Scrap-based EAFs can utilize up to 100% scrap, further reducing their scope 3 footprint. A majority of EAF emissions come from electricity consumption and the use and transport of OBM inputs. Thus, the decarbonization pathways for EAFs focus on scope 2 and 3 emissions.

Clean energy traditional EAF: The clean energy pathway for EAFs provides a route for decarbonization at a relatively lower cost compared to alternative methods of abatement. However, the source of renewable energy will have a significant influence on costs, as energy storage systems might be required for intermittent sources. By switching from fossil fuel-based electricity to clean energy, producers can almost eliminate scope 2 emissions.

DRI-EAF: OBMs will continue to play a key role in the EAF value chain. As of now, many EAFs globally utilize high-quality pig iron produced in blast furnaces that use coal, leading to relatively high scope 3 emissions. These emissions can be reduced by switching from coal-based pig iron to natural gas produced DRI, as is done in the U.S.

NG-DRI-EAF with CCS: For this pathway, carbon capture is installed on the DRI plant top gas stream which will abate between 55% and 60% of the CO2 emitted, thus lowering scope 3 emissions for the EAFs it supplies. Higher capture rates could be achieved by applying CCS to the reformer stack. Although there is some interest in developing CO2 capture from the EAF, its emissions (associated with carbon from the graphite electrodes and the iron) are comparably low, leading to relatively high abatement costs.25

H2-DRI-EAF: Traditional DRI production methods using natural gas, syngas, or other fossil fuel-based reductants promotes high carbon iron reduction. DRI producers can reduce their emissions by utilizing low-carbon hydrogen as a partial, or full reductant source. The transition to hydrogen DRI can be done gradually, allowing for delayed, or planned investment that does not sacrifice existing capacity. For instance, DRI or HBI produced to serve the EAF can be fed into blast furnace operations during the EAFs capacity ramp-up.

Hydrogen-based pathways offer significant abatement opportunity, with inherent flexibility, but the use of hydrogen at higher concentrations alters the chemical energy balance of ironmaking. Unless carbon-containing gasses are used in the initial reduction process, the resulting iron units will contain insufficient levels of carbon. Thus, additional carbon units must be injected into the melt when producing steel in the EAF or BOF. The injected carbon is less energy efficient, meaning that mills will require a higher volume of carbon units per ton of steel produced, increasing direct CO2 emissions.

