Flaring Accountability

Global gas flaring by major oil and gas companies and their partners

Glossary and Abbreviations

Bcm | Billion cubic meters of natural gas |

Equity Ownership Attribution method | Method of apportioning flare volumes to companies based on their percent ownership stake in the flaring asset, regardless of whether they operate the asset |

Flaring Intensity | Cubic meters of gas flared per barrel of crude oil and condensate produced (m3/bbl) |

GWP | Global Warming Potential |

IEA NZE | International Energy Agency Net Zero Emissions Scenario |

IOC | International Oil Company |

JV | Joint venture |

Mcm | Million cubic meters of natural gas |

MMbbl | Million barrels |

MM(s)cf | Million (standard) cubic feet |

Mt | Megatonnes or million metric tons |

NOC | National Oil Company |

NOJV | Non-operated joint venture |

Non-routine and Safety Flaring | The World Bank refers to safety flaring as flaring of gas to ensure safe operations of the facility and non-routine flaring refers to all flaring other than routine and safety. In this report, non-routine and safety flaring are combined to mean all flaring that is not routine flaring. |

Operated Asset Attribution method | Method of apportioning flare volumes to companies that attributes the entire volume of a flare to the asset’s operator, even if they don’t own 100% of the asset |

Routine Flaring | The World Bank defines routine flaring as “flaring during normal oil production operations in the absence of sufficient facilities or amenable geology to re-inject the produced gas, utilize it on-site, or dispatch it to a market.” |

ZRF | The World Bank’s Zero Routine Flaring Initiative |

Executive Summary

Gas flaring remains a persistent global problem, one that has not improved significantly despite the introduction of direct observations of flaring from satellites and prominent global commitments to reduce the wasteful and harmful practice. In 2023, based on satellite observations, the total volume of gas flared from upstream oil and gas was 145 billion cubic meters (bcm)i—equivalent to half of Europe’s natural gas demand in that yearii—which means a global average flaring intensity of 5.0 cubic meters per barrel of oil/condensate produced (m3/bbl).iii

This report determines, for the first time, a company’s whole flaring impact around the world by attributing flaring to individual companies for both their operated and non-operated assets. Our analysis shows that just 10 large international oil companies (IOCs)—BP, Chevron, ConocoPhillips, Eni, Equinor1, ExxonMobil, Occidental Petroleum, Repsol, Shell, and TotalEnergies—are responsible for 7% of global flaring, based on their ownership percentages in flaring assets. This is an enormous amount of flaring—about 10 bcm of gas in 2023, which is enough gas to supply Norway and Austria combined.iv

The 10 IOCs analyzed are uniquely positioned to influence joint venture partners given the global reach of their operations and corporate partnerships. They have direct influence on 15% of global flaring—when accounting for the total volume of flaring that occurs at assets in which they have invested capital.

Beyond this, they have influence on nearly 40% of global flaring when considering all flaring occurring at their operations and at the companies they partner with (see Figure 13).

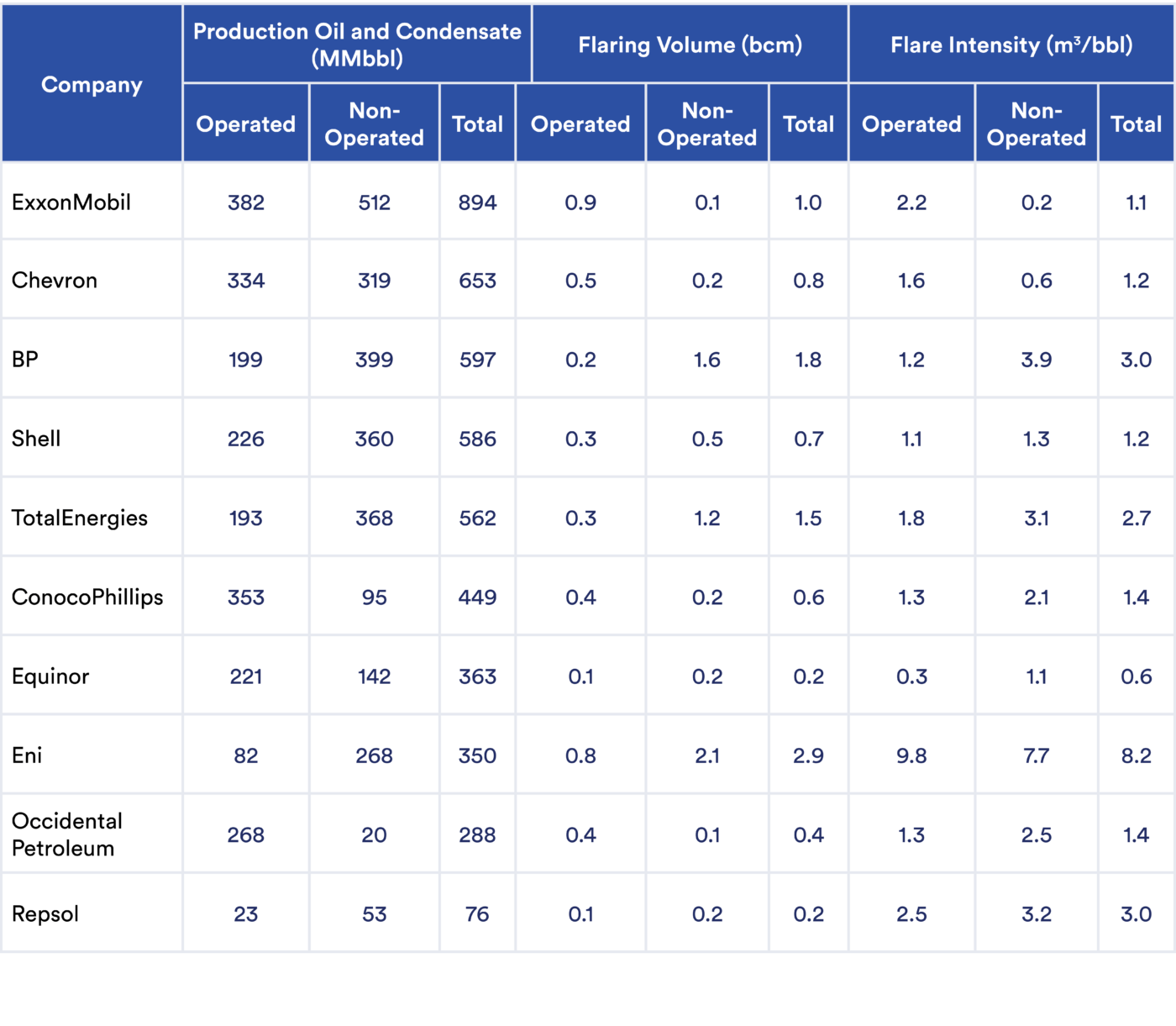

All oil and gas companies bear responsibility for flaring at assets from which they are profiting, even if they are not the operator. However, company commitments to reduce flaring largely do not apply to non-operated assets, and flaring from non-operated assets is largely missing from company reports.2 More than half of the flaring volume attributed to these companies comes from their non-operated assets. Seven of the 10 companies analyzed have higher flaring intensities at non-operated assets than operated assets (Figure 1). Given the substantial amount of investment, production, and profit the 10 IOCs obtain from these operations it is imperative that emissions reduction targets and efforts are extended to non-operated assets.

Figure 1: IOC Flaring Intensity vs Production at Operated and Non-Operated Assets3

Total oil and condensate production (x-axis), total flaring intensity (y-axis), and total flare volume (area of the bar) for each company’s operated and non-operated assets.

The oil and gas industry remains far behind necessary targets to minimize flaring to a level that meets global climate goals. Net-zero emission goals will require steep cuts in flaring. The International Energy Agency’s Net Zero Emissions Scenario (IEA NZE) includes a 95% reduction in flaring by 2030, which equates to a flaring intensity of 0.3 m3/bbl, but none of the companies analyzed has a flaring intensity below 0.6 m3/bbl (as averaged across all assets both operated and non-operated). The worst performer amongst the IOCs profiled in this report, Eni, which has been a signatory to the World Bank’s Zero Routine Flaring (ZRF) Initiative since 2015, has a company average flaring intensity of 8.2 m3/bbl (see Figure 1).3

The level of ambition must be raised to eliminate virtually all flaring at oil and gas assets around the world—both routine and non-routine—that is not legitimately emergency-related. A focus only on “Zero Routine Flaring” is no longer sufficient.The 10 IOCs have committed to ending “routine flaring” by 2030 as part of the World Bank’s ZRF Initiative, but only 30% of total reported flaring from these companies was listed as “routine” in 2022. Thus, if these IOCs only meet their target to eliminate “routine flaring,” the other 70% of flaring classified as “non-routine” may remain largely unabated. In this scenario, flaring will remain far higher than the levels required under the IEA’s net zero target (a 95% reduction by 2030).

The 10 IOCs in this report have an outsized influence on global flaring. The companies are critical global actors because they have made commitments to end “routine flaring” throughout their operations, they have substantial ability to influence flaring through their joint ventures and partnerships around the world, and they have the technical skills and financial resources to assist more resource-constrained companies in low- and middle-income countries with whom they partner.

Moving the oil and gas industry from targets to action—and measurable, real-world methane and flaring reductions—requires an effective combination of regulatory, financial, and economic levers alongside technical solutions and company leadership. For IOCs, building alignment with other joint venture partners around flaring reduction goals is often an essential prerequisite to advancing flare-gas capture projects. Well-designed and enforced regulations can play a critical role in directly reducing flaring and creating an enabling environment for flare reduction. Financial institutions and other private sector stakeholders also play a key role in leveraging positive and negative incentives to reduce flaring. Flaring is a large but very solvable problem. While existing efforts to capture and utilize gas that would otherwise be flared are commendable, the pace of these projects must be sped up drastically in order to match the size of the problem on a global scale.

Footnotes

- Equinor is a majority state owned company but has many international joint ventures and international operations and has therefore been included in this report.

Only one company, Chevron, reports flaring volume from non-operated assets in their annual sustainability report.

Following publication, Eni provided additional data that more accurately represented the company’s ownership shares in Libya and supplied detailed documentation on divestments in Congo and Nigeria. As a result of these updates, Eni’s overall intensity reduces from 8.2 to 7.1 m3/bbl. Specifically, the non-operated intensity decreases from 7.7 to 6.7 m3/bbl and operated intensity adjusted from 9.8 to 8.3 m3/bbl.

Credits

Report Authors: Lesley Feldman, Heny Patel, and James Turitto

Contributors: Ioannis Binietoglou, David McCabe, Felicia Douglas, Brandon Locke

For questions or comments about this report, please contact: James Turitto, CATF, [email protected]

Data analysis was performed by Clean Air Task Force with the support of the Mathematics, Computer Science and Artificial Intelligence Lab (MCSAI Lab), Faculty of Public and One Health, University of Thessaly, Greece. We thank Evie Hammer for excellent research support during the project. Flaring analysis is based on the VIIRS Nightfire (VNF) nightly data produced by the Earth Observation Group, Payne Institute for Public Policy, Colorado School of Mines. Rystad Ucube dataset was used for underlying equity production and operator tagging of assets.