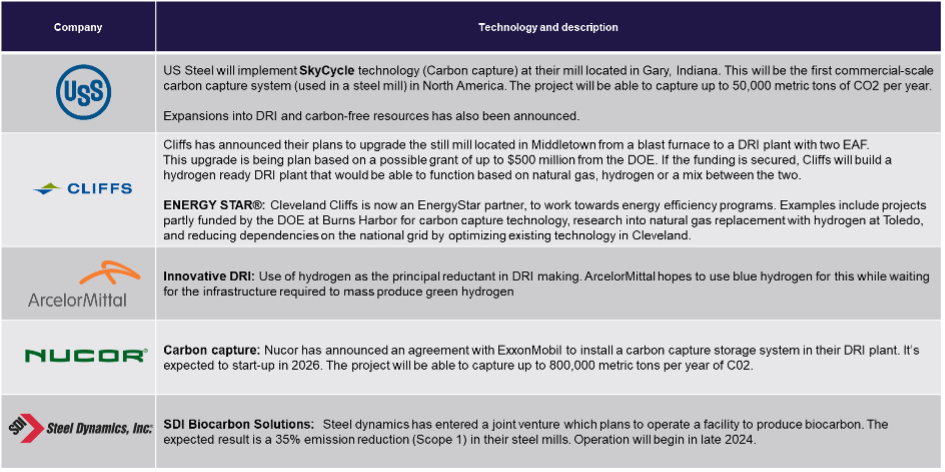

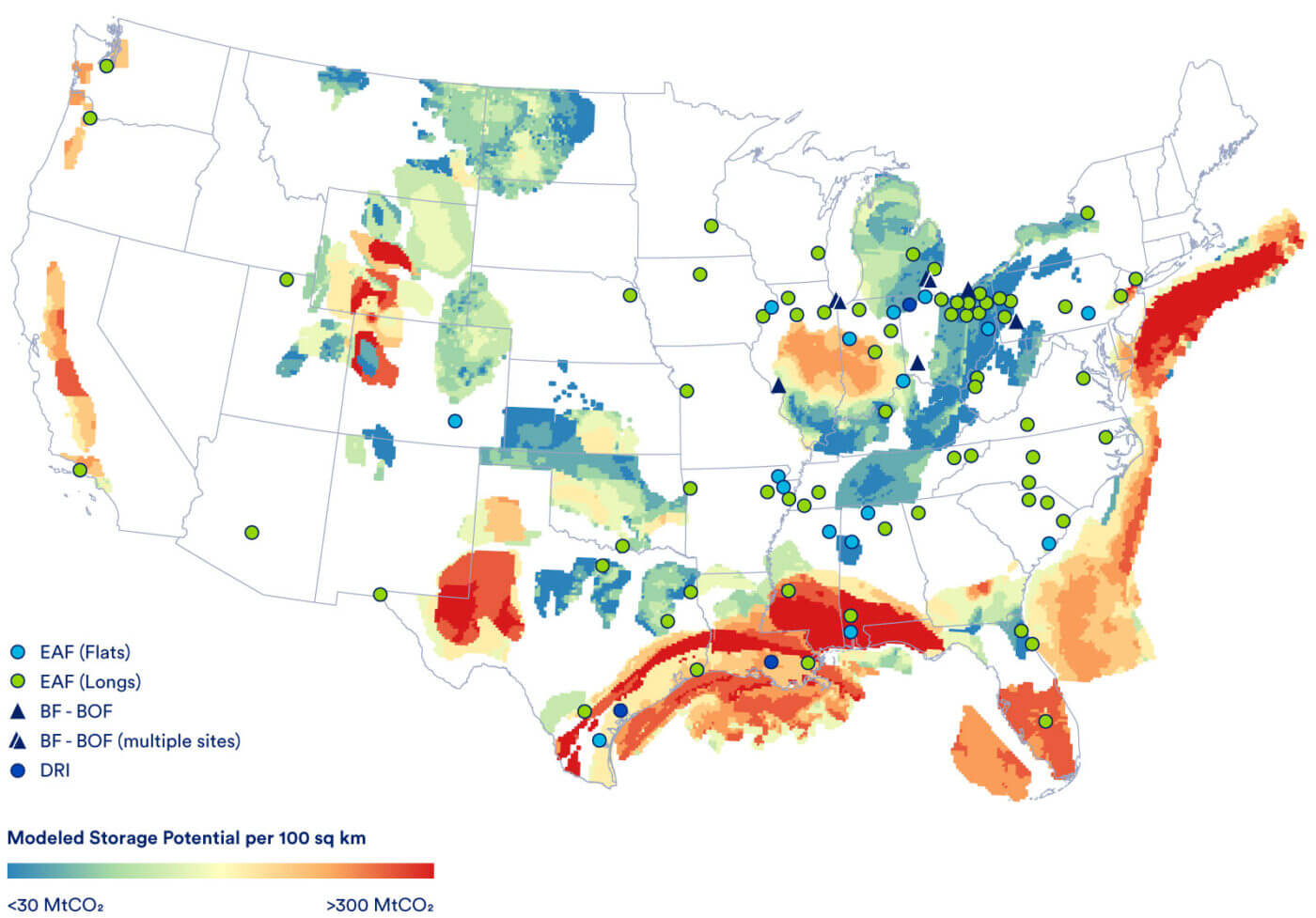

The large cluster of BF/BOF plants in northwest Indiana (Cleveland Cliffs Indiana Harbor, Burns Harbor, and U.S. Steel Gary) are in the best position to implement CCS, as they are close enough to utilize shared infrastructure, with significant storage capacity available within 150 miles in central Illinois. This geographic region contains significant amounts of other heavy industry, which could also make use of any CCS infrastructure. USS Mon Valley and Cleveland Cliffs Cleveland plant are both close to storage in eastern Ohio but are too far apart to share infrastructure; they could benefit from the implementation of either CCS or DRI. Table 3 below summarizes the decarbonization pathways currently being explored or implemented by domestic steel producers.