The cover photo is a satellite visualization of oil and gas flaring in Algeria. Contains modified Copernicus Sentinel-2 data (2023), visualized using the QuickFire script developed by Pierre Markuse.

The Flaring Problem

Flaring is a common practice used by industry to burn associated and excess gases during the exploration, production, processing, and transportation of oil and gas. The environmental, climate, and health impacts of gas flaring are significant. The combustion process emits carbon dioxide (CO2), a primary greenhouse gas, along with other hazardous air pollutants that pose detrimental effects to human health and the environment. Globally, over 4% of natural gas production is flared;v in addition to being a large source of pollution, this practice is a huge waste of natural resources, as no value is realized from this gas as it is burned off.

Moreover, methane—a potent greenhouse gas—is also released due to incomplete combustion at the flare; the less efficient the flare, the more methane is emitted. The World Bank estimates that in 2023 flaring was responsible for 381 million tons of CO2 equivalent (CO2e), of which 45 million tons CO2e (~12%) was “methane slip” from incomplete combustion. This amount of methane emitted to the atmosphere is significant and even still, it likely underestimates the true real-world volume and impact.4 With a warming potential over 80 times greater than CO2 over a 20-year period, reductions in methane emissions can have a more immediate impact on slowing the rate of global warming. Beyond its impact on the climate, researchers in several countries have found increased health risks in communities close to gas flares, due to the release of particulate matter and other harmful pollutants. In a report published in 2023, CATF found that in 18 oil exporting nations, 10 million people live close to active flares (within 5 kilometers), including a half million people who live very close to flares (within 1 kilometer).vi The science is clear—reducing methane is an opportunity that we can’t afford to pass up. As flaring is a major source of both CO2 and methane emissions from the oil and gas industry, reducing and managing this wasteful and harmful practice must be a priority for all oil and gas companies.vii

Several countries have adopted regulations to reduce flaring. The effectiveness of these regulations varies by country, with some nations having more stringent enforcement than others. Furthermore, some regulations that too narrowly focus on flaring may lead to unintended consequences, such as increased venting (the release of un-combusted methane into the atmosphere) due to financial penalties for flaring,viii which up until now has been easier to observe than venting. Corporate practice and the political will of regulators plays a significant role in the amount of flaring that occurs. In basins and regions that have a higher propensity for flaring, investments in technologies to minimize flaring must be built into engineering and financial plans at the start of an asset’s development cycle or proactively added as retrofits at existing sites.

Minimizing flaring has multiple benefits:

- Reduces emissions that contribute to climate change,

- Protects the health of populations living near flares,

- Addresses energy security in regions with limited access to natural gas if gas that would otherwise be flared is moved to market,

- Provides revenue for companies from gas that would otherwise be wasted, and

- Does not require drilling new production wells.

Footnotes

4. The World Bank flaring methane emissions estimate uses the 100-year Global Warming Potential (GWP) rather than the 20-year GWP and it assumes a destruction efficiency of 98%, which is much higher than observed in many parts of the world. Adjusting this to assume a 94% destruction efficiency would triple the methane emissions estimate. Methane is a short-term pollutant remaining in the atmosphere for about 12 years, a GWP20 better reflects the impact of methane on global warming and a GWP100 understates the actual impact of methane emissions over a shorter time horizon. The GWP100 for methane is 29.8 and the GWP20 is 82.5.

Credits

Report Authors: Lesley Feldman, Heny Patel, and James Turitto

Contributors: Ioannis Binietoglou, David McCabe, Felicia Douglas, Brandon Locke

For questions or comments about this report, please contact: James Turitto, CATF, [email protected]

Data analysis was performed by Clean Air Task Force with the support of the Mathematics, Computer Science and Artificial Intelligence Lab (MCSAI Lab), Faculty of Public and One Health, University of Thessaly, Greece. We thank Evie Hammer for excellent research support during the project. Flaring analysis is based on the VIIRS Nightfire (VNF) nightly data produced by the Earth Observation Group, Payne Institute for Public Policy, Colorado School of Mines. Rystad Ucube dataset was used for underlying equity production and operator tagging of assets.

The cover photo is a satellite visualization of oil and gas flaring in Algeria. Contains modified Copernicus Sentinel-2 data (2023), visualized using the QuickFire script developed by Pierre Markuse.

State of Global Flaring

Global flaring estimates based on satellite data are useful for assessing global, regional, and country-level flaring trends. The World Bank has published such data on global flaring volumes since 2012. The data shows the total volume of gas flared from upstream oil and gas in 2023 was 145 billion cubic meters (bcm).ix Flaring rose by 9 bcm from 2022 to 2023 while oil production only grew by one percent, resulting in an increase in flaring intensity from 4.7 m3/bbl to 5 m3/bbl (see Figure 2).x

Figure 2: World Bank Global Flaring and Methane Reduction Partnership (GFMR)xi

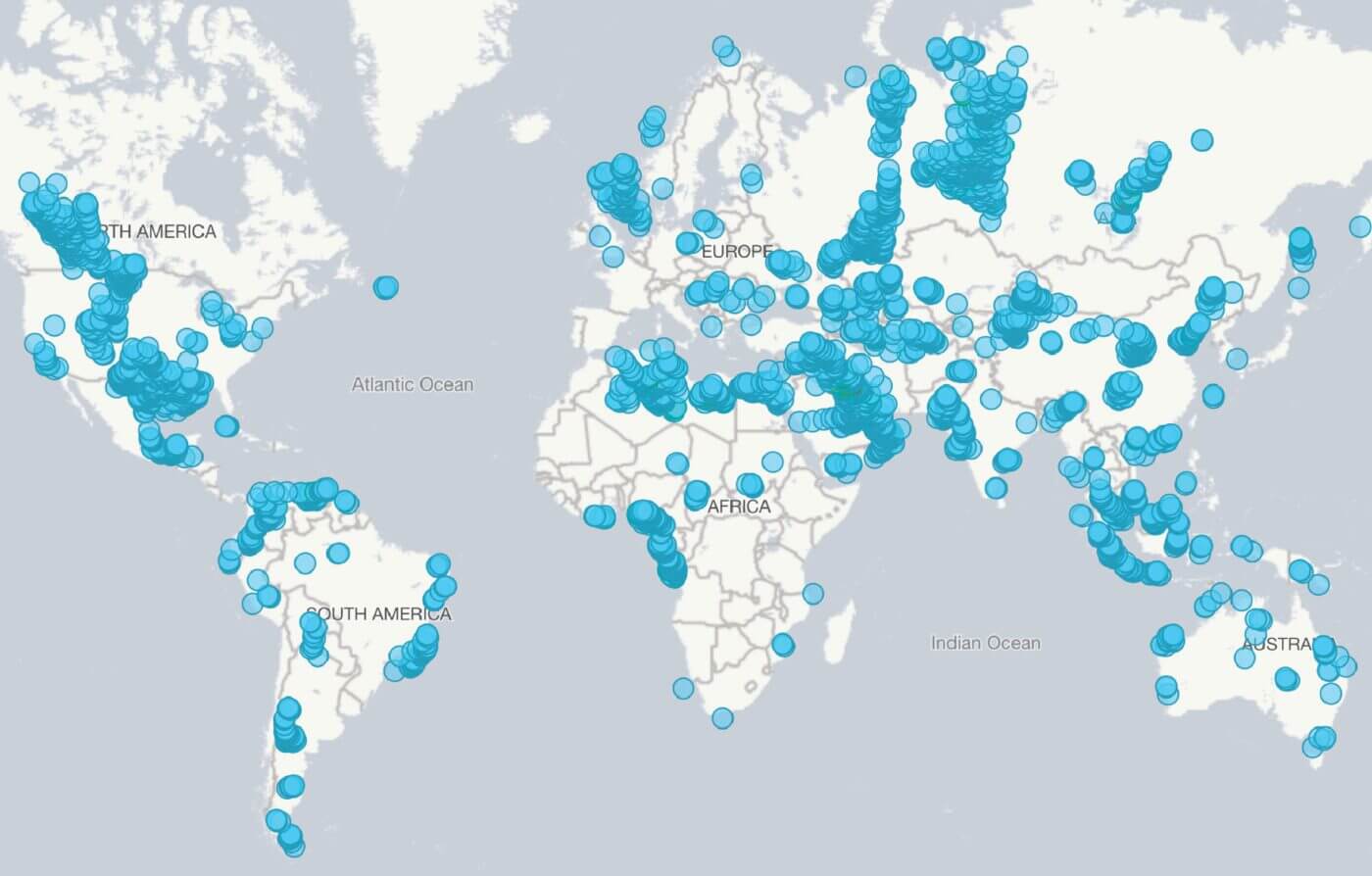

Figure 3: Locations of Flares Observed by Satellite, from World Bank Global Gas Flaring Tracker Reportxii

Flaring occurs, to some degree, at nearly all oil and gas assets, but a limited number of countries and companies are responsible for a large portion of the problem (see Figure 3).

Note about Russia and Iran: Nearly 20% of global flaring occurs in Russia and 14% occurs in Iran. Given current political dynamics and limited partnerships between IOCs and companies in Russia and Iran, this report does not focus on flaring in these countries. Flares in Iran are included in the satellite analysis— nearly all oil and gas production and flaring in the country is controlled by the national oil company. See “Russia Flaring—Satellite Data excluded” section for an overview of flaring in Russia and why it is excluded from the satellite analysis.