Table 3: Steelmaking decarbonization developments in the U.S.

Decarbonization pathway methodology and results

CRU developed the following methodology to identify and analyze feasible steelmaking pathways, ranging from status quo “baseline” production methods to highly advanced alternatives which have not yet been commercialized. The methodology deconstructs current and future steelmaking pathways into individual options that are grouped into process pathway categories including 1) iron ore source, 2) reductant, 3) ironmaking technology, 4) iron unit source, 5) steelmaking technology, and 6) carbon capture as shown in Table 4. The table includes the relative impacts to employment for adopting different pathways. Recent announcements have shown up to 6% increases in employment in replacing a blast furnace with a DRI and SAF.

The options within each pathway have been identified and check marked in the following table. For example, a BF-BOF pathway requires 1) BF pellet iron ore, 2) coal/coke as a reductant, 3) ironmaking via a blast furnace, 4) resulting in hot metal, which is 5) converted to steel in a basic oxygen furnace. A BF-BOF with CCS will follow the same pathway as a traditional BF-BOF but require additional capital and operating expenses to implement carbon capture technology. The NG-DRI-SAF pathway echoes the recent announcement by Cleveland Cliffs that they plan to transition from the traditional BF-BOF operation to a DRI with EMF at their Middleton facility. A traditional EAF starts with 1) scrap as the iron unit source which is 2) converted to steel using an EAF.

Table 4: Feasible steelmaking pathways

Comparison of pathway costs and abatement levels

The following section presents the CapEx, OpEx, CO2 abatement, CO2 intensity, abatement cost, and expected years to commercialization of each pathway presented in Table 4.

Table 5: Summary matrix of steelmaking configurations

| Key pathways | CapEx ($/t capacity)27 | OpEx ($/tcs) | CO2 intensity (t CO2/tcs)28 | CO2 abatement (t CO2/tcs)28 | CO2 abatement cost ($/t CO2)28,29 | Years to commerc-ialization |

|---|---|---|---|---|---|---|

| Traditional BF-BOF (Baseline) | 0 | 570 | 2.21 | – | – | 0 |

| Green H230 DRI SAF BOF | 900 | 841 | 0.22 | 1.99 | 175 | 6 |

| Blue H2 DRI SAF BOF | 900 | 708 | 0.77 | 1.44 | 149 | 5 |

| NG DRI SAF BOF CCS | 1,530 | 601 | 0.94 | 1.27 | 129 | 4 |

| BF-BOF with CCS | 420 | 647 | 1.14 | 1.07 | 115 | 4 |

| NG DRI SAF BOF | 900 | 589 | 1.27 | 0.94 | 104 | 0 |

| Clean-e Traditional EAF | 450 | 591 | 0.53 | 1.6831 | 36 | 0 |

| Traditional EAF | 450 | 571 | 0.77 | 1.44 | 40 | 0 |

| Green H2 DRI EAF | 1,000 | 748 | 0.17 | 2.04 | 130 | 6 |

| Blue H2 DRI EAF | 1,000 | 748 | 0.17 | 2.04 | 130 | 6 |

| NG DRI EAF CCS | 1,070 | 548 | 0.82 | 1.39 | 51 | 4 |

| NG DRI EAF | 1,000 | 537 | 1.04 | 1.17 | 45 | 0 |

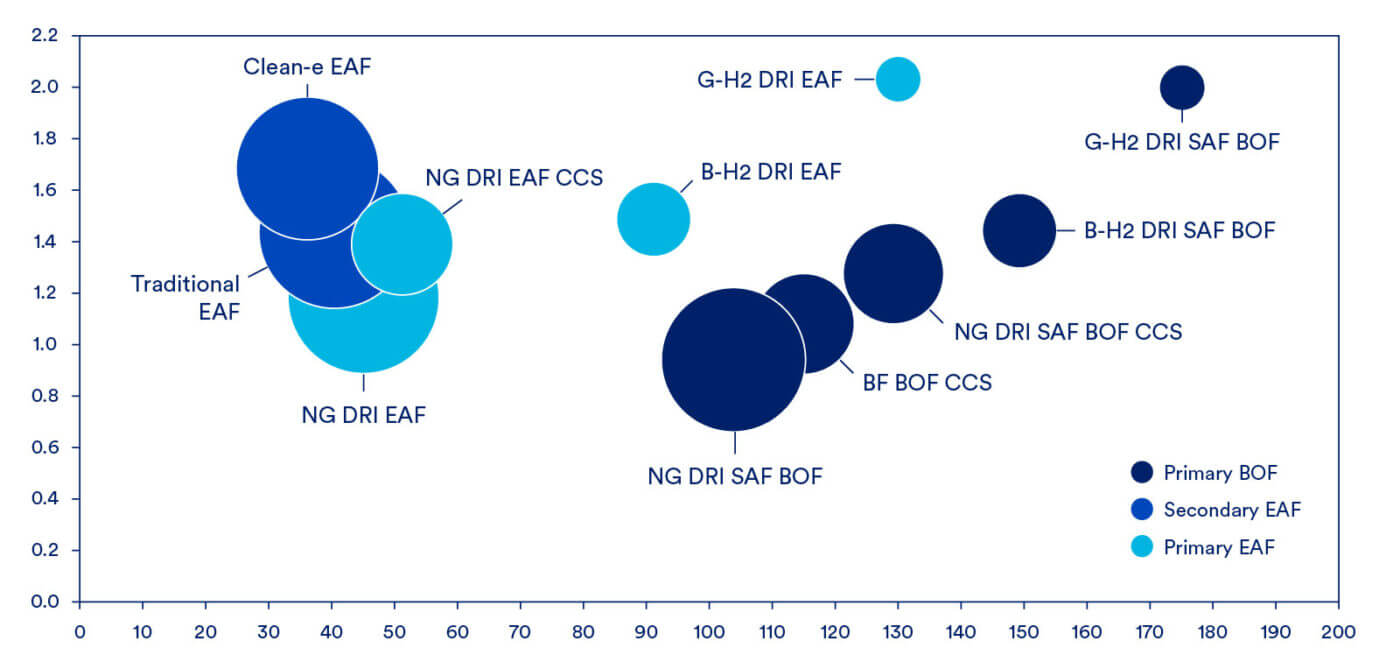

Figure 33: Abatement pathways, x-axis: Abatement cost ($/t CO2), y-axis: Actual abatement (t CO2/tcs), bubble size represents years to commercialization (larger bubble equals earlier adoption)

Note: Figure 33 shows abatement of scope 1 and 2 emissions in addition to scope 3 emissions, except for natural gas supply chain emissions. See next section.

Natural gas supply chain considerations32

Natural gas-based DRI production in the United States consumes significant quantities of natural gas, approximately 264 Nm3 per ton of DRI produced.33 While not included in CRU’s scope 3 figures throughout this report, the emissions contributions from the natural gas supply chain can and do have significant impacts to the scope 3 profile of DRI. The blue hydrogen DRI pathways are also impacted by these emissions. Production of hydrogen for these pathways consumes approximately 320 Nm3 of natural gas per ton of DRI produced.34 Finally, natural gas and coal are used to generate a large portion of electricity in the U.S., so there are emissions upstream of the power plant (for both fuels) that are attributable to power consumption for steelmaking using commodity grid electricity as opposed to low-carbon electricity. Generally, in the natural gas supply chain, the emissions contribution (CO2e) component from the methane emissions exceed those from the CO2 component, but the ratio of contribution will vary depending on source of natural gas; in any case reducing methane emissions (in addition to CO2 emissions) is an important climate mitigation goal and strategy.