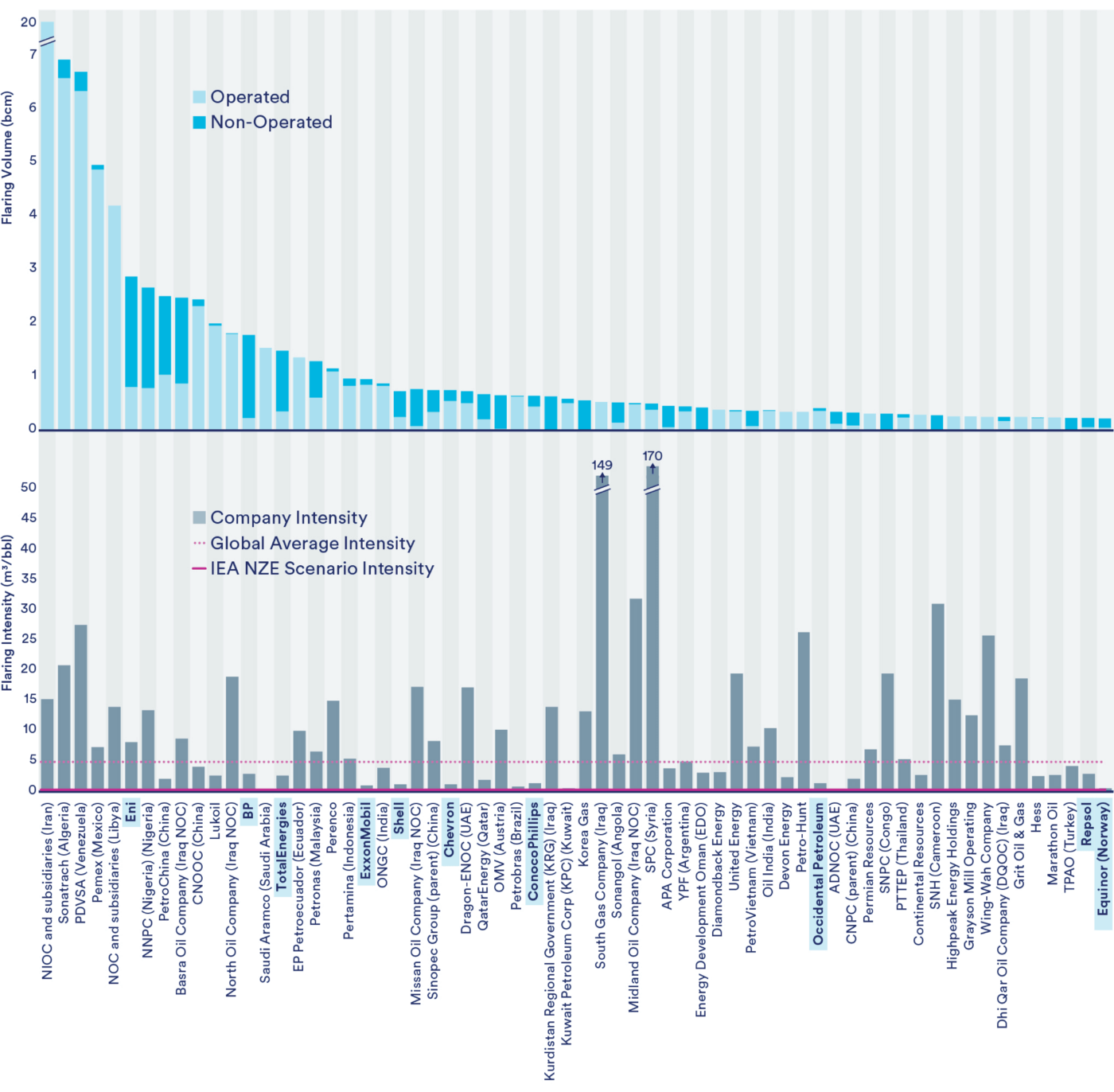

Figure 4 shows the volume of flaring (upper panel) and flaring intensity (cubic meter of gas flared per barrel of oil and condensate produced, lower panel) for the highest 64 flaring companies (excluding Russia). The data in these charts accounts for flaring from assets that the companies operate and assets that they do not operate, but in which they hold a stake, on an equity-weighted basis. All oil and gas companies bear responsibility for flaring at assets from which they are profiting, even if they are not the operator. The bottom panel also shows, as horizontal lines, the global flaring intensity average and the flaring goal aligned with the International Energy Agency’s Net Zero Emissions scenario (see Box 1).

Figure 4: Flaring Volume and Intensity for Top 64 Flaring Companies3

Box 1: Net Zero Emissions by 2050 Scenario

The International Energy Agency (IEA) has defined a Net Zero Emissions by 2050 (NZE) Scenario, which shows a pathway for the global energy sector to achieve net zero CO2 emissions by 2050.xiii One component of this scenario is a 95% reduction in all flaring by 2030.xiv The IEA’s Oil 2024 report forecasts that oil production will remain relatively constant over the next eight years.xv As a result, the flaring intensity will need to decrease by 95%, mirroring the necessary reduction in flare volume. Therefore, in this report, we use 0.3 m3/bbl, a 95% reduction from 5 m3/bbl, as a 2030 target for flaring intensity consistent with net-zero goals.

Of the 64 highest flaring companies, 28 are national oil companies (NOCs). Many other high flaring companies are not officially classified as NOCs, because part of the company is publicly traded on a stock exchange (e.g., PetroChina, CNOOC, Petrobras, Lukoil), but they are largely state-owned and controlled.

However, international oil companies (IOCs) also have substantial flaring footprints. Figure 5 shows flaring intensity (height of bars) and volumes (area of bars) for the 100 highest flaring companies, including both operated and non-operated assets on an equity-weighted basis. In this report, we focus on the 10 IOCs highlighted in orange: BP, Chevron, ConocoPhillips, Eni, Equinor5, ExxonMobil, Occidental Petroleum, Repsol, Shell, and TotalEnergies. Among companies that are neither state-owned nor state-controlled, these large IOCs flare the largest amounts of gas and have some of the highest flaring intensities.

These 10 IOCs are responsible for 7% of global flaring, on an equity-weighted basis, including both operated and non-operated assets. This is an enormous amount of flaring—about 10 bcm of gas in 2023, which is enough gas to supply Norway and Austria combined. Using the World Bank’s estimate of climate pollution from flaring, we estimate that this flaring leads to 27 million tons CO2e—about as much climate pollution as 72 natural gas-fired power plants.xvi

But the influence of these 10 IOCs extends far beyond their equity footprint. These IOCs are critical financers and innovators, and they are highly influential in the industry. Their leadership, if exercised, could materially influence the industry to aggressively reduce flaring. As we will show below, they have direct influence on 15% of total global flaring, when accounting for the full volume of flaring that occurs at assets in which they have an ownership stake. They have further influence on an additional 25% of flaring—for a total of up to 40% of global flaring – when considering all flaring occurring at their operations and at the companies they partner with.

These 10 IOCs are critical global actors because they have made commitments to end routine flaring throughout their operations (see Box 2), they have substantial ability to influence flaring management through their joint ventures and partnerships around the world, and they have the technical skills and financial resources to assist more resource-constrained companies in low- and middle-income countries with whom they partner. Despite the challenges, these companies are uniquely positioned to influence joint venture partners worldwide by pressing for flare reduction technologies and best practices. Following the lead of the Oil and Gas Methane Partnership (OGMP) 2.0, which requires companies to report on methane emissions from non-operated joint ventures in order to maintain Gold Standard designation, companies should extend flare reduction targets to their entire operations, including joint venture assets.

Figure 5: Production vs Flaring Intensity for top flaring companies worldwide (excluding Russia)3

The horizontal width of each bar represents the total crude oil and condensate production for each company, while the height of each bar represents the average flaring intensity of the company. Thus, the area of the box represents the total flaring volume.

Box 2: Routine vs. Non-Routine Flaring

The World Bank defines routine flaring as “flaring during normal oil production operations in the absence of sufficient facilities or amenable geology to re-inject the produced gas, utilize it on-site, or dispatch it to a market.”xvii It defines safety flaring as flaring of gas to ensure safe operations of the facility, while it uses the term non-routine flaring for all flaring other than routine and safety. The relative proportion of routine and non-routine flaring varies significantly across companies, suggesting differing company practices and/or diverging definitions of routine and non-routine flaring. For example, some companies consider scheduled maintenance of midstream operations as outside of “normal operations” and therefore categorize this type of (sometimes long-term) flaring as “non-routine”—while other companies may account for this flaring as “routine”. Regardless of the definitions, routine flaring is the largest type of flaring (volumetrically), as companies flared off large amounts of “stranded” associated gas from wells drilled for oil with no gas infrastructure, or insufficient gas infrastructure, in place. To date, most voluntary flare reduction commitments have focused on routine flaring. Nevertheless, in order to meet climate targets, the level of ambition must be raised to include the virtual elimination of all flaring at oil and gas sites around the world—both routine and non-routine—that is not legitimately emergency-related. Phasing out “routine flaring” is essential, but it falls far short of what’s needed.

Box 3: Attribution of Flaring Emissions in Iraq

In Iraq, BP and Eni are engaged in oil and gas production through Technical Service Contracts. As such, the contractor is responsible for the improved production and enhanced recovery of petroleum. According to the companies’ past public statements, they do not have the right to commercialize gas production at these assets, and all decisions about the commercialization of gas must be taken by the national oil companies or the Government of Iraq. Through their contracts, it is CATF’s position that they are a stakeholder in the management of these assets, and therefore they have an obligation to make management decisions about production, maintenance, and emissions control of all assets under control of these contracts.

Footnotes

5. Equinor is a majority state owned company but has many international joint ventures and international operations and has therefore been included in this report.

Credits

Report Authors: Lesley Feldman, Heny Patel, and James Turitto

Contributors: Ioannis Binietoglou, David McCabe, Felicia Douglas, Brandon Locke

For questions or comments about this report, please contact: James Turitto, CATF, [email protected]

Data analysis was performed by Clean Air Task Force with the support of the Mathematics, Computer Science and Artificial Intelligence Lab (MCSAI Lab), Faculty of Public and One Health, University of Thessaly, Greece. We thank Evie Hammer for excellent research support during the project. Flaring analysis is based on the VIIRS Nightfire (VNF) nightly data produced by the Earth Observation Group, Payne Institute for Public Policy, Colorado School of Mines. Rystad Ucube dataset was used for underlying equity production and operator tagging of assets.

The cover photo is a satellite visualization of oil and gas flaring in Algeria. Contains modified Copernicus Sentinel-2 data (2023), visualized using the QuickFire script developed by Pierre Markuse.