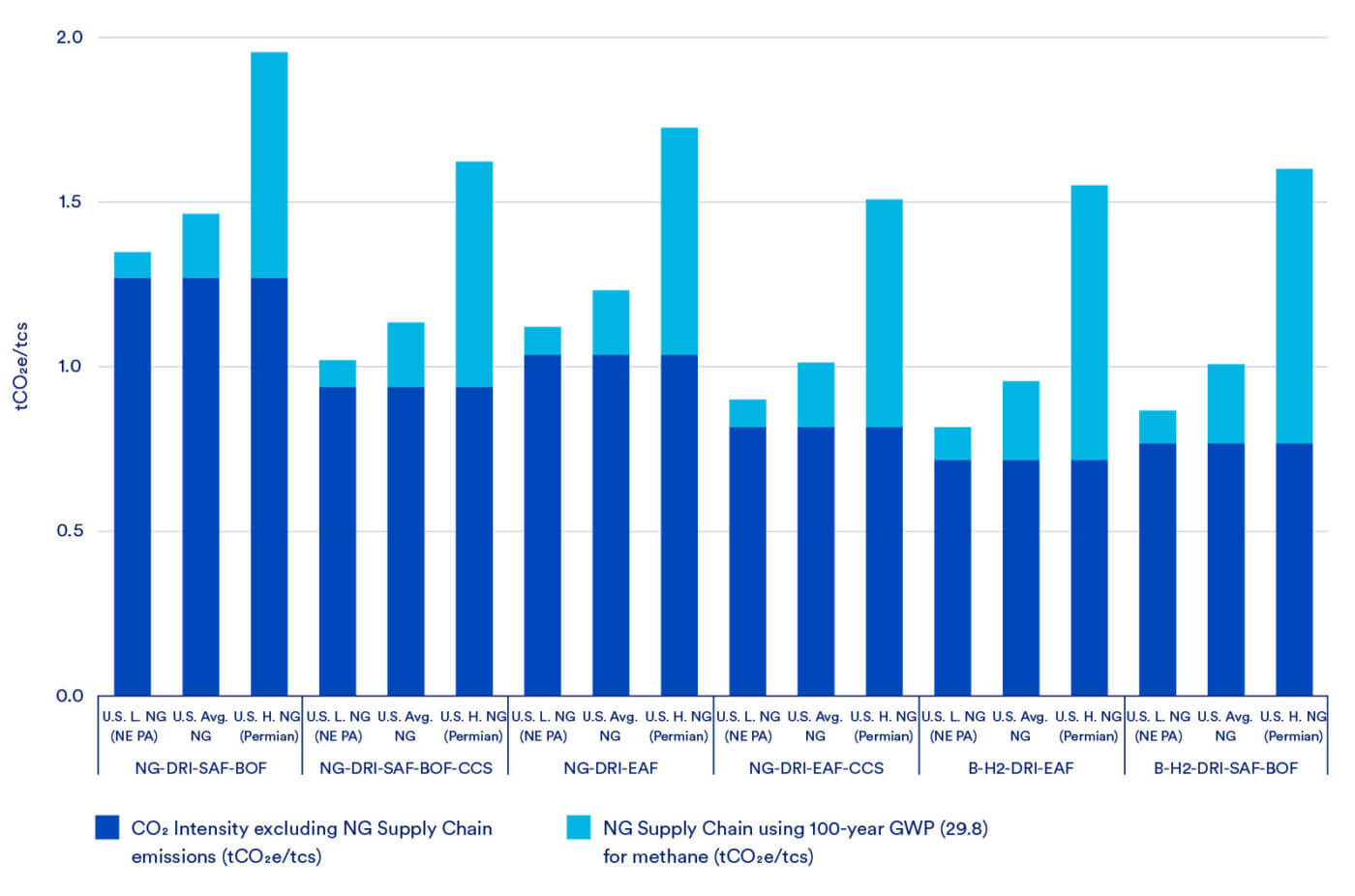

To illustrate the importance of upstream natural gas emissions for hydrogen- and natural gas-based DRI, we used CATF’s methodology32 for calculating the contributions of both methane and CO2 emissions associated with the natural gas supply chain to perform a sensitivity analysis using three U.S. sources of natural gas representing high (Permian), national average, and low (Appalachian) supply chain emissions. The results presented in Figure 34 show each pathway’s total CO2e intensity, including the associated emissions from the natural gas supply chain, for various sources of natural gas.

Figure 34: Total CO2e emissions impacts (scope 1, 2, and 3) from NG-DRI & B-H2-DRI steelmaking pathways including natural gas supply chain emissions for U.S. Average, U.S. High (Permian), and U.S. Low (Appalachian) gas (tCO2e/tcs)

Note: Methodology based on https://www.catf.us/resource/analysis-lifecycle-greenhouse-gas-emissions-natural-gas-coal/

The overall emissions intensity of the NG-DRI pathways could increase by approximately 6% to 84% depending on the source of natural gas and production pathway. Even though both the NG-DRI-EAF and NG-DRI-EAF-CCS pathways consume similar amounts of natural gas per ton of DRI produced, the emissions from the natural gas supply chain make up a larger proportion of the overall emissions in CCS pathway due to lower direct emissions and therefore have a greater potential to impact the total emissions profile. Similarly, the overall emissions intensity of the Blue H2 DRI pathways could increase by approximately 13% to 116% depending on the source of natural gas used to produce hydrogen and the steel production pathway. Because of the higher natural gas usage in Blue H2 pathways when compared to the NG-DRI pathways, the supply chain impacts are also higher. Even in scenarios with the highest emissions from the natural gas supply chain, total emissions of any DRI pathway are still lower than an unabated BF-BOF plant. Reductions in the carbon intensity of the natural gas supply chain would significantly lower the total scope 3 emissions profile for DRI.

It is important to note that while these upstream emissions are quite significant, they are also quite variable and it is feasible to significantly reduce these emissions, for example with regulatory emissions standards covering natural gas facilities.

Key takeaways from decarbonization pathways

Domestic steelmakers have a variety of decarbonization pathways from which to choose. To select the most feasible decarbonization pathway, a variety of constraints need to be considered, such as product portfolio, level of decarbonization, energy supply, hydrogen availability, CCS locations and infrastructure. The following sections outline the key constraints of each pathway, and the tools steelmakers will use to reach partial or full decarbonization.

Integrated mills will take advantage of alternative iron production as the first step

Switching iron production from a blast furnace to a DRI-SAF facility utilizing natural gas is a currently available pathway for U.S. integrated mills. This will achieve partial decarbonization and will prepare for the future use of hydrogen at the DRI facility, while allowing the mill to operate the BOF and downstream facilities with no modifications. The BF-BOF with CCS pathway offers similar levels of abatement at a slightly higher cost, but it does not allow for the potential future conversion to green hydrogen that a DRI plant provides. For deep decarbonization, one likely path for integrated mills will be a green hydrogen fuelled DRI plant feeding into an SAF, which will then feed liquid iron into the BOF. Another option for this pathway is to utilize blue hydrogen as an intermediate step before making the full transition towards green hydrogen. The flexibility to drive deeper decarbonization levels via hydrogen without expending significant additional CapEx on the DRI plant is an advantage of the DRI production route. This specific transition is already planned for the Middleton facility owned by Cleveland-Cliffs, where they are building a DRI facility along with two SAFs to replace a blast furnace.

An EAF powered with clean electricity and using natural gas produced DRI will have a relatively small carbon footprint

The clean electricity scrap-based EAF has the lowest abatement cost on a $/t of CO2 basis. However, it will be difficult to match the quality of steel with that of integrated steelmakers without the use of large amounts of OBM. EAF producers that do not require low residual steel to service their customers can make a switch to clean electricity to reduce emissions, with no changes to process flow. Referencing back to Figure 15, this switch would reduce the overall emissions of EAF production by roughly 20%.

EAF producers that require higher product quality will require OBMs as an input. The most logical first step will be implementing a natural gas fuelled DRI facility, particularly if that DRI can be hot charged into the EAF, lowering the amount of electricity needed to melt the DRI. The NG DRI EAF will achieve higher abatement relative to the NG DRI SAF BOF pathway, at a significantly lower operating cost. Making the switch to NG DRI iron production along with a switch to clean electricity is a pathway that is available and in use today. To further decarbonize the production process, the operator will have the option to either install CCS on the DRI plant or switch to green hydrogen, both providing higher levels of abatement, with CCS being more cost effective.