Methodology

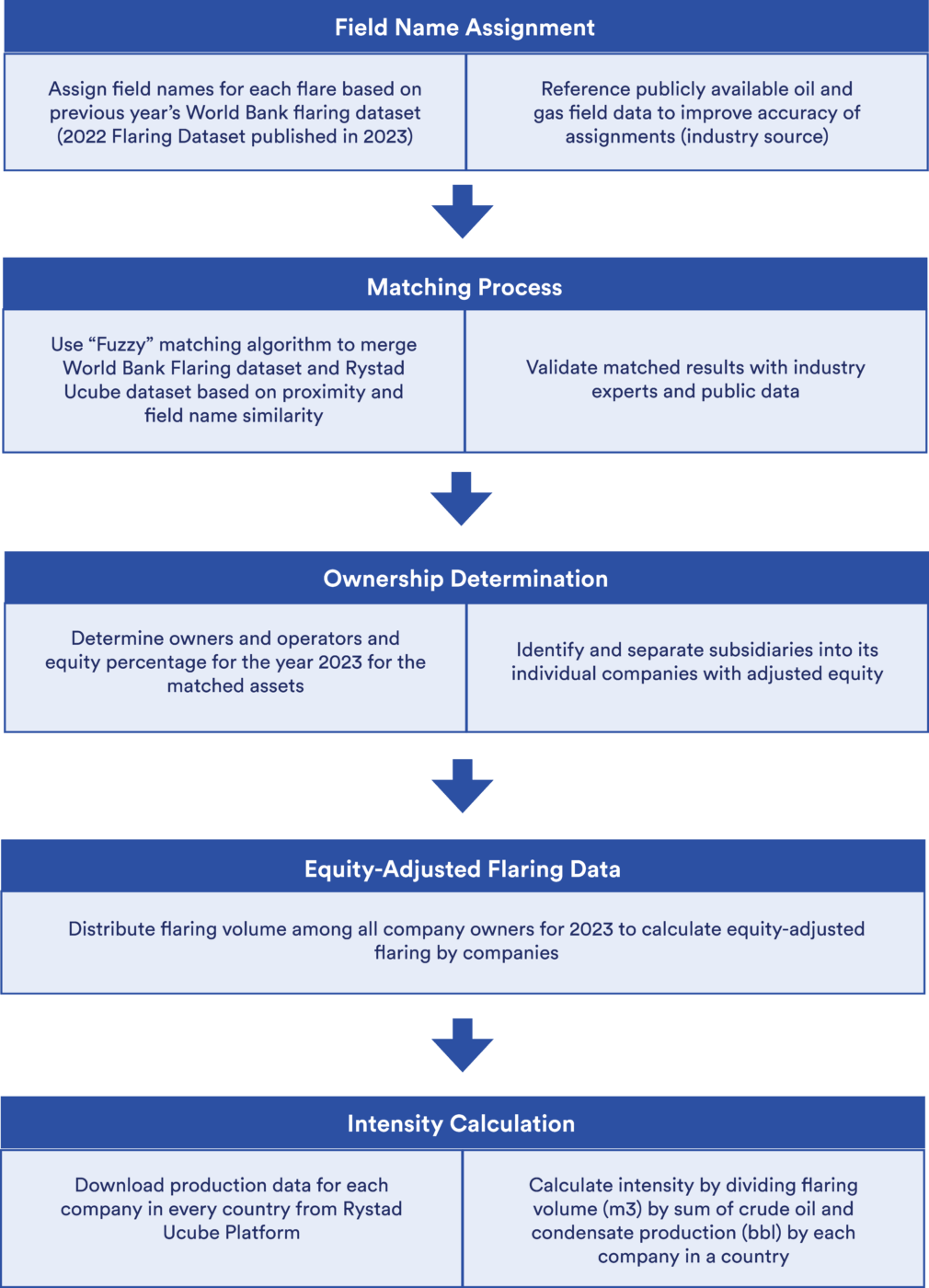

Attributing Satellite Flaring Data to Companies

This report uses the World Bank provided flaring volumes, along with flare and asset location data, to attribute flares to companies. The World Bank assumes a linear relationship and a single calibration factor to convert the radiant heat emitted by flares to gas flared volume; to the extent that the assumptions used in the World Bank’s assessment differ from local or asset level conditions, levels of flaring may vary from what is presented here.

World Bank Flaring Dataset: The World Bank Flaring Dataset, one of the primary data sources for this report, contains flare coordinates and annual flaring volume derived from the VIIRS (Visible Infrared Imaging Radiometer Suite) satellite instrument for the upstream oil and gas sector.xviii For more than a decade, these data have been processed by a team of researchers at the Colorado School of Mines to retrieve the timing, temperature, and radiative heat of flaring around the globe.xix The relationship between the volume of flared gas and the radiative heat that the satellite detects is calculated from analysis of a large number of flares with known quantity of gas being flared. The analysis uses only nightly VIIRS data, eliminating possible daytime interferences that may be a problem with data from other sensors. The frequent observations enable reliable data collection even in frequently cloudy regions. Over the years, the algorithms have been improved to remove biases due to flare shape, better identify the location of nearby flares, and separate flares from other high temperature industrial activities.xx The algorithm has been tested against ground-truth data in limited cases and against reported data in several countries.xxi The research shows that while individual detections can have uncertainties, aggregates over large number of observations and flares—as used in this study—will be robust estimates of total flaring volume.

This report analyzes the observed flares in 2023 for the entire world except for Russia and onshore United States (see sections below for more detail on our treatment of those countries).

Rystad Energy Ucube Database: The Rystad Energy (Rystad) UCube database consists of data on upstream oil and gas, including field-by-field production data, resource estimates, and ownership details, among other metrics. The UCube database also provides coordinates of all the upstream oil and gas fields and assets globally. This dataset was used to identify the field names, operators and joint ownership of each of the flares quantified by the World

Bank.xxii

Attribution Methodology: We matched each flare in the World Bank Flaring Dataset to a field in the Rystad UCube database. Thus, we were able to assign each flare to an operator as well as attribute the flare volume to all owners, based on equity stake in the asset. We took the following steps to assign operators and owners: i) match field name assigned by World Bank to Rystad asset name, ii) check geographical proximity using latitude and longitude data for the flare and asset, iii) research flare and asset characteristics using publicly available information, and iv) in cases where there were multiple similar field/asset names, multiple assets in close proximity, etc., conduct additional validation measures. The final equity-adjusted flaring data (aggregated by subnational region) was sent to the IOCs highlighted in this report for review. At the time of this publication, we have received responses from majority of the companies and have made appropriate adjustments to our dataset where documentary evidence was provided and where changes match our methodology. We also note that for nine of the 10 IOCs we focus on in this report, our assessment of the volume of flaring from operated assets is lower than the companies self-report.

Calculating Flaring Intensity: Using the asset ownership details, the total volume of flared gas was distributed to company owners which resulted in equity-adjusted flaring data for all companies. The Rystad UCube database provides equity adjusted production data which was then used to calculate a flaring intensity. The formula for flaring intensity calculation is the similar to the one used by the World Bank in the Global Gas Flaring Tracker.xxiii

The methodology was developed by Clean Air Task Force. See Appendix for more details about methodology.

Cases where Flaring Satellite Data was Not Used

U.S. Onshore Flaring – Satellite data replaced with Greenhouse Gas Reporting Program data

In 2023, oil and gas operators in the United States flared nearly 10 billion cubic meters of gas, making the U.S. the 4th highest flaring country in the world. While total flaring volume (and flaring intensity) has come down from its peak in 2019, the most recent year’s data shows an uptick – much more work remains to be done to properly address the flaring problem in the United States (see Figure 6).xxiv

The source of flaring data in the onshore United States is different than that used for the rest of the world. This is for several reasons: 1) frequent ownership changes of upstream oil and gas assets make it difficult to robustly track and attribute by using only satellite flaring data, and 2) tightly spaced upstream assets in many key flaring basins (including the Permian) make it infeasible to attribute flares to specific well pads (and therefore companies) using such satellite data. On the other hand, onshore oil and gas operators in the U.S. are required to report flaring volumes as part of the U.S. EPA Greenhouse Gas Reporting Program (GHGRP) Subpart W.6 While there is not a perfect match between the satellite observations and reported flaring data, the total volumes are roughly similar, and likely within the uncertainty bounds for each methodology.

Figure 6: Satellite observations of flaring volume and intensity in the oil and gas industry in the United States from 2012 to 2023

Figure 7 compares total flared volumes from the two methods for 2023. For each of the IOCs considered in the report, we add reported flaring volumes from the GHGRP for onshore U.S. to the satellite total from outside the U.S. to get the company’s total flaring volume and intensity.

Figure 7: Comparison of Reported and Observed Flaring in the Onshore United States

In 2023 the 10 IOCs considered in this report are responsible for 11% of the flaring in the onshore U.S., while producing 28% of the oil and condensate in the U.S.xxv Two of the IOCs (ConocoPhillips and ExxonMobil), are among the top 20 flaring companies in the U.S. The 10 IOCs highlighted in this report have relatively low flaring intensities at the onshore U.S. operations: high flaring levels at onshore U.S. operations are dominated by companies with solely U.S. footprints (see Figure 8).

Figure 8: Gas Flaring Volume and Intensity of Top 20 Flaring Companies in the United States

Russia Flaring – Satellite Data excluded

Oil and gas companies in Russia flare more gas than in any other country—and this has been consistent since 2012 when the World Bank first started collecting and publishing satellite flaring data. In 2023 flaring in Russia accounted for nearly one-fifth of flaring globally. Flaring in Russia has been increasing steadily over the past several years, both in absolute terms and in terms of intensity (flaring per barrel of oil produced) (see Figure 9).xxvi

However, despite the magnitude of the problem, geopolitical circumstances have left IOCs with very little leverage over operations in Russia. According to analysis by the Yale Chief Executive Leadership Institute (CELI), since the Russian invasion of Ukraine in 2022, many of the IOCs considered in this report have significantly reduced or withdrawn from their operations in Russia (see Table 1).xxvii While some companies continue to operate joint ventures, there is a diminishing opportunity for influence in partnerships with state-owned oil companies in Russia. As a result of these political constraints as well as practical limitations (i.e. concerns about data quality and significant recent changes in ownership of oil and gas assets in Russia), we did not conduct our ownership attribution analysis for flares in Russia.

Figure 9: Satellite observations of flaring volume and intensity in the oil and gas industry in Russia from 2012 to 2023

Table 1: Status of IOCs in Russia

| Company | Involvement in Russia prior to 2022 | CELI evaluation |

|---|---|---|

ExxonMobil | Operated Sakhalin-1 project | Withdrawal: Exit Rosneft partnership |

| Chevron | Interest in pipeline transporting oil from Russia | Suspended: Pausing all transactions and sales of refining products, lubricants, and chemicals |

| Shell | Scaled Back: Committed to total withdrawal but backtracked with LNG | |

| BP | Withdrawal: Will divest from 20% Rosneft stake | |

| TotalEnergies | Buying Time: no longer will provide capital for new projects in Russia/stop purchasing Russian oil; withdraw from Arctic LNG 2 project | |

| ConocoPhilips | None since 2015 | |

| Equinor | Withdrawal: Exit joint ventures in Russia | |

| Eni | Withdrawal: Suspend stipulation of new oil contracts; divest from investments for rubles | |

| Occidental Petroleum |

Footnotes

6. Note, companies do not report flaring directly, instead they report metric tons of CO2 emitted. We convert to volume of gas flared assuming the following gas composition: 80% methane, 10% ethane. 5% propane, 3% butanes, 1% pentanes, and 1% hexane (by volume). Reported CO2 emissions volumes for “Associated Gas Venting and Flaring” and “Other Flaring” and oil and gas production sites are included. “Other Flaring” at oil and gas production sites includes CO2 emissions from the following emissions sources: Tanks, Compressors, Completions/Workovers, Dehydrators, Flare Stacks, and Well Testing.