Several key constraints will impact the speed and cost of adopting new steelmaking pathways

Plant age and configuration will challenge the viability of decarbonization pathways for U.S. integrated mills

The integrated steel mills in the U.S. have a long history of steelmaking. These facilities are relatively old, which limits the options for easily integrating carbon reduction technologies. Pathways are limited by plant design, zoning, location, and financial constraints. On a more positive note, most steel producers route their process off-gases through a variety of scrubbers and baghouses to minimize emissions and maintain compliance with environmental regulations, which provides potential collection points for CCS.

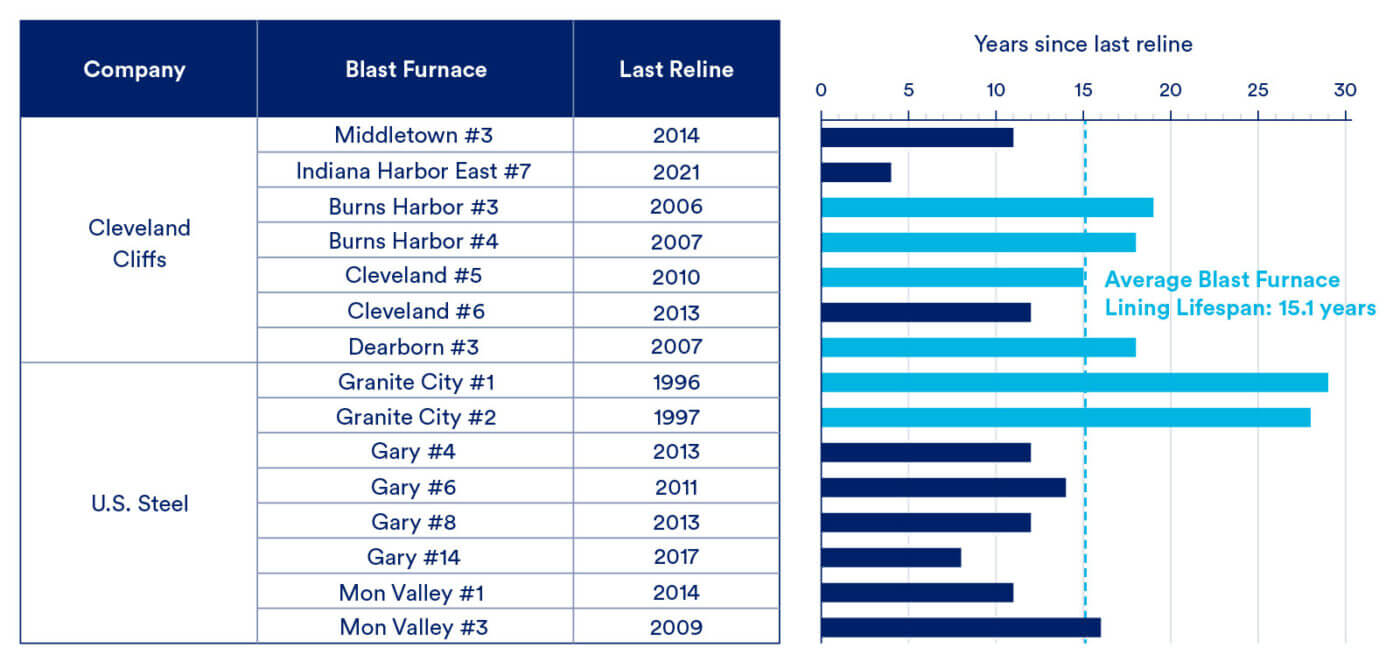

Plant age will dictate the time-cost effectiveness of installing carbon capture technology. As with all capital investments, there is a payback period for CCS equipment. If a mill is expected to reline or shut down, investments in facility upgrades are less likely. Recent scheduled facility relines in the U.S. have been delayed or postponed over public disapproval regarding continued mill emissions of pollutants such as benzene, hydrogen sulfide, and PM2.5 particulates. Because of this, future relines are likely to coincide with decarbonization technology announcements, to take advantage of the facility downtime and to answer stakeholder concerns.