Credits

Report Authors: Lesley Feldman, Heny Patel, and James Turitto

Contributors: Ioannis Binietoglou, David McCabe, Felicia Douglas, Brandon Locke

For questions or comments about this report, please contact: James Turitto, CATF, [email protected]

Data analysis was performed by Clean Air Task Force with the support of the Mathematics, Computer Science and Artificial Intelligence Lab (MCSAI Lab), Faculty of Public and One Health, University of Thessaly, Greece. We thank Evie Hammer for excellent research support during the project. Flaring analysis is based on the VIIRS Nightfire (VNF) nightly data produced by the Earth Observation Group, Payne Institute for Public Policy, Colorado School of Mines. Rystad Ucube dataset was used for underlying equity production and operator tagging of assets.

The cover photo is a satellite visualization of oil and gas flaring in Algeria. Contains modified Copernicus Sentinel-2 data (2023), visualized using the QuickFire script developed by Pierre Markuse.

Global Flaring Analysis

Comparing Company Reported Data to Satellite Data

The flaring dataset that we have assembled in this report differs from company reporting in two major ways:

- Our analysis uses satellite observations of flaring matched to oil and gas operations. Company reporting on flaring volume, in contrast, is based on a variety of sources, including flare meters, engineering calculations, and other operational information.

- Most companies only report flaring volume using an operated assets attribution method,7 meaning that they account for 100% the flaring from the assets that they operate even if they don’t fully own the asset; conversely, they do not include flaring from assets they do not operate, even when they have an ownership stake. Instead, the main analysis in this report attributes flaring to companies based on an equity ownership attribution method which attributes flaring to companies based on their percent ownership stake in the flaring asset, regardless of whether they operate the asset.

Before diving into the detailed findings of our satellite-based equity ownership flare attribution, it is useful to first assess the impact of these two major differences in approach. First, we compare company reporting to satellite observed data attributed to companies, using the same operated assets attribution method that companies typically use for self-reported flaring to calculate company volumes from the satellite data. Second, we compare the satellite flaring data assessed using the operated asset method to satellite data assessments using the equity ownership method.8

Figure 10 shows the difference between the flaring data reported by the companies and the satellite-derived flaring data, using the same operated assets attribution method. Significant discrepancies exist for some companies between company-reported data and the satellite data. Satellites can detect flaring that may be unreported by companies for various reasons. However, in 9 of the 10 cases, company-reported flaring from operated assets exceeds satellite flaring observations. There are several potential explanations for this, including:

- Satellites can only measure flares at nighttime, which might introduce bias as operations during the night may be different from during the day (e.g. maintenance activities that might result in flaring are typically conducted during daylight hours).

- Satellites have challenges assessing flaring in countries with high amounts of cloud cover and have other errors/uncertainties, which the World Bank may not be fully able to account for.

- If flaring combustion efficiency (a difficult quantity to measure) is lower than that assumed in the World Bank’s flare analysis, the satellite data will underestimate actual flaring volumes.

- Our analysis of satellite data excludes flaring in Russia (see “Russia Flaring—Satellite Data excluded” section for an overview of flaring in Russia and why it is excluded), so to the extent that these companies operated assets in Russia in 2023, the satellite data underestimates total flaring.

- Satellites can detect large flares (larger than approximately a 7,000 standard cubic meters/day); they do not fully account for smaller flares, which can be persistent and in the aggregate account for large volumes of flaring.

- Companies may include in their reported flaring volumes non-hydrocarbon gases (CO2, N2, H2O) which are not burnable and thus won’t be accounted for in satellite observations.

- Satellites observe flares intermittently and extrapolate to estimate annual flaring volumes, and thus they may be biased upwards or downwards depending on when flare observations are made.

Figure 10: Comparison of Reported and Observed Flaring Based on Operated Assets Attribution3

Figure 11 shows the comparison of satellite flaring data for each of the 10 companies using the two different attribution methods: operated assets vs equity ownership. Even though most companies report flaring volume only for their operated assets, this is not the only way, or necessarily the best way, to attribute flaring volume. In the equity ownership attribution method, we can distinguish between flaring that occurs at assets operated by the company vs. flaring at non-operated assets. This method illuminates the significant flaring problem that exists at non-operated assets for many companies. Table 2 highlights the pro and cons of each attribution method.

Figure 11: Comparison of Satellite Data with Operated Asset and Equity Ownership Attribution3

Table 2: Pros and Cons of different Attribution Methods

| Method | Pros | Cons |

|---|---|---|

| Operated Assets Attribution | Industry standard: Companies are used to reporting flaring and other environmental metrics at the operated asset. Measure what you can directly control: Companies have direct control over operated assets. | Not inclusive: Does not include non-operated assets from which the company profits and can influence. Not aligned with company financial reporting that account for ownership in various operated and non-operated assets. |

| Equity Ownership Attribution | Allows calculation of intensity: Production data based on an equity adjusted method is available, so flaring can also be adjusted with equity ownership to calculate flaring intensity. Aligns to revenue and profit: It accounts for a company’s “stake” in flaring around the world, making it clear that they bear responsibility for flaring at assets that they are profiting from, even if they are not the operator. | Diffuses the accountability link: Multiple owners for same flare, so not a single company to hold accountable. |

Comparing the 10 IOCs

International oil companies have a significant global presence in oil and gas production. This report highlights 10 of the largest IOCs, namely: BP, Chevron, ConocoPhillips, Eni, Equinor, ExxonMobil, Occidental Petroleum, Repsol, Shell, and TotalEnergies. These companies have historically avoided taking the responsibility for emissions and practices, including flaring, at their non-operated assets. All 10 companies are members of OGMP 2.0, and have therefore committed to reducing emissions and flaring at their non-operated joint ventures. With operations in over 50 countries and partnerships with numerous NOCs and other public and private firms, these companies have much greater influence to set standards and drive essential changes to reduce flaring (refer to Broader Impact of International Oil Companies section below for more detailed discussion). All data and figures in this section are calculated on an equity-weighted basis.

Production: The 10 IOCs highlighted in this report produced an equity-weighted total of 4,818 million barrels of oil and condensate in 2023, approximately 16% of total global production in that year.xxviii Each of these companies has a global footprint, with production occurring at both operated and non-operated assets, although the equity-weighted split between these different types of assets ranges from 31% of production from operated assets for Repsol, to 93% from operated assets for Occidental. On average, 51% of the crude oil and condensate production for these 10 companies is from non-operated assets.

Figure 12a: Oil and Condensate Production for IOCs3

Flaring Volume: Total flaring attributable to the 10 companies analyzed was 10 bcm in 2023, which was 7% of global flaring in that year. The specifics of flaring differ for each company: ExxonMobil, Chevron, ConocoPhillips, Eni, and Occidental have the majority of equity-weighted flaring at their operated assets; conversely, BP, Shell, TotalEnergies, Equinor and Repsol have the majority of flaring at their non-operated assets. As shown in the company summaries, this trend also looks different for individual companies comparing across countries. For these 10 companies, 61% of flaring takes place at non-operated assets.

Figure 12b: Flaring Volume for IOCs3

Flaring Intensity: Seven companies (BP, Shell, TotalEnergies, ConocoPhillips, Equinor, Occidental and Repsol) have higher flare intensity at their non-operated assets, while ExxonMobil, Chevron, and Eni have higher flare intensity at their operated assets. While 9 of the 10 have flaring intensities lower than the global average, all have intensities that are much higher (by at least a factor of two, in many cases much more) than the target level for 2030 from the IEA NZE scenario.

Figure 12c: Flaring Intensity for IOCs3

Figure 12d: Top IOC Flaring Intensity vs. Crude Oil and Condensate Production3

Footnotes

7. One company, Chevron, reported flaring separately using both methods. Other companies do not explicitly state which method is used. We assume the Operated Asset Attribution method in all other cases.

8. Each satellite observed flare is matched with an oil and gas asset, and thus it is possible to attribute flares to companies using either method.

Credits

Report Authors: Lesley Feldman, Heny Patel, and James Turitto

Contributors: Ioannis Binietoglou, David McCabe, Felicia Douglas, Brandon Locke

For questions or comments about this report, please contact: James Turitto, CATF, [email protected]

Data analysis was performed by Clean Air Task Force with the support of the Mathematics, Computer Science and Artificial Intelligence Lab (MCSAI Lab), Faculty of Public and One Health, University of Thessaly, Greece. We thank Evie Hammer for excellent research support during the project. Flaring analysis is based on the VIIRS Nightfire (VNF) nightly data produced by the Earth Observation Group, Payne Institute for Public Policy, Colorado School of Mines. Rystad Ucube dataset was used for underlying equity production and operator tagging of assets.

The cover photo is a satellite visualization of oil and gas flaring in Algeria. Contains modified Copernicus Sentinel-2 data (2023), visualized using the QuickFire script developed by Pierre Markuse.

Broader Impact of International Oil Companies

Three Approaches to Flaring Attribution: Equity Portion, Ownership Influence, and the Partner Multiplier Effect

Thus far, we have focused on the flaring that can be attributed to each of the 10 IOCs at both their operated and non-operated assets based on equity weighted flaring at each asset. While this has a clear accounting logic, it underestimates the total amount of flaring that these companies can influence. This broader influence stems from their partnerships and the global reach of their operations.

We identify three levels of influence that IOCs have on global flaring: Equity Portion, Ownership Influence, and the Partner Multiplier Effect. For each successive level, the flaring volume increases (see Figure 13), but the influence becomes less direct. Together, these figures give a fuller picture of the role that IOCs can play in reducing flaring worldwide. While the relationships between these companies, the companies with which they partner, and the countries in which they operate are complex, IOCs must exert leverage to reduce flaring beyond their direct operations.

Equity Portion: This includes flaring at both operated and non-operated assets and apportions flare volume to each company based on percent ownership in the flaring asset. The portion of global flaring attributed to the 10 IOCs under this method is 7%.

Ownership Influence: This accounts for the entire volume of flaring at assets where the 10 IOCs are involved and does not discount flaring volume by ownership percentage. As part owners, the IOCs have influence on all flaring from these assets, which amounts to 15% of all global flaring.

Partner Multiplier Effect: The 10 IOCs, and the companies that they partner with, account for about 40% of all flaring worldwide. Because of these partnerships, the 10 IOCs have financial and operational relationships with NOCs and other firms that are responsible for vast amounts of flaring. The IOCs must use these relationships to share flare reduction best practices and influence their partners to collectively advance projects and practices to reduce flaring. Utilizing this Partner Multiplier Effect can greatly reduce flaring.

Figure 13: Three Approaches to IOC Flaring Attribution3

The IOCs highlighted in this report have a unique opportunity to influence and support their partners in reducing flaring across their operated and non-operated assets. Figure 14 depicts the volume of flaring for each company using the Equity Portion and Ownership Influence attribution methodologies. The size of difference between attribution methodologies depends on the ownership structure of each company’s assets. At the high end, for TotalEnergies and Repsol, the volume of flaring using the Ownership Influence methodology is five times higher than flaring based on Equity Portion, due to significant investments with partners flaring very large amounts of gas.

Figure 14: IOC Equity Portion vs. Ownership Influence3

Bringing National Oil Companies to the Table

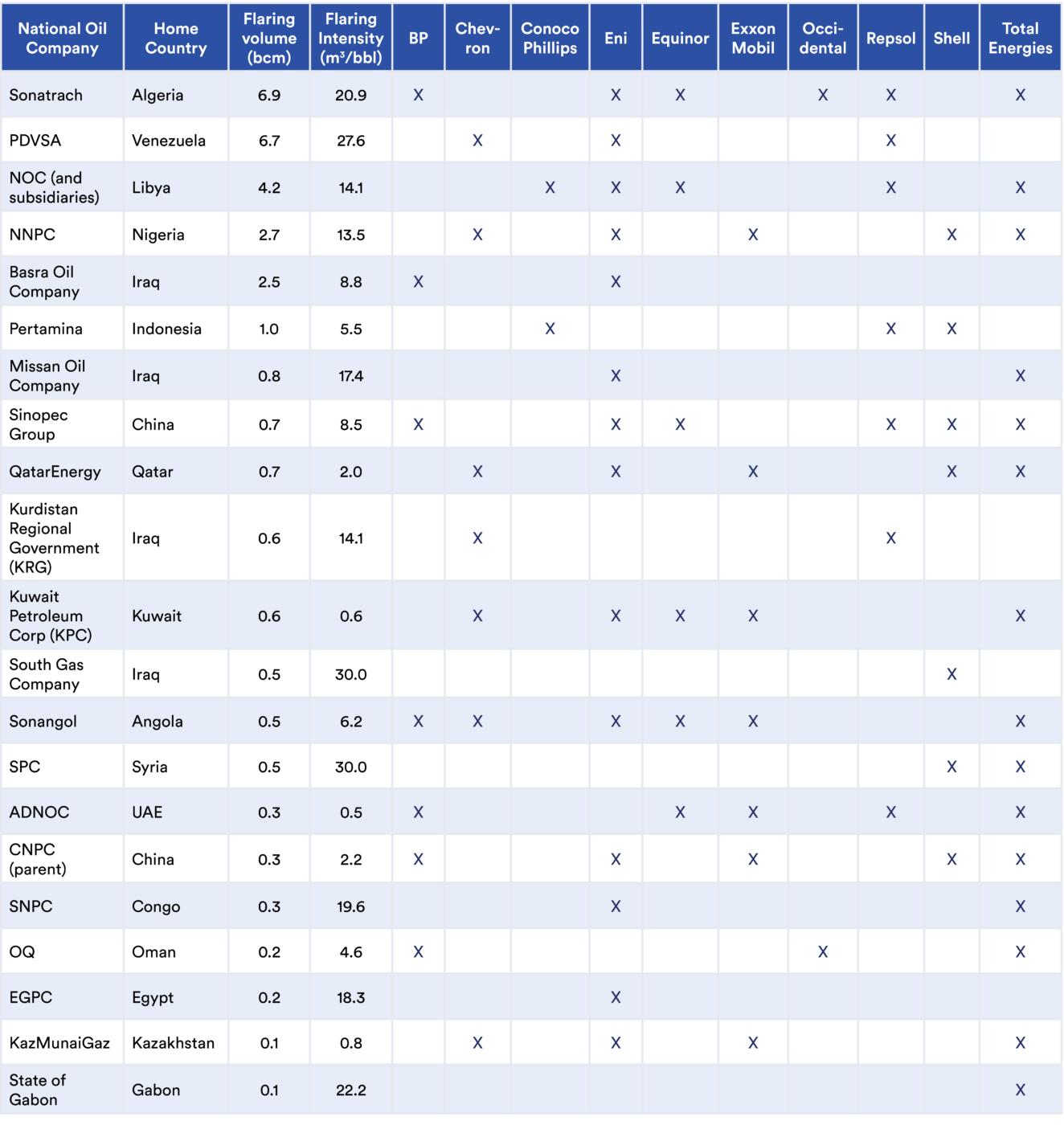

NOCs are responsible for at least half of global flaring, and many NOCs have important relationships with one or more of the 10 IOCs—thus the Partner Multiplier Effect is significant. These relationships are documented in Table 3, which looks at the 37 NOCs that are among the top 100 flaring companies. For each, it marks whether that NOC has joint ownership of flaring assets with any of the 10 IOCs. Half of the NOCs have some relationship with at least one of the 10 IOCs, and in many cases they have multiple partnerships. Many IOCs have started engaging their NOC and other equity partners through voluntary initiatives such as the Oil and Gas Methane Partnership (OGMP 2.0) and Methane Guiding Principles to advance methane emissions reductions and improve data measurement and reporting.xxix

These efforts must be adopted by more companies and expanded quickly at a global scale to drive the necessary reductions in flaring. In addition, investments in technologies that eliminate flaring should not be considered one asset at a time—gas utilization depends on pipelines, compression, or other gas capture and use projects that can serve an entire region/basin, and therefore IOCs should be thinking about flaring more broadly and not only about the assets they operate or own.

Table 3: Relationships between IOCs and Top NOCs in Top 100 by Flaring Volume (not including flaring in Russia)

Table 4 looks at the 20 highest flaring countries, and notes how much of the flaring in each is attributable to the 10 IOCs on an equity basis, and how much of the flaring could be influenced by IOCs (Ownership influence). (The Equity Portion figures in this table match the figures presented in the bulk of this report, while the Ownership Influence figures, as noted above, count the entire flare volume for which one or more IOC is involved.) Countries such as Angola, Nigeria, Congo, and Oman, where the IOCs are responsible for a large fraction of the equity portion and/or ownership influence, should hold the participating IOCs accountable in reducing flaring.

Table 4: IOC Involvement in Top 20 Flaring Countries – Percent of Flaring attributed to each IOC in top 20 Flaring Countries3

Moving From Targets to Action

Recognizing the significant impacts of flaring, international organizations have initiated efforts to reduce routine gas flaring. The most important effort to date is the World Bank’s Zero Routine Flaring by 2030 (ZRF), a voluntary initiative that aims to eliminate “routine” gas flaring through cooperation with governments, oil and gas companies, and development institutions. Such global efforts underscore the collective recognition of the need to urgently address flaring.xxx However, despite commitments by over 100 companies, governments, and organizations, global gas flaring has largely remained at the same level for more than a decade.

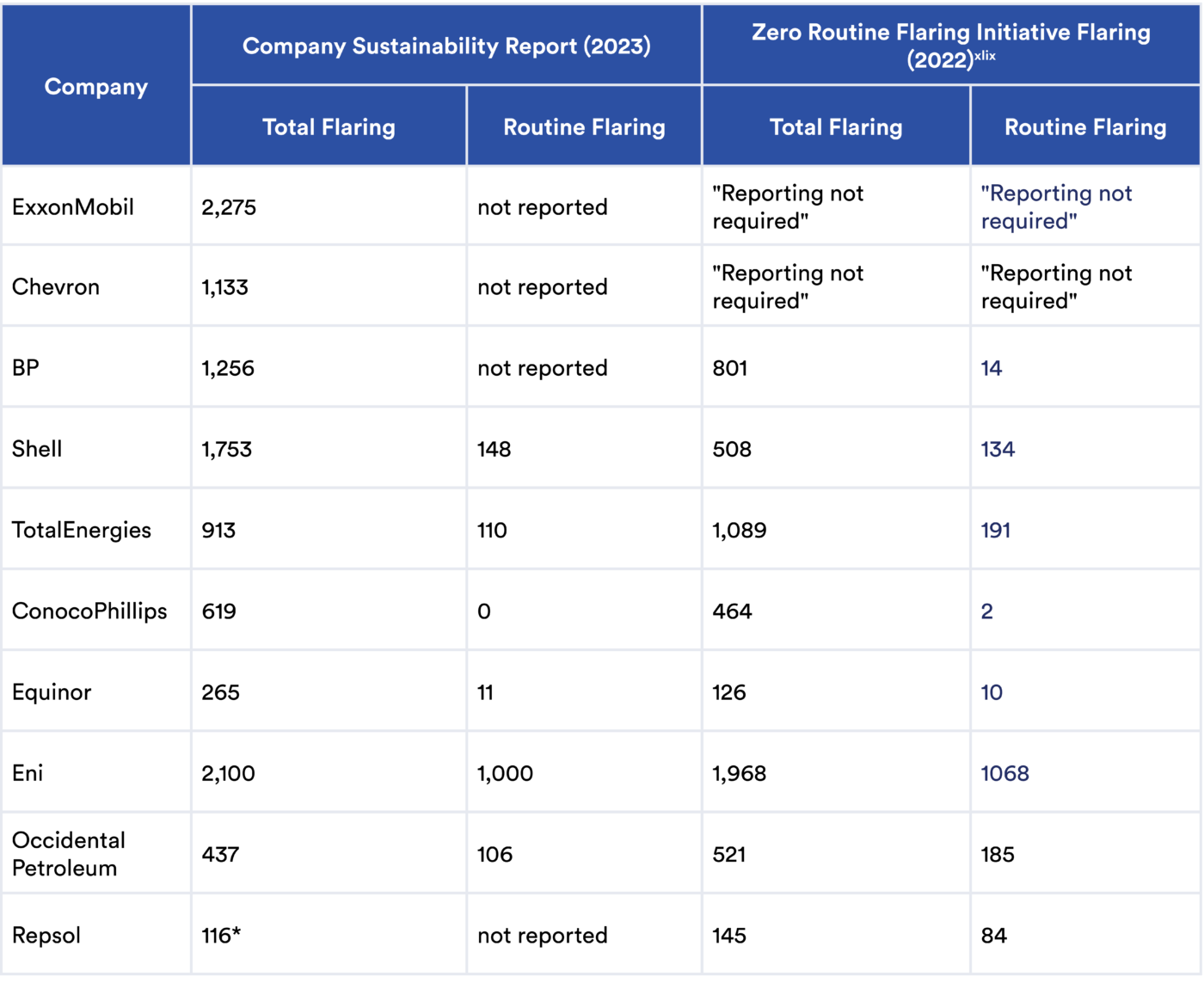

All 10 IOCs highlighted in this report have endorsed the ZRF initiative and are required to report total flaring and routine flaring volumes for operated assets each year. Table 5 summarizes the self-reported progress by each company in meeting their zero routine flaring goals.

It is important to note the general focus in these commitments on routine flaring. The World Bank defines routine flaring as “flaring during normal oil production operations in the absence of sufficient facilities or amenable geology to re-inject the produced gas, utilize it on-site, or dispatch it to a market.”xli As we explore below, for many of the IOCs, only a small portion of reported flaring is classified as routine, raising questions about what activities are leading to such sizable volumes of non-routine flaring, whether companies are using uniform definitions for routine vs. non-routing flaring, and how non-routine flaring will be addressed.

Table 5: The Gap Between ZRF Endorsement and Real-World Flaring Practices

| Year of ZRF Endorsement | Total Routine Flaring (mcm)* | Company Reported Progress on Zero Routine Flaring Commitments | |

|---|---|---|---|

| ExxonMobil | 2022 | – – | Eliminated routine flaring in Permian Basin operated assets in 2022.xxi |

| Chevron | 2021 | – – | Efforts to reduce flaring in the Permian through the use of real-time autonomous optimizers.xxxii |

| BP | 2015 | 14 | Increased flaring in 2023 in Azerbaijan-Georgia-Türkiye region but still on track to end routine flaring by 2030.xxxiii |

| Shell | 2015 | 134 | In 2021 moved target for eliminating routine flaring from 2030 to 2025.xxxiv |

| TotalEnergies | 2015 | 191 | In 2023 ended routine flaring in the Nigeria OML100 offshore block, which had represented 57% of the company’s exploration and production (E&P) flaring in 2020.xxxv |

| ConocoPhillips | 2020 | 2 | Set goal of ending routine flaring by 2025. In 2022 routine flaring decreased 90% from 2021.xxxvi |

| Equinor | 2015 | 10 | Goal to end routine flaring by 2030 for all assets in operational control.xxxvii |

| Eni | 2015 | 1,068 | Goal of zero routine flaring in 2025, subject to project execution in Libya.xxxviii |

| Occidental Petroleum | 2020 | 185 | Reduced routine flaring by 44% in global oil and gas operated assets since joining ZRF from 2020 through 2022, including Zero Routine Flaring in U.S. operations in 2022.xxxix |

| Repsol | 2016 | 83 | Aim to reduce routine flaring emissions 50% by 2025.xl |

Figure 15 shows the flaring volumes that each company has reported to the ZRF since 2018, broken out by routine and non-routine flaring. Some key takeaways from the reported data include:

- The amount of flaring that is routine varies widely across companies, suggesting either different operational characteristics or different definitions/judgments of what constitutes “routine flaring”. For example, both Eni and BP reported similar total flaring volumes at the beginning of the time series, but of that total, BP reported that only a small amount was routine, while for Eni the majority was classified as routine.

- Eni has reduced its volume of routine flaring over the time series, but overall flaring volume has stayed relatively constant—non-routine flaring has increased considerably.

- Shell and TotalEnergies have reduced both routine and total flaring volumes, but remaining volumes are still very substantial.

- ConocoPhillips, BP, and Equinor reported that they have virtually eliminated routine flaring, but their volumes of non-routine flaring are still significant.

- Repsol has relatively low flaring volume, but a large portion of that flaring is classified as routine.

- Although there is an overall downward trend in routine flaring, the total volume of flared gas—taking into consideration non-routine flaring events—remains high and largely unabated.

Figure 15: Five years of Reported Flaring, routine and non-routine (World Bank Zero Routine Flaring Initiative)

Based on the flaring volumes reported by IOCs to the ZRF Initiative, only 30% of flaring in 2022 was routine. Thus, even if the companies meet the ZRF by 2030 target, the remaining non-routine flaring will still be a very large source of pollution and flaring will be many times higher than the 95% reduction required to meet the IEA NZE reduction target. The level of ambition must be raised to include the virtual elimination of all flaring at oil and gas sites around the world that is not legitimately emergency-related.

Additionally, there are also several shortcomings in flare reporting to the ZRF, as well as voluntary reporting in sustainability reports:

- The distinction made by the ZRF between routine and non-routine flaring is useful, but it is necessarily vague, and it is not clear that all companies are interpreting it in the same way.

- Reported volumes typically only account for flaring at a company’s operated assets. It does not account for flaring at assets in which the company may have an ownership stake but is not the operator.

- Reporting likely does not account for situations where an operating company is created for the purposes of operating an asset that is wholly owned by other companies. For example, in 2022 Azule Energy was created as a 50/50 joint venture between BP and Eni to operate assets in Angola.xlii Thus, assets operated by Azule Energy may not be considered “operated assets” of either BP or Eni in the corporate sustainability or ZRF reporting.

- Companies report flaring volume at a corporate level, not broken out by country or producing basin, which limits the utility of the dataset.

Operational and Technical Solutions

Despite voluntary efforts by the World Bank and other institutions to curtail the practice of flaring in the oil and gas industry, and the higher visibility of flaring as satellites, drones, and other remote sensing technologies become ubiquitous, the problem continues to be a major contributor to climate change and threatens the health of millions of people. Flaring is an issue that can largely be solved with existing technology—where flaring does persist it is because of a combination of factors including ingrained company practices, a lack of proper planning, a shortage of capital, and a lack of political will.

While companies can secure financial, environmental, and health benefits from reducing flaring, delivering the technical solutions to capitalize on these opportunities requires broad internal engagement and buy-in, including from facility managers, operational managers, and top management. Securing this engagement starts with improving internal data on flaring for both operated and non-operated assets, as patchy data conceals potential economic returns and undermines confidence in investment decisions. (One way that IOCs can help improve data on non-operated assets is by encouraging their joint venture partners to join OGMP 2.0.) In addition to improving the quality and visibility of flaring data, companies must ensure every management level is empowered with the capacity and incentive to drive a potential flaring reduction project forward. This requires a shift in company culture where flaring objectives are placed on par with other safety or production targets and included in key performance indicators and bonus frameworks.

Technological solutions to reduce flaring broadly require investments in gas capture capacity and other gas utilization infrastructure, permitting gas to be used onsite for local operations, brought to market, reinjected, or used to produce other petroleum products. For new assets, planning is key and, to the maximum extent possible, gas utilization infrastructure should be put in place from the beginning of an asset’s productive life to ensure that flaring does not occur when production first starts if gas-handling infrastructure is not yet built.

The technology solutions to reduce flaring are clear and can include:

- Pipelines to bring associated gas to markets;

- Compressed Natural Gas (CNG) trucking to act as a “virtual pipeline” to bring gas to markets;

- On-site electricity production, either for local use or to feed into the electricity grid;

- Gas-to-liquids facilities;

- Natural gas liquids recovery to remove higher hydrocarbons; and

- Reinjection into underground reservoirs (where applicable).

Flare capture solutions have been documented at facilities around the world and are often profitable for companies implementing them.xliii The World Bank has developed a “Flare Mitigation Technology Selection Tool” and comprehensive flare management guidance.xliv While existing efforts to capture and utilize gas that would otherwise be flared are commendable, the pace of these projects must be sped up drastically in order to match the size of the problem on a global scale.

Eliminating routine flaring often requires major infrastructure to capture and utilize the gas. Non-routine flaring is associated with things like maintenance, plant trips, upsets, and is managed through operational efficiency and a strong management philosophy to conserve gas to be produced rather than flared. Thus, minimization of non-routine flaring often requires zero capital expenditure but does entail operational costs and a cultural shift in operational philosophy.

Leveraging Company Leadership

This analysis attributing global flaring to equity owners makes clear that some of the world’s largest IOCs are profiting from their investments in operations with high volumes and intensities of flaring, and they must be held accountable to address this problem. Despite commitments from all 10 IOCs in this report to eliminate routine flaring, the data show that further steps are needed to extend these pledges to non-routine flaring and comprehensively address flaring across non-operated assets. While the level of direct influence that IOCs have on non-operated assets may vary depending on contractual joint venture agreements, IOCs have several options to guarantee reductions in flaring wherever they hold ownership stakes.

Moreover, building alignment with other joint venture partners around flaring reduction goals is often an essential prerequisite to advancing flare-gas capture projects. Due to potential contractual hurdles related to gas-ownership and sale, and the use of infrastructure and pipelines, alignment between joint venture partners around flare-reduction objectives is critical for practical implementation of many technological solutions.

To achieve this alignment between joint venture partners, and fully leverage the influence of IOCs to reduce flaring at non-operated assets, the following tools and objectives should be considered:

- Flare reduction goals and actions must extend beyond operated assets to all assets in which the company has a stake: This can be established unilaterally as a company policy and would entail the consideration of flaring from all non-operated assets in the calculation of any company targets. Institutions and initiatives such as the World Bank should support this goal through updates of goals and targets to include non-operated assets, following the lead of OGMP 2.0.

- Fully leverage joint venture governance tools: Companies should use their position on the governance committees of joint ventures to pursue flaring reductions in non-operated assets, for example by building consensus for a written charter, or by leveraging approval rights on major budgetary decisions. Companies can also encourage flaring objectives through joint venture board resolutions, and by including contractual obligations to manage methane in new operating agreements.xlv

- Company commitments to reduce flaring must include total flaring rather than only routine flaring: There must be a stricter definition of what is considered “routine” flaring and follow through on commitments to eliminate this practice. And there must be stronger commitments to drastically reduce total flare volume. Again, institutions and initiatives seeking to reduce harm from flaring should support these goals.

- Proactively share technology and best practices: Given the powerful leverage these companies have in many of the countries in which they operate, it is also critical that IOCs share flare reduction technologies and best practices with partner companies (often NOCs), to ensure that flaring is minimized across the industry.

Regulatory Levers

Firm regulations are indispensable for reducing flaring, and several countries and subnational governments have already enacted measures to this end. Norway implemented the first ban on routine flaring as early as 1972, and subsequently demonstrated that strict emissions regulations are not mutually exclusive with industry competitiveness.xlvi Subsequently, several jurisdictions in the United States and Canada, as well as Nigeria, Mexico, Qatar, Brazil, the European Union and others have made regulatory efforts to reduce flaring. Well-designed and enforced regulations can play a critical role in directly reducing flaring and creating an enabling environment for flare reduction, and governments should consider the following tools:

- Set penalties on flaring to reduce the net cost of flare reduction: Regulators should set penalties for all flaring, or for exceeding flare volume or intensity limits, creating an immediate financial incentive to reduce flaring. Financial penalties can effectively reduce the net cost of flare reduction, but they must be consistently applied to be considered in a cost-benefit analysis of a potential project.

- Requiring gas-capture plans for new operations: For new operations, careful planning can eliminate the risk of routine flaring in the future. Regulators should make these plans’ development a prerequisite for any license for new operations.

- Defining and prohibiting routine flaring, and precisely defining exceptions for allowed, non-routine flaring: Regulations can play an important role by defining what flaring events qualify as ‘routine,’ and delineating what exceptions should qualify as ‘emergency’ or ‘non-routine’ flaring. As previously noted, the percentage of total flaring that companies report as ‘routine’ varies significantly across the industry, suggesting use of diverging definitions for what qualifies as ‘routine.’ These definitions are critical in the context of the commitments that the 10 IOCs in this report made to eliminate routine flaring, as collectively they report 30% of their flaring as routine, potentially leaving 70% of flaring unabated. The World Bank’s definitions for routine, non-routine, and safety flaring are useful, however the latter two categories permit broad interpretation to re-classify events that should be considered routine flaring.

In the absence of industry alignment, governments and regulators must play a role setting guard-rails for how companies define these terms. This can be done by setting a general prohibition on flaring, except for in emergency or malfunction situations that are clearly delineated. The European Union’s new Methane Regulation, for example, takes this approach and lists 11 specific situations when flaring is permissible, if necessary, with an additional condition that flaring is only allowed when re-injection, storage for later use, utilization on-site, or putting the methane on the market is not feasible for reasons other than economic considerations. In other jurisdictions, the narrow exemptions to a broad flaring prohibition are backed up by volumetric or intensity limits standards that limit the amount of flaring that can occur, even from these specific, excepted processes.

Finally, it is important to consider that regulations that appear strong on paper may be quite weak in practice, due to lack of enforcement capacity within the regulatory agency, conflicting priorities within the regulatory agency (i.e. when the same agency is charged with increasing production and enforcing flaring limits), lack of independent oversight, or potential loopholes in the text of the legislation. Ineffective regulations that do not consistently apply rules and penalties can distort companies’ cost-benefit analyses. While there is no silver bullet, governments should consider the following tools to strengthen enforcement and compliance with regulations:

- Better and more consistent reporting requirements and metrics.xlvii

- The use of satellite flaring data to monitor and detect discrepancies with reported data.

Financial and Economic Levers

Financial institutions and other private sector stakeholders also play a key role in leveraging positive and negative incentives to reduce flaring. Due to evolving shareholder priorities and ESG goals, major banks, pension funds, and other investors have increasingly sought to align investment decisions with environmental and climate objectives, which include climate prerequisites to qualify for financing, climate reporting requirements, and can involve adjusting the cost of capital based on emissions performance targets. These requirements are a powerful tool to drive company action, and investors providing finance to the upstream oil and gas sector should consider the following actions:

- Banks and other financial institutions can require flaring elimination/minimization plans before funding new oil and gas production projects and can finance flare reduction projects at existing sites.

- Investors can hold oil and gas companies accountable for the flaring at the assets they operate, assets they own but do not operate, and flaring at NOCs with which they have partnerships. They can also ask for better disclosure (including routine/non-routine flaring, flaring by country and/or basin, and flaring at both operated and non-operated assets) as well as improved targets (that include both routine and non-routine flaring).

In addition to these “sticks,” investors and private sector stakeholders can also offer “carrots” to drive flaring reductions. While many flare-reduction projects can result in net profit for companies due to the potential use or sale of captured gas, potential investments face high levels of competition for capital within companies, including potentially more profitable investments in core-business operations. Positive financial incentives, such as concessional loans or price premiums on captured gas, could increase the return on investment for flaring reduction, and drive company action. Financial institutions and downstream importers should consider the following tools:

- Banks and private investors should develop methane sustainability instruments and bonds, which could provide inexpensive capital under methane and flaring reduction performance targets. These instruments and bonds would require a comprehensive framework to define absolute emissions reduction targets and flaring targets, to allow for interest rates and capital costs to reflect a company’s performance.

- Downstream importers can require or incentivize flare reduction. For example, the European Union’s You Collect We Buy initiative aims to facilitate the purchase of gas that would have been otherwise flared or wasted, complementing the forthcoming emissions reductions obligations for the EU’s trading partners under the Methane Regulation.

IOCs should share best practices and financing with NOC partners and ensure that investments to reduce flaring at their own sites can be utilized to reduce flaring at a basin or regional level.

Appendix

Company Summaries

The following section aims to provide a granular dataset on IOC flaring by country in order to move the conversation forward about what IOCs can do to reduce flaring at both their operated assets and the non-operated ventures around the world. This novel dataset makes it possible to highlight notable flaring problem areas and advocate for mitigation opportunities.

For each company, we present four figures that together provide a fuller picture of flaring at each company:

- Production by Country, operated and non-operated

- Flaring Volume by Country, operated and non-operated

- Flaring Intensity by Country, operated, non-operated, and company average (country average also included for comparison)

- Mekko chart with the horizontal length of each bar representing the total crude oil and condensate production for each company, the height of each bar represents the average flaring intensity of the company, and the area of the box represents the total flaring volume.

We flag notable outliers, significant flaring volumes, and instances of high flaring intensity. We also note cases where the IOCs are invested in high flaring sites operated by national oil companies, as these are key instances where increased political will and economic pressure can help lead to reduced flaring.

ExxonMobil

ExxonMobil produces the majority of its crude oil and condensate in North America, with its production in the United States mostly from operated assets and in Canada mostly from non-operated joint ventures.

Figure 16a: ExxonMobil Production by Country

Total flaring volume for ExxonMobil is dominated by flaring in four countries: Nigeria, the United States, Malaysia, and Angola. In all these countries, most of the flaring is occurring at operated assets.

Figure 16b: ExxonMobil Flaring by Country

ExxonMobil’s flaring intensities for operated assets in Nigeria and Malaysia are high. In Nigeria, the flaring occurs at 15 flare locations, while in Malaysia only six flare locations contribute to this total flaring volume.

Argentina has a relatively high intensity, due to flaring volumes associated with very small amounts of production, mostly at non-operated assets.

Figure 16c: ExxonMobil Flaring Intensity by Country

Countries where ExxonMobil has the most production of crude oil and condensate, like the United States, Guyana and Kazakhstan, have relatively low flaring intensities. Average flaring intensity is 1.1 m3/bbl across operated and non-operated assets. Countries, like Nigeria, where the intensity exceeds the average are due primarily to operated assets. There is significant potential to reduce flaring and associated emissions from their operated assets, in Nigeria, Malaysia, Argentina, and Angola.

Figure 16d: ExxonMobil’s Flaring Intensity vs. Crude Oil and Condensate Production

Chevron

Chevron produces the majority of its crude oil and condensate in the United States mostly from operated assets onshore and non-operated assets offshore. The second largest country for production is Kazakhstan; from mostly non-operated joint ventures.

Figure 17a: Chevron Production by Country

The total flaring volume for Chevron is dominated by flaring in two countries, Nigeria and Angola, with 14 and 13 flaring assets, respectively. In both countries, most of the flaring is occurring at operated assets.

Figure 17b: Chevron Flaring by Country

Chevron’s flaring intensity is higher than the country average in Saudi Arabia and Angola. In Nigeria, the flaring intensity for its operated assets is much higher than that of its non-operated assets.

Figure 17c: Chevron Flaring Intensity by Country

Chevron’s flaring intensity is the highest for operated assets in Angola and Nigeria. The average flaring intensity of Chevron’s assets is 1.2 m3/bbl.

Figure 17d: Chevron’s Flaring Intensity vs. Crude Oil and Condensate Production

BP

BP has significant non-operated assets in Iraq, UAE, Norway, and Angola. In Azerbaijan, the United Kingdom, and the United States (onshore), most of its production is from operated assets.

Figure 18a: BP Production by Country

BP’s total flaring volume is dominated by Iraq and Angola, which accounted for more than 80% of the company’s equity-weighted flaring in 2023—all from non-operated assets. In Angola, the flaring is spread across 32 observed flares, and BP participates in these production assets through its Azule Energy joint venture with Eni. In Iraq, BP holds a non-operating stake in 14 flaring assets, along with co-owners Basra Oil Company (an Iraqi NOC) and PetroChina. The company also has significant flaring at operated assets in the United States and Azerbaijan.

Figure 18b: BP Flaring by Country9

BP has its highest flaring intensities in Iraq and Angola underestimating the flaring associated with its production. BP is involved in major flare capture project in both Angola and Iraq, but even still, flaring remains very high in these countries.xlviii To the extent that flaring from these non-operated assets is not included in the company’s sustainability report flaring, it is significantly underestimated.

Figure 18c: BP Flaring Intensity by Country

The countries where BP produces the most crude oil and condensate include Iraq, Angola, Azerbaijan, the United States, the UAE, and Norway. BP’s flaring intensity is significantly lower in several other countries, such as the UAE and the United States. This highlights the potential for reducing flaring in its higher-intensity assets. BP’s overall flaring intensity is 3 m3/bbl.

Figure 18d: BP’s Flaring Intensity vs. Crude Oil and Condensate Production

Shell

Shell’s portfolio is dominated by significant non-operated assets in Brazil, Oman, Kazakhstan, and the United Kingdom, and operated assets in the United States and Nigeria.

Figure 19a: Shell Production by Country

Shell has the highest flaring volumes in Oman and Nigeria. It has smaller but still considerable amounts of flaring in Brazil, Australia, Argentina, Brunei, Malaysia, Syria, United Kingdom, and United States relative to its production. In Brazil, the 16 observed flares attributed to Shell are all at facilities operated by Petrobras.

Figure 19b: Shell Flaring by Country

Shell has significantly high flaring intensity at its non-operated assets in Nigeria, Oman, and Malaysia, as well as its operated assets in Australia. Flaring intensity in China is disproportionately high because its assets in that country are producing very little crude oil and condensate.

Figure 19c: Shell Flaring Intensity by Country

Shell’s average flare intensity is 1.2 m3/bbl. Although Shell does not have much production in Australia, the intensity of their operated assets is nearly 10 times higher than their company average. The majority of the flaring attributed to Shell comes from their non-operated assets in Oman and its operated assets in Nigeria.

Figure 19d: Shell’s Flaring Intensity vs. Crude Oil and Condensate Production

TotalEnergies

TotalEnergies has significant crude oil and condensate production at assets throughout Sub-Saharan Africa, the Middle East, North Africa, and Central Asia. Much of this production comes from non-operated assets, except for notable exceptions where it is the operator in Angola, Nigeria, Congo, and the United Kingdom. Note: TotalEnergies produced approximately 2 bcm of crude oil and condensate in Russia in 2023, but that production, and flaring from those assets, is not included in these figures.

Figure 20a: TotalEnergies Production by Country

The highest flaring volumes by country occur in Iraq, Libya, and Nigeria—the first two are solely non-operated assets while the latter is split between flaring at operated and non-operated assets. In Libya, all the flaring assets attributed to TotalEnergies involve the Libyan NOC as a majority stakeholder.

Figure 20b: TotalEnergies Flaring by Country

TotalEnergies has the highest flaring intensities in Gabon, Congo, Iraq, Algeria, and Libya; which are predominantly non-operated assets. In Gabon and Argentina, it also has a notably high flaring intensity at operated assets that is more than three times the national average. In Angola, its flaring intensity at non-operated assets is more than twice that of the country average.

Figure 20c: TotalEnergies Flaring Intensity by Country