Figure 35: U.S. blast furnace reline timeline

Note: Reline schedules provide a measure for when a furnace is likely to come offline in the future

While some integrated mills will take advantage of CCS to maintain the production status quo, plants like Cliffs Middletown see DRI/EMF as a more effective route. It remains to be seen how the Middletown conversion will advance the decarbonization effort for other U.S. mills. The DRI-SAF switch is a suitable abatement pathway for integrated mills, but the investment is very costly ($1.8 bn for 2.7 Mt of capacity). Cliffs will run the DRI plant with natural gas, with the option to switch to hydrogen or to equip the DRI plant with CCS. Given the much lower carbon footprint of a DRI plant (particularly if the SAF is powered with clean electricity), proper incentives35 will help to justify the additional $500 million needed for CCS to abate an already reduced carbon footprint. The 45Q tax credit for carbon sequestration, for example, provides a credit of $85 per ton of CO2 captured and permanently stored. This could lead to partial or potentially full coverage of CCS OpEx costs, especially for integrated mills.

CCS on an integrated mill cannot provide full abatement but can offer a more cost-effective route when compared to a full hydrogen-DRI SAF conversion. By utilizing CCS, integrated mills achieve short term abatement but accept financial risk in the event of a conversion or shutdown. Mills which have most recently relined or committed to extended production will be more likely to adopt partial abatement strategies like CCS. On the other hand, plants like Middletown are incentivized to make more permanent changes prior to an expensive reline.

EAFs consume DRI, often produced offsite, creating a separation in the value chain. DRI facilities and the EAFs they serve bear the cost of their respective carbon capture strategies individually. In this way, both facilities are constrained by the other’s willingness to pay or willingness to accept one another’s desired abatement strategy. DRI plants which chose to produce decarbonized material, either by utilizing hydrogen or installing CCS will be subject to the associated higher costs and, if possible, will cover those increased costs via higher charges for the material sold, increasing the raw material cost for associated EAFs. DRI plants producing low-carbon DRI will depend on the market’s willingness to pay premium prices for reductions in carbon intensity that are marginal relative to the EAF’s overall emissions. Ultimately, facilities that choose to abate through a lower carbon supply chain will view clean DRI as a useful option, and may invest in their suppliers, but for those who focus their efforts on decarbonizing energy use, they may settle for the less costly, more carbon-intensive DRI that is currently available.

To reduce their carbon footprint as well as to take advantage of a market for low-carbon OBMs, some DRI producers are positioning themselves to provide low-carbon OBM. Nucor Louisiana is equipped with carbon removal technology and is capable of a 100% conversion to hydrogen reduction through its Energiron system. Plants with an existing recycling system like Energiron would only need to install a compressor and some auxiliary equipment to reach 60% abatement, greatly reducing the cost compared to a full CCS system on a standard NG-DRI plant. However, the other two DRI plants in the U.S. use a different technology (Midrex) and would require additional equipment to implement carbon capture.

The efficiency and cost of CCS depends on the location of the plant, CO2 transport, and storage process. CCS uses large, integrated systems to reroute, process, treat, and capture off-gasses from industrial processing. Although the process can reduce steelmaking emissions, there will be constraints implementing the technology given the state of their equipment, plant location, and budget. As demand for decarbonization grows, CCS can be used to reduce emissions for high-polluting industries like power generation and steel and will be an option for remaining BF-BOFs in the U.S. It may also find use in DRI plants and some EAF production where the plant’s configuration is conducive to cheaper CCS integration. CCS investments are picking up pace in Europe and the Middle East. As more projects prove technological and economic viability, this trend will grow. CRU expects clusters of CCS developments to form around prime storage locations. This will be driven by the cost relationship between a plant’s distance to storage, and the cost of transporting the captured gas. Pipelines will cost millions to install, and every additional mile that is constructed could add between $1-$3 million in CapEx, depending on pipeline diameter and building terrain.36,37,38 This range considers variable pipeline diameters that could be used for CO2 transport, but these figures are not representative of detailed modelling conducted by CRU. Clustering infrastructure and investing in CO2 pipeline corridors will provide economies of scale and synergies to reduce investment risk and the unit cost of storage